Most of us know which local hospitals and doctors are covered by our insurance providers, but even when we make sure that we only see an in-network physician or surgeon, nearly one-third of privately insured Americans are still hit with higher-than-expected medical bills, often because their in-network hospital brought in or contracted out to an out-of-network service provider. How did we get to the point where so many consumers have so little information about what to expect when their hospital bill arrives?

According to consumer advocates and a medical billing specialist who spoke to Consumerist, the problem of surprise medical bills isn’t exactly new, but healthcare providers appear to be taking greater advantage of long-existing loopholes in the insurance system, leaving more patients feeling blindsided when they finally get their bills.

“It’s a tremendous problem that seems to be getting worse and worse,” Chi Chi Wu, an attorney with the National Consumer Law Center, tells Consumerist. “The big picture is that it’s due to peculiarities and problems and how healthcare is priced in the U.S.”

Out-Of-Network Vs. In-Network

At the core of the issue is the distinction between in-network and out-of-network health insurance coverage and how each is priced and passed on to consumers.

In-network providers are those who have agreed to charge lower fees to customers of a particular insurer, with the expectation that being listed as a covered provider will bring in more patients.

Julie, a long-time medical billing specialist, provided Consumerist with an example of how in-network billing works:

You have a procedure done for which an in-network doctor normally charges $1,000, but your insurance company has negotiated a maximum fee of $600 for that procedure with that doctor, so that’s the most the physician can charge.

The doctor must write off the remaining $400 and is prohibited from “balance-billing” you for the difference between the $1,000 list price and what your insurance’s “maximum allowable amount” or “negotiated fee” is for that service.

On the other hand, an out-of-network doctor is, basically, not bound by any rules of your insurance company because he or she has not agreed to any of maximum.

That doctor, therefore, can charge you the full $1,000 for that procedure, or the difference between $1,000 and whatever your insurance pays, with no discount.

The Problems With Sticker Price

While the idea of in-network and out-of-network might is fairly straightforward — you’ll pay more going to an out-of-network provider because he or she simply isn’t covered by your insurance — healthcare providers sometimes present patients with situations where part of the care is covered and part is not.

For example, you may go to an in-network hospital for surgery, only to find out that somewhere along the way, the hospital brought in another doctor — many times, it’s the anesthesiologist — or used a lab, or hired an outside consultant, that is out-of-network. This is often done without notifying the patient, meaning they won’t know until they get their bill that their insurance will not cover all of these particular costs.

And even if your insurance provider will agree to pay some amount to these out-of-network providers, they can still come after you for the balance.

“Your financial responsibility for a given charge is going to vary widely based on your specific treatment,” Julie says.

Part of the reason for this, as Wu of the NCLC previously pointed out, is because of the way healthcare is priced in the U.S.

“Most hospitals and providers, including ambulances and the field of dentistry, have a master price list – or a sticker price – but that is rarely what gets paid,” Wu says.

Much like other industry the prices shown in the medical field are often much higher than what is typically paid.

Wu likens the situation to that of the hotel industry: you may see a hotel room for $500 per night, but no one really pays that much because there are almost always special rates or discounts.

Likewise, the price of medical care, while shown to be much higher on the master charge list, is discounted by the insurance companies — sometimes referred to as a negotiated maximum fee.

“The providers start giving discounts on that price,” Wu says. “So Medicaid might get the lowest price, then Medicare, private health, and so on. The only people who end up paying the charged master price are those who are uninsured.”

And that becomes a problem when someone who is insured ends up at an out-of-network provider or when an out-of-network physician unexpectedly provides service at the patient’s in-network facility.

While hospitals generally accept the insurance plans of the doctors they directly employ, physicians are not always tethered to a single facility, and many are independent contractors who work with patients at multiple hospitals. This means they can pick and choose which health plans to participate in with little regard to the hospital or facility in which they practice.

By doing so, these doctors are able to charge higher prices when a patient doesn’t have a preferred plan, leaving that consumer with a much more expensive bill than they were possibly anticipating.

It all ties back to that master list of sticker prices, says Wu, who adds that “unfortunately, consumers can only do so much to prevent this, especially in an emergency situation.”

Different Plans, Different Coverage

If you want to avoid or minimize costly and unexpected medical bills, it’s important to understand the basic types of health insurance, and to know which one you have.

There are several varieties of plans available to consumers, whether through their workplace, the government, or through the private insurance marketplace.

The most common types of insurance plans are an Exclusive Provider Organization (EPO), a Health Maintenance Organization (HMO), Point of Service (POS), a Preferred Provider Organization (PPO) and Medicare/Medicaid.

Each plan includes a different set of requirements and stipulations on what exactly is covered.

For example, a EPO covers services only if you use doctors, specialists, or hospitals in the plan’s network – except in an emergency.

A HMO typically limits coverage to care from doctors who work for or contract with the HMO. That means it generally won’t cover out-of-network care except, again, in an emergency. In many cases, a HMO will require you to live or work in its service area to be eligible for coverage.

A POS plan allows users to pay less if they use doctors, hospitals, and other healthcare providers that belong to the plan’s network. However, this type of plan generally requires that patients get a referral from a primary care doctor in order to see a specialist.

With a PPO, users pay less if they use a provider in the plan’s network; they can typically use doctors, hospitals, and providers outside of the network without a referral for an additional cost.

While the above plans are private insurance, Medicare and Medicaid are government-run programs.

Medicare is a federal, government-run healthcare that covers U.S. citizens over the age of 65 and younger disabled people.

Although patients do pay premiums and have small deductibles, and they have to pay a 20% co-insurance for many services, many patients buy supplemental policies that will cover some or all of the deductible and coinsurance, so many Medicare patients have few out-of-pocket costs for covered treatment.

Medicaid is a government-run healthcare program for low-income Americans that is managed at the state level.

“So while Medicare’s policies are set at the federal level and operate the same in all 50 states, Medicaid policies operate differently in each state and in most cases; Medicaid patients in one state could have trouble finding care in another state,” Julie tells Consumerist.

Just Some Of The Costs

While all of these insurance plan can make the expense of visiting a doctor or undergoing surgery less of a burden for consumers, they don’t generally cover all of the costs.

That’s because insurance is an intricate web of coverage where aspects like deductibles, co-insurance, and co-pays vary from plan to plan.

While understanding insurance can be a daunting task, there are some key aspects of most plans that consumers should be familiar with when it comes to knowing their obligations.

One of the most important is the deductible — the amount of money that the patient will have to pay each calendar year before your insurance will start paying on your medical bills.

Your co-pays and co-insurance — more on those in a moment — will not be charged to you until you’ve met your deductible for the year.

So, for example, when visiting the doctor for a routine exam you may have been asked to pay a co-pay. This is a flat fee that is paid every time you get a particular type of medical care from a provider — usually only after your deductible has been met.

And then there’s co-insurance, which is the percentage of charges that consumers will have to pay to their medical provider after having met a deductible and the insurance has started paying on the claims.

In a hypothetical scenario, a schedule of benefits chart may show that you would owe: a $20 co-pay for an office visit, or 20% of the cost for radiology services – meaning X-rays, MRIs or other testing – after insurance.

In this example, co-insurance would apply to radiology services and to outpatient services (usually surgery), but would not apply to regular doctor office visits.

Once you’ve met your deductible, your insurance would pay 80% of their “allowed or negotiated amount” for an MRI that you receive, and would require you to pay 20%, Julie explains.

If you had an outpatient surgery and had met your deductible, your insurance would pay 90% of their “allowable” and would require you to pay 10%.

“Exactly what you would have to pay for co-insurance is nearly impossible to calculate, because it bears no relationship to what the doctor actually charges for his or her services,” Julie says.

What Can Be Done?

Short of overhauling the entire medical and insurance industries, the best thing you can do to avoid being surprised by a doctor or hospital bill is to be prepared and aware.

Over at Consumer Reports, they recently published tips for avoiding bill shock from your healthcare provider.

For example, if you’re going to have a non-emergency procedure — something like delivering a baby where many parents-to-be select their doctors and hospitals months in advance — ask your doctor’s billing folks to provide a complete list of the anesthesiologists, assistant surgeons, and everyone else who could conceivably be part of your medical team.

Check with your insurer to see if these providers are all covered — not just by your insurance company but by your particular plan. If you come across someone involved in your procedure who is out-of-network, ask for an in-network option. And if that is not an option and you can’t have the procedure done by someone else, then contact that non-network provider to find out in advance what you’ll be expected to pay.

Likewise, it helps to know which hospitals in your area not only accept your coverage but also only have in-network emergency room staff. As you’ll see in an upcoming Consumerist story, some ERs go out-of-network for staff, leaving patients with potentially huge bills or having to drive out of their way to seek emergency care.

“Even if you go to a hospital in your network, the unfortunate truth is that there is no guarantee that all your treatment — whether it’s the radiologist, anesthesiologist or lab work — will be treated as in-network,” DeAnn Friedholm, former Director of Health Reform for Consumers Union, said earlier this year in relation to a report released by the organization.

Still, several states have attempted to prevent unfair out-of-pocket costs from devastating consumers by enacting or proposing new laws.

Back in June, the California Assembly passed a measure that would only require a patient who obtains care at an in-network facility but from an out-of-network provider to pay the non-participating provider what would have been charged by a participating provider.

That means if you go to your local hospital – which is covered by your insurance – and you see a doctor who isn’t covered by your insurance, you would only be on the hook for the amount you would typically pay if the doctor you saw was considered in-network.

Additionally, any cost that the patient pays for services by the non-participating provider will count toward their limit for annual out-of-pocket costs.

The California bill would have applied to health care service plan contracts and insurance policies issues, amended or renewed on or after July 1, 2016. In September, the bill passed the California Senate, but when it was sent back to the Assembly for a final vote, it failed because of strong opposition.

[Editor’s note: a previous version of this story contained an out-dated status for the California measure.]

Other states have taken different approaches.

A report [PDF] for the California HealthCare Foundation also explored several states with laws that take varying approaches to balance billing to see if any would provide more adequate protection to consumers.

The paper refers to a measure in Texas that aimed to increase transparency by providing consumers access to data, such as pricing and network participation information, needed to estimate their financial liability for medical services.

For example, a managed care organization – such as a PPO or HMO – must disclose, in writing, whether a network facility uses non-network providers and that a member may be balance billed by a non-network provider.

When the report was published, not enough time had passed to determine if the measure was advantageous for consumers, but the authors noted that many stakeholders reported concerns about how valuable the information would be, especially with regard to emergency medical care.

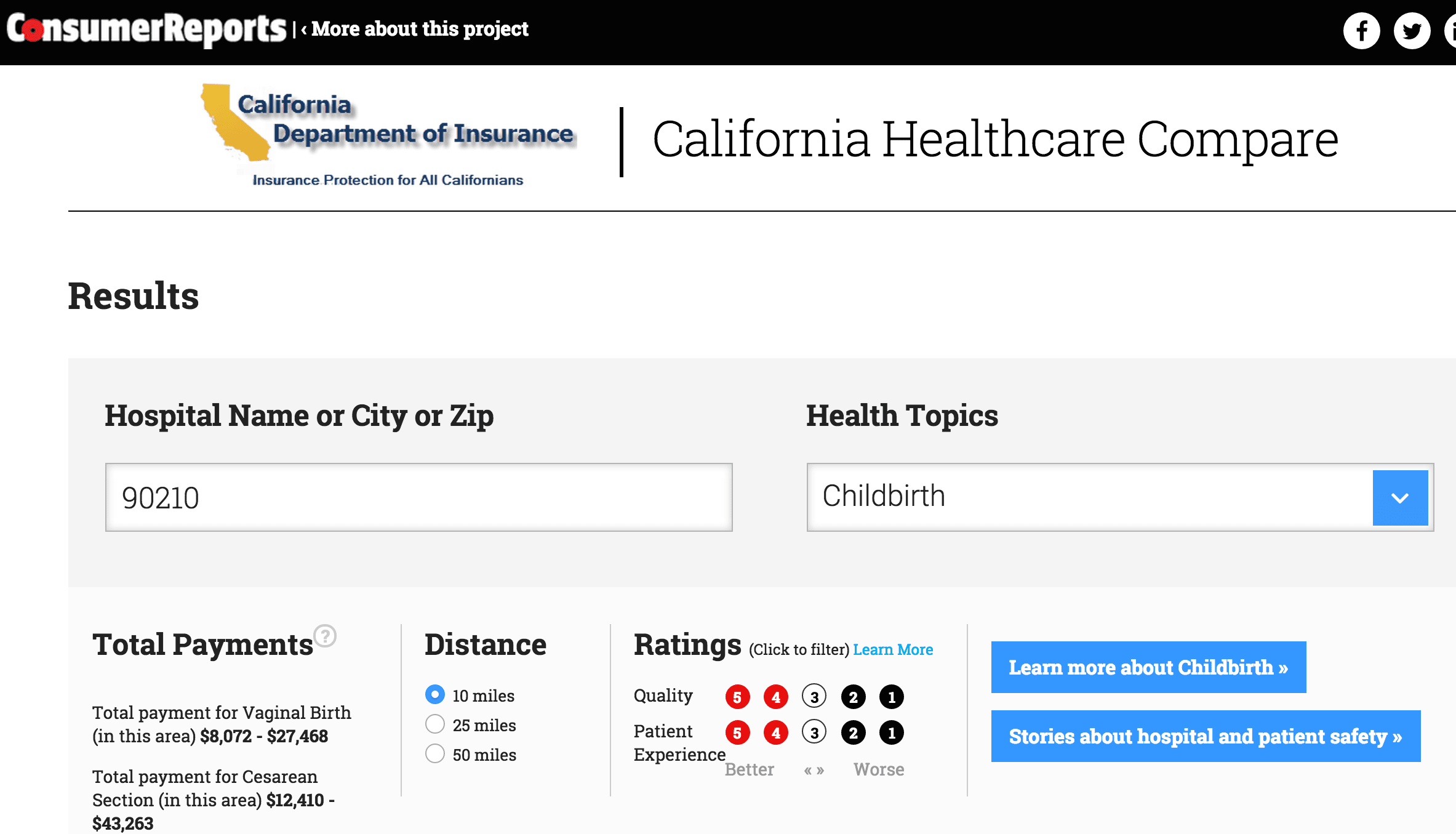

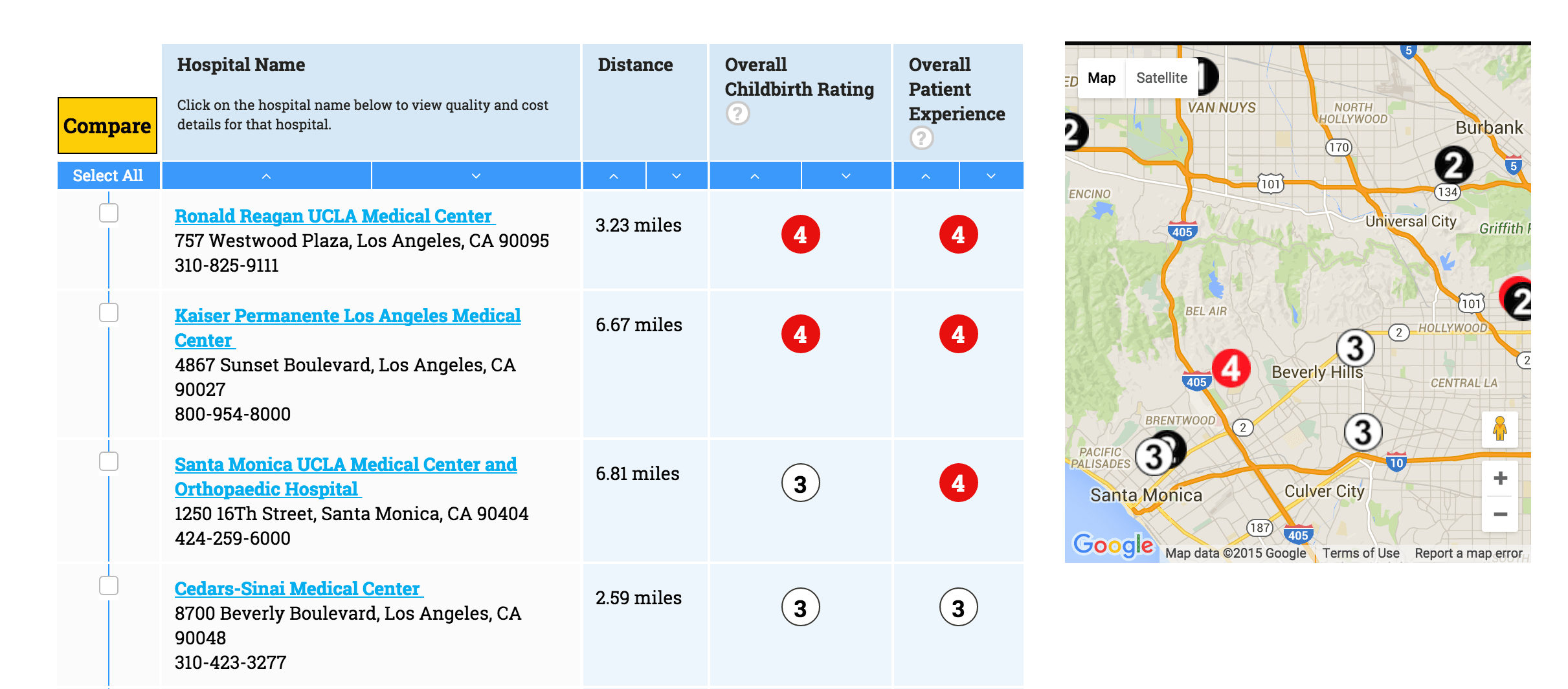

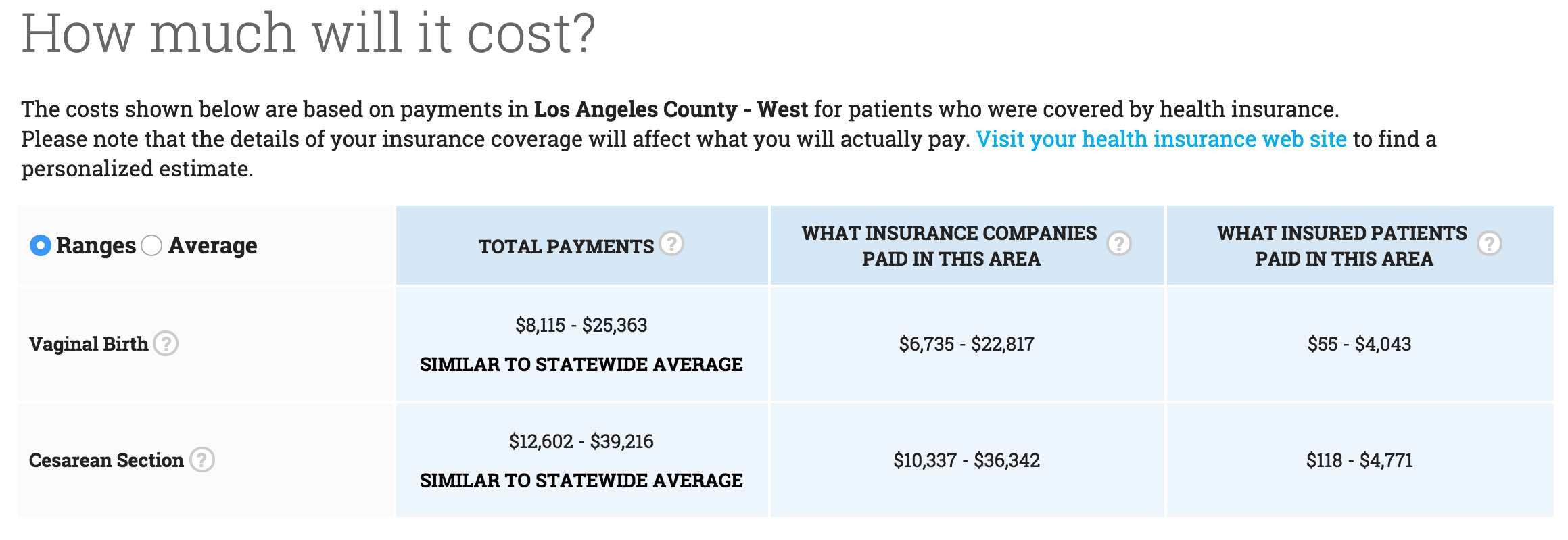

More recently, Consumer Reports teamed up with California Insurance Commissioner Dave Jones, and the University of California San Francisco to announce the launch of California Healthcare Compare, an online tool that allows you to search local hospitals in the state based on different types of procedures. The results provide consumers with information about hospital ratings, and what sort of costs patients should expect to pay:

(NOTE: We only know one California ZIP code off the top of our heads; thus the 90210)

In Florida, the authors found a law that places restriction on balance billing with regard to payment rate requirements in emergency settings.

When a consumer seeks emergency care, or to evaluate if an emergency condition exists, the statute makes the HMO liable for costs, and restricts the non-network provider from balance-billing the patient.

According to the report, this measure has so far been effective, but it only applies to HMO members.

While some states have found taken steps to ensure consumers are protected, those measures aren’t foolproof.

Editor's Note: This article originally appeared on Consumerist.