Sign In

President Obama signed the new health law into effect back in 2010, but its four most momentous changes kick in Jan. 1, 2014:

The centerpiece of the transformed health care system wrought by the Affordable Care Act is an entirely new way of choosing and purchasing individual health insurance known generically as marketplaces. They open for business Oct. 1, 2013, in every state, whether the state is willing or not.

This year only, marketplace open enrollment will run from Oct. 1, 2013, through March 31, 2014. In subsequent years, it will take place on the same schedule as Medicare open enrollment: Oct. 15 through Dec. 7.

In the marketplace, a kind of virtual insurance store, millions of Americans will be able to sign up for the plan of their choice, just like that, no questions asked about their medical history. Well more than half will get the welcome news that they have income-based tax credits coming to them to help pay the premiums.

In addition, about 4 million of the poorest Americans will become newly entitled to free or ultra-low-cost Medicaid coverage, which they can apply for on the spot in their state's marketplace. It's one of the most significant expansions of this government-paid health program since its creation in 1965. But at least 5 million more will live in states that have decided not to expand Medicaid in that way, leaving them uninsured and too poor to get tax credits.

Judging from the decibel level of the public argument, you'd think that the new health law will upend the health insurance of practically everybody. But that's not the case. At least 80 percent of Americans will notice almost no change because they already have insurance that meets the law's requirements.

That includes the 49 percent of Americans who get health insurance through their or someone else's job, as well as people who get insurance through the government. That includes Medicare, most Medicaid coverage, CHIP (health insurance for children in low-income families), some Veterans Affairs coverage, and Tricare (health insurance for active-duty military, retirees, and their families).

Although the law applies across the land, how you experience it will depend on your state. Some states have embraced the law. They've been working on their marketplaces for some time and have leaned on insurance companies to give consumers a good deal. In those states, you're likely to see lots of ads and public-service announcements and find it easy to get information about the new law.

But other states have been less gung-ho. As of now, 22 are not expanding Medicaid, and three more are still debating it. Thirty-four have forced the federal government to run their marketplaces in whole or in part, a development that is putting federal officials under deadline pressure.

This report explains what you need to do to get ready for the new law, depending on

whether you now get insurance:

For more detailed advice and calculators that can help you determine your eligibility for subsidies and links to state-run marketplaces, go to our comprehensive online guide at HealthLawHelper.org.

Regardless of how you get your insurance, also check out the rankings of health insurance plans, which can help you choose a plan.

Confused by the new health law? Try our free tool HealthLawHelper.org. (The tool is in Spanish at AseguraTuSalud.org.) Answer basic questions about your age, household size, income, and where you get insurance now, and it will tell you what you have to do (if anything). It won't tell you which insurance plan to buy, but for help deciding, turn to our rankings of health plans based on quality and value.

If you get health insurance through your work or someone else's, you've met your obligation to be insured. Your only job will be to hang onto a couple of forms that you'll be given:

Even if you have insurance through your employer, you might need to consider other options in two scenarios:

Your employer cancels your plan for 2014. That could happen, especially if you have a so-called "mini-med" plan that provides severely limited benefits. Those plans had an exemption to continue operating through the end of 2013 only. If you lose your employee coverage, you may be able to get better insurance through your state marketplace and possibly qualify for subsidies to help pay for it.

You have a very expensive plan. In that case, you may—or may not—qualify for some financial relief.

Dig out that employee form you got in the fall. You should find what your employer charges employees for the cheapest individual plan it offers.

If that number is more than 9.5 percent of your household income, and your income is below certain levels, you can turn the plan down and purchase your own coverage on your state's marketplace, with a subsidy. But if it's less than 9.5 percent you can get a subsidy only if your plan covers less than a "minimum value" of expected medical costs. The form should include information about that.

But an important catch may ensnare some families with multiple members covered on the same plan.

If, for example, your employer charges you $20 a month but $750 more to add your spouse and $250 more to add your kids, even if the total premium adds up to more than 9.5 percent of your family's income, you can't get a marketplace subsidy because the employee-only contribution is the one that counts. It's unfair and may need to be fixed with new legislation.

If that happens to you, price plans in the marketplace for your dependents anyway. Even at full price it might be cheaper than keeping them on your employer plan.

The marketplace is designed for people like you. You can't compare it to anything you have already experienced because it's an entirely new animal, a centralized resource where you can do the following.

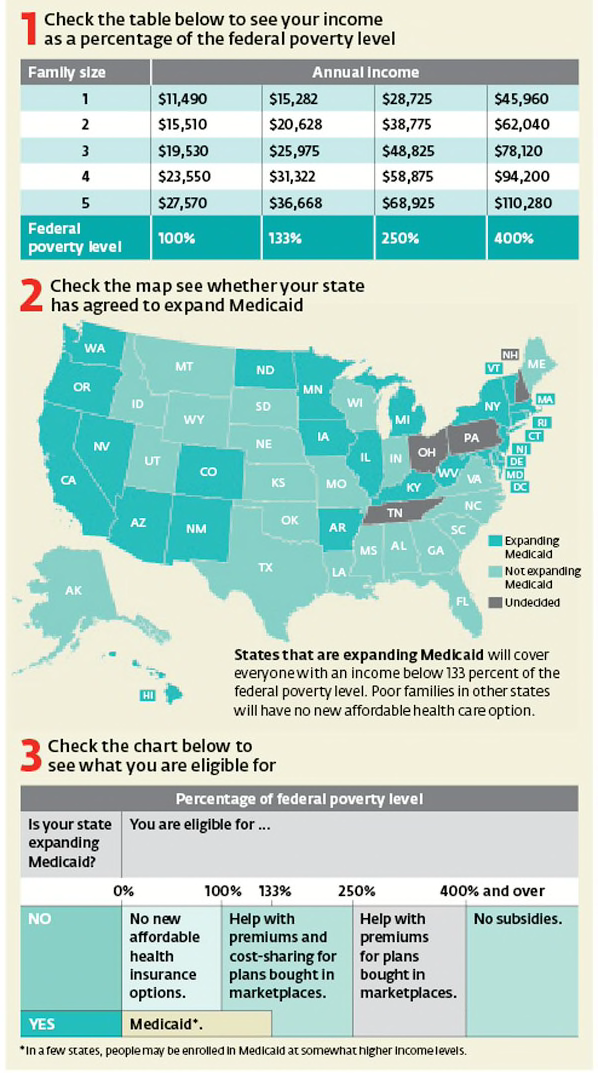

Investigate financial help. Find out whether you qualify for income-based assistance with your premiums, lower out-of-pocket costs, or free or almost-free Medicaid. (See this table for what types of help are available depending on income level.) You can still buy private insurance outside the marketplace, but you can qualify for and receive financial assistance only within the marketplace.

The help will come in the form of a tax credit that you can use right away to lower your premium. Lower-income households will also receive help with out-of-pocket costs. For details, download our free brochure at ConsumerReports.org/healthtaxcredit.

Shop for health plans. Compare private insurance plans that offer comprehensive health benefits and meet other qualifications. You'll be able to see the premiums you would pay, the health care providers who belong to each plan's network, plan details such as deductibles and co-pays, and in some states, quality ratings. (You should also check our free health plan rankings to see how similar plans fared.)

Enroll in a plan. Coverage can start as early as Jan. 1, 2014. You won't have to provide any information on your health history because insurance companies won't need it anymore.

Get Medicaid or CHIP. Enroll in Medicaid or CHIP for your kids if your income qualifies. More people will be eligible for Medicaid in states that are expanding the program.

To find your state's marketplace, start at HealthCare.gov, the federal government's omnibus health reform site. (In your state the marketplace may be called something else, such as Kynect, MNsure, or NY State of Health.) Or call the federal information line at 800-318-2596 to talk with a representative. Licensed insurance brokers can act as marketplace intermediaries according to state regulations.

If you already have bought health insurance on your own, you can keep it and it will satisfy the new requirement to have insurance. But it still pays to check out your marketplace options. You might find that you qualify for a better plan at lower cost.

Confused by the new health law? Try our free tool HealthLawHelper.org. (The tool is in Spanish at AseguraTuSalud.org.) Answer basic questions about your age, household size, income, and where you get insurance now, and it will tell you what you have to do (if anything). It won't tell you which insurance plan to buy, but for help deciding, turn to our rankings of health plans based on quality and value.

If you're on Medicare, you don't have to do anything or buy anything extra to comply with the new law.

Medicare Part A and Advantage plans fully qualify as insurance under the new law. And nothing significant about Medicare is changing in 2014. Benefits and programs will work the same as they do now.

But there is one situation in which the new health care law might help: You are a new enrollee and your spouse isn't on Medicare yet.

Once the older spouse retires and enrolls in Medicare, the younger, often nonworking spouse, may suddenly be without insurance. The spouse often has a hard time buying an individual policy because of pre-existing conditions.

Now the younger spouse can buy a plan on the marketplace and not worry about getting turned down or charged extra on the basis of a pre-existing condition.

Note: If you're the younger spouse, you'll need to put down your joint income when applying for marketplace coverage, even though you're the only one doing the buying. Your subsidy, if any, will be based on that number.

Maybe, depending on where you live and how much you make.

People who buy insurance through the new marketplace can receive various levels of financial help depending on where their household income falls in relation to the current federal poverty level. In states that are expanding Medicaid, all low-income households will be enrolled. In other states, many may be left with no affordable source of health insurance. (But they won't be fined in that case.)

Health care can be very expensive, far beyond the means of most people. It costs about $30,000 to deliver a baby or to stay in the hospital for three days, and a bout of breast cancer can top $100,000. Health insurance reduces your costs by sharing risk with others. That works because most people are mostly healthy most of the time. Here are three things you need to know when choosing insurance.

Before health reform, insurers were allowed to sell plans that didn't cover important services, such as prescription drugs, mental health, and maternity care. Plans for individuals and small businesses that take effect on or after Jan. 1, 2014, must offer these "essential health benefits": emergency services, hospitalization, laboratory tests, maternity and newborn care, management of chronic diseases such as diabetes, mental health and substance-abuse treatment, outpatient care, pediatric services including dental and vision care, prescription drugs, preventive services such as immunizations, mammograms, and colonoscopies, and rehabilitation and habilitation services. Most plans through large employers will provide the same benefits.

You pay for health insurance in two ways: up front in the form of a monthly premium and when you actually receive health care in the form of out-of-pocket expenses such as deductibles, co-insurance, and co-pays.

Whether you are better off with a high premium and low out-of-pocket expenses or vice versa depends on your situation:

No private health plan gives unrestricted access to doctors and hospitals. Every plan has a network of doctors, hospitals, laboratories, imaging centers, and pharmacies that provide services to plan members at a contracted price. Every marketplace plan must provide a directory of participating providers that you can consult before you make your final plan selection.

Confused by the new health law? Try our free tool HealthLawHelper.org. (The tool is in Spanish at AseguraTuSalud.org.) Answer basic questions about your age, household size, income, and where you get insurance now, and it will tell you what you have to do (if anything). It won't tell you which insurance plan to buy, but for help deciding, turn to our rankings of health plans based on quality and value.

This article appeared in the November 2013 issue of Consumer Reports magazine.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop