Whether you get your health insurance through your employer, Medicare, or one of the Affordable Care Act (ACA) exchanges, there's a good chance you're paying more than you need to.

According to a study last year by the National Bureau of Economic Research, 63 percent of the 50,000 employees at a Fortune 100 company selected a health plan that was not the most cost-effective option. Other studies have shown that most people pick a plan that's more expensive than they need.

Why are so many people electing insurance plans that aren't the best fit? Because it's downright confusing, so much so that a 2015 study commissioned by the insurance company Aflac found that more people would rather scrub their toilets than research insurance plans.

Despite recent announcements from major insurers including Aetna and UnitedHealthcare that they won't be participating in some ACA exchanges in 2017, consumers in large markets can still have as many as 50 plans to choose from. There are hundreds of Medicare prescription drug plans and Medicare Advantage plans, and even employers may offer two or more choices.

Making the right health insurance choice has never been more important because consumers are shouldering more of the rising cost of health services. (For example, average annual deductibles for people buying individual coverage through their employer have risen 255 percent in the past decade, according to the Kaiser Family Foundation.)

Autumn is the period for open enrollment, when most American adults have to choose their health insurance plan for 2017. Deadlines are Dec. 15 for ACA coverage that begins Jan. 1 and Dec. 7 for Medicare. Most employers have their open enrollment period in November.

To help you navigate your way through all the offerings, we looked at four common mistakes people make when choosing insurance plans and provide advice on how to avoid them. So put down your toilet brush and follow these easy steps.

The Big Mistake: Automatically Reenrolling

Given the distaste for researching health-insurance plans, it's not surprising that the Aflac study found that nine out of 10 (PDF) workers stick with the same benefits year after year. Other research shows that only 13 percent of Medicare users switch drug plans each year, despite the fact that they could save money by doing so. And just less than 60 percent of Obamacare enrollees stayed in the same plan in 2016, even though a 2015 Department of Health and Human Services analysis found that eight in 10 could find a plan with a lower premium that offers the same coverage if they switched.

The remedy: Review all the offerings during open enrollment each year; plan benefits change frequently. Participating doctors are added and deleted, and drug formularies—the lists of prescription medications a plan covers—are revised. Other plan benefits, reimbursement rates, and premiums (the amount you pay each month for coverage) may also change from year to year. Insurance companies provide much of that information online and in the multipage packets your benefits department hands out.

But talking with an informed source can be more efficient, informative, and pleasant than sifting through all that information on your own. People who are covered under the ACA can discuss their options with someone by going to localhelp.healthcare.gov. Medicare offers counseling through its State Health Insurance Assistance Programs (shiptacenter.org), and about 50 percent of companies offer one-on-one help to employees.

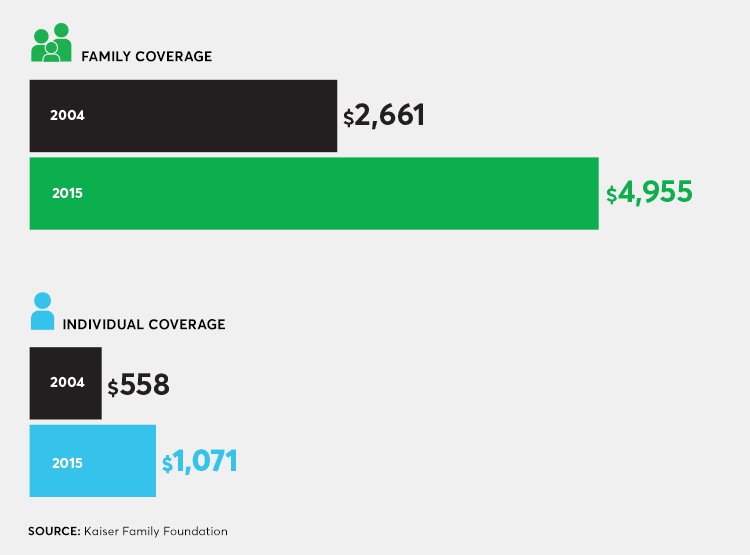

The Rising Price of Health Insurance

Average annual premium contributions paid by people in employer-provided insurance plans.

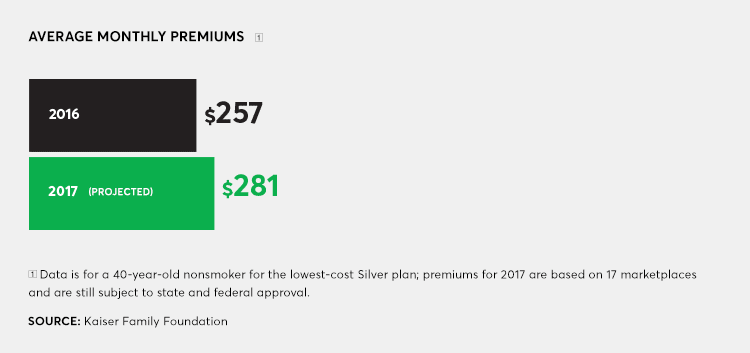

Premiums for Affordable Care Act health insurance are projected to be higher next year, but tax subsidies will offset the increase for most people.

The Big Mistake: Miscalculating Your Healthcare Needs

You can't choose the most cost-effective coverage without knowing how much you're likely to spend on healthcare in the coming year. Only then will you be able to make an informed decision between, say, a plan with a high deductible and one with a low deductible. But few people take the time to calculate their medical spending or even know how to do it. A study by the National Bureau of Economic Research found that only about one-third of workers at a large firm could answer questions correctly about their own recent healthcare spending.

The remedy: Of course, no one has a crystal ball to see into the future, but the amount you and other family members spent on healthcare this year is a good indicator of about how much you'll spend next year, says Kim Buckey, vice president of client services at DirectPath, a benefit and compliance management firm. You can find your claims (including what you spent out of pocket) on your insurer's website. Your pay stub will show how much you paid in monthly premiums, and your pharmacy will have a record of how much you spent on medication.

After you've determined how much you paid last year, "think about what could be different next year," Buckey says. Was someone in your family diagnosed with a health condition that requires new medication? Are you planning to start a family and make more visits to the OB-GYN? Are you finally going to get that surgery for your bunions? Talk with doctors about the cost, then see how much will be covered by the plans you're offered.

The Big Mistake: Focusing on Low Premiums

It's tempting to try to save money by choosing a plan with the lowest monthly premium, but that strategy can backfire. "If you shop by premiums alone, you could spend a lot more in out-of-pocket costs than if you had gone with a higher premium plan," says Kev Coleman, head of research and data at HealthPocket, a technology company that compares and ranks health insurance plans.

The remedy: In addition to premiums, consider the amount of the deductible—how much you have to spend before the insurance company begins covering expenses. Remember: The cost of many preventive measures, such as mammograms, colonoscopies, and cholesterol screening, are covered 100 percent before you meet your deductible and require no co-pay.

Deductibles can range from about $500 to $5,000 or more, but among low-premium plans, the average today is closer to the high end of that range.

Also look at co-pays (the flat charge you pay every time you go to a doctor, hospital, or other healthcare provider) and co-insurance (the percentage of the bill that you have to pay for treatments). You're responsible for co-pays and co-insurance for doctor visits and procedures even after you've met your deductible and until you hit your out-of-pocket maximum, which is yet another number you need to know.

As its name suggests, the out-of-pocket max is the most you have to pay for covered services in one year. After you've reached it, the insurer pays 100 percent of the costs. That max counts deductibles, co-payments, and co-insurance but not premiums or out-of-network services your plan doesn't cover. Generally, plans with lower premiums have higher out-of-pocket maximums and vice versa.

If you're in a low-premium/high deductible plan and didn't come close to meeting your deductible last year, you might do fine sticking with it. But if you quickly hit your deductible (perhaps because of a chronic health condition that requires frequent doctor visits), choosing a plan with a higher premium and a lower deductible could save you money overall.

Another way to ease the pain of high out of pocket costs is to use a flexible spending account (FSA) or a health savings account (HSA) if your employer offers one. Seventeen percent of small firms and 74 percent of large firms offer employees the option of contributing to an FSA. One-quarter of employers offer an HSA with a high deductible health plan (HDHP) and among large employers with more than 200 workers, 51 percent offer HSAs, according to the Kaiser Family Foundation's 2016 Employee Benefits Survey. HSAs and FSAs both allow you to set aside tax-free dollars to cover qualified out-of-pocket medical costs in the coming year. You decide whether to fund these during open enrollment.

Get more information on how FSAs and HSAs can ease the pain of healthcare costs.

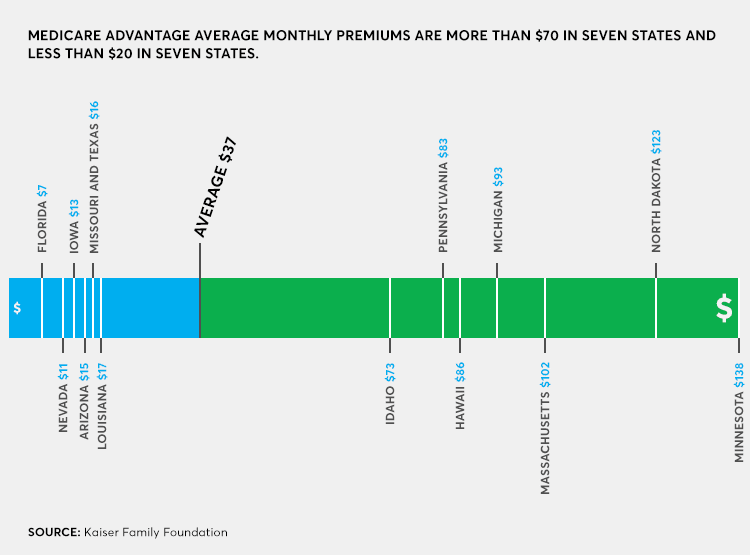

Medicare Advantage Plan Costs Vary Considerably By State

Average monthly premiums for Medicare Advantage plans have dropped since 2010, but there are vast differences in how much you pay depending on where you live.

The Big Mistake: Not Switching to Keep Your Doctor

For many people, keeping the same doctors is more important than cost. That's natural and important. If you're a parent, you may have a bond with the pediatrician who has treated your kids since they were infants. Or you have had the same trusted doctor for years. But just because your doctor is in your plan's network doesn't mean the network offers the broad choices of specialists and hospitals you may want.

The remedy: Focus on what's covered if you want to go out of network (to a well-known cancer treatment center or a top teaching hospital, for instance). Some plans provide no coverage for out-of-network nonemergency services, but others will provide some level of reimbursement. So even if your doctor isn't in the plan, you might be able to afford the cost. But if your plan offers little or no out-of-network coverage, you'll be stuck with most or all of the bill except in emergency situations. "When I choose a health plan, I look at whether the best hospitals in the area are included and if I have to go outside the state, will I have any of that care covered," Coleman says.

Editor's Note: This article also appeared in the November 2016 issue of Consumer Reports magazine.