By now you’re probably used to going to your bank’s website and being upsold on everything from car loans to mortgages to retirement accounts before you can move on to see how your money is doing. But have you ever gone to your bank’s site only to be told you must update your income with the bank before going any further?

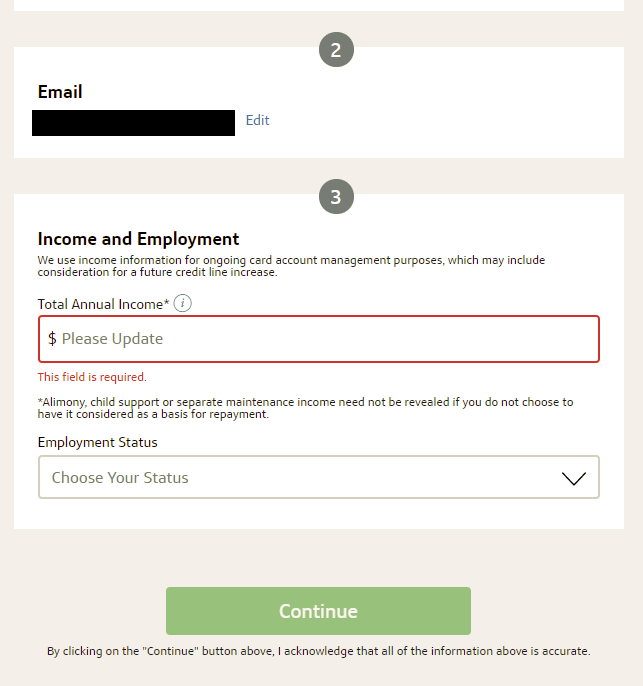

That’s what happened to Consumerist reader Sean, who was just trying to log on to CapitalOne.com, where he has both a savings account and a credit card, only to be faced with a demand for his latest income info:

He said he suspected it had something to do with him having a Capital One credit card, and acknowledged that other financial institutions had asked for such information in the past, but that he’d never seen anything “so intrusive” because there was no option to opt out. He was frustrated that he couldn’t access his non-credit card accounts without entering something in that field.

“Maybe it was just an error because I have a credit card with them too, but this feels really unethical,” Sean wrote, wondering if it was legal to require that information before allowing him to log in to see any of his accounts.

Is This Legal?

Although Sean felt Capital One was being intrusive, it’s not only legal for credit card companies to ask for income information, they’re also required by law to keep records of that info current: According to federal regulations, credit card issuers have to make an “ability to repay” evaluation when considering potential customers, or when contemplating credit increases to existing customers.

“A card issuer must not open a credit card account for a consumer under an open-end (not home-secured) consumer credit plan, or increase any credit limit applicable to such account, unless the card issuer considers the consumer’s ability to make the required minimum periodic payments under the terms of the account based on the consumer’s income or assets and the consumer’s current obligations,” states this ability-to-repay rule.

To accomplish this, card issuers may consider things like the ratio of the customer’s debt obligations to their income.

“It would be unreasonable for a card issuer not to review any information about a consumer’s income or assets and current obligations, or to issue a credit card to a consumer who does not have any income or assets,” the rule reads.

Capital One notes this on their web site:

“It’s important to make sure that all your personal info is accurate and current. Federal regulations generally require that credit card companies use up-to-date income information when considering an account for a credit limit increase,” the site reads. “Check yours at least once a year to make sure it’s accurate.”

Credit card companies don’t just rely on customers’ past disclosures, however. They may periodically reach out to them to make sure the information is still correct.

“It is important that we have current customer information for ongoing account management purposes,” the Capital One rep told Consumerist. “We conduct reviews regularly, and ask customers to update their info if it is either missing or dated.”

So again, while this may feel icky, it’s definitely legal — and could actually benefit you in the long run.

“While it may feel uncomfortable to be asked how much you make when you contact your credit card company, credit card companies have a legitimate reason for asking,” Christina Tetreault, our colleague and Senior Staff Attorney for Consumers Union, explains. “Having your income information helps credit card companies calculate how much credit they should offer you, and ideally means that you can manage to repay what you borrow.”

How To Get Around It

When Sean contacted Capital One on Twitter, a customer service representative told him that he was not required to provide that information before he could log into his accounts, and that he could enter “123” into the “Total Annual Income” field to bypass the option.

However, the bypassing method is not disclosed on the screen when Capital One requests the information, which could have been useful to Sean at the time he was attempting to log in. Instead, he had to reach out to Capital One on Twitter.

In an email from Capital One to Sean after his Twitter chat, a company rep said they were aware of his concerns, and “there not being an option to opt out without contacting us about how to bypass it.”

The company said it’s glad the social media rep alerted him to the bypassing method, and that it appreciates him “addressing these concerns for other customers in the same situation.”

So What’s The Deal With “123”?

As it turns out, the rep wasn’t just advising Sean to enter any old random numbers — and effectively lie about his income in the process — but was instead offering a workaround.

“We allow customers that contact us and are reluctant to provide their income to use a code to bypass the income field,” a Capital One spokesperson explained to Consumerist, noting that the “123” code will not show up as your updated income, it’s just a sign to the system that the information wasn’t updated.

But be warned: Entering a random string of numbers into this field could constitute fraud, as you’re effectively giving the bank inaccurate information about your income.

When customers apply for a credit card with Capital One, they attest that everything they’ve stated is correct, including information about them needed to manage their account, the company’s rep noted. For example, among other things, it needs your legal name, date of birth, Social Security number, and employment and income information.

But because frustrated customers may put in whatever numbers come to mind in order to access their accounts — say, $1,234,567 — Capital One says it performs “reasonableness checks” to help verify information provided by customers.

Editor's Note: This article originally appeared on Consumerist.