New Payday Loan Ruling Is Bad News for Borrowers

Payday lenders can now expand even in states that tried to rein them in. What to know—and how to avoid payday loan perils.

On Election Day last month, more than four out of five Nebraska voters approved a ballot initiative that would cap interest rates on short-term, ultra-high-interest payday loans at 36 percent. The previous law allowed annual rates to climb as high as 459 percent.

Yet one week before the election, an obscure branch of the U.S. Treasury Department, called the Office of the Comptroller of the Currency (OCC), issued a ruling that many consumer advocates say could undermine the Nebraska voters’ intention—as well as anti-payday laws and regulations in other states around the country.

The initiative in Nebraska made it the 19th state, plus Washington, D.C., either to ban these short-term, ultra high-interest loans or to limit interest rates on them to a level that effectively bans them because lenders no longer see the business as adequately profitable.

Why Payday Lending Is a Problem

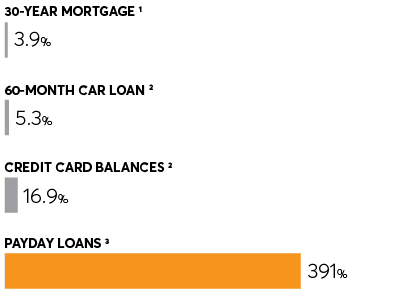

About 12 million Americans take out a payday loan each year, typically borrowing less than $500 at a time and promising to repay the loan in about two weeks—a promise usually sealed by the borrower handing over electronic access to his or her bank account or a signed, forward-dated check drawing on it.

When a consumer takes out a payday loan, the cost of borrowing is expressed as a fee, typically 10 to 30 percent of the loan. So to borrow $375, they would have to pay between $37.50 and $112.50 in fees. But that’s the cost to borrow the money for two weeks. Expressed as an annual percentage rate—the way we typically think about borrowing costs—payday lenders routinely charge around 400 percent, and in some states upward of 600 percent.

Compounding the problem is the fact that most borrowers can’t pay back their loans at the end of the two weeks—so they take out another loan to pay off the first, triggering another round of fees in the process. And then they do it again a couple of weeks later. In fact, more than 80 percent of payday loans are rolled over in this way, and half of all loans are part of a sequence of 10 or more such loans. All told, the average payday borrower ends up spending $520 on fees to borrow $375.

A 2015 survey by the Federal Deposit Insurance Company found that Hispanic and Black Americans are two and three times as likely to take out payday loans than non-Hispanic whites, respectively. And several studies by the Center for Responsible Lending have found that payday lenders disproportionately target areas with higher concentrations of people of color, even when the population data is controlled for income.

The Consumer Financial Protection Bureau in 2017 tried to curtail repeat borrowing with a regulation declaring it “unfair and abusive” to make payday loans without “reasonably determining that consumers have the ability to repay.”

The regulation never went into effect, however, and was revoked in July 2020, largely leaving it to states to protect their own citizens from the payday debt trap—which is why last month’s OCC ruling has consumer advocates so worried.

Rent-a-Bank Schemes

Would-be lenders have long tried to evade state usury laws using so-called rent-a-bank schemes: An out-of-state bank, which does not have to abide by interest rate caps in the payday lender’s state, acts as a front for the company that’s actually behind a high-interest loan that it couldn’t legally make itself. In exchange for “renting” itself out in this way—expending little effort and taking little risk in the process—the bank gets a small cut of the action.

Such schemes were common about 20 years ago but were mostly regulated away in the early 2000s. But, says NCLC’s Saunders, they’ve been making a comeback in the past two years, partly due to lack of enforcement. Her organization has documented rent-a-bank schemes involving at least six banks in at least 30 states in that time period.

To combat such schemes, regulators have historically invoked something called the true lender doctrine, a legal principle that lets courts determine which entity is the true lender based on factors such as who did the marketing work to generate the business, who is taking the financial risk, and who most stands to benefit. In the eyes of the law, the true lender must comply with the applicable laws.

The OCC's October ruling essentially discards the doctrine, declaring instead that the true lender is simply the entity named as the lender on the loan agreement.

In other words, consumer advocates argue, the OCC’s rule is a green light for payday lenders to get around state usury laws by simply typing the name of a willing out-of-state bank into the small print of its loan documents.

The OCC dismisses such concerns, stating that rent-a-bank schemes “have no place in the federal banking system” and denying that the ruling facilitates them. Nothing in it relieves banks of their obligation to comply with federal lending and consumer protection rules, the OCC notes, insisting that the rule merely eliminates legal uncertainty over who makes a loan and which laws apply as a result.

“By clearly identifying when the bank is the true lender, we can hold the bank accountable for all of the compliance obligations associated with the origination of the loan,” says Bryan Hubbard, the OCC’s Deputy Comptroller for Public Affairs.

But Saunders calls the OCC’s reassurances “completely hollow.” The fact that banks must comply with federal and even state laws doesn’t prevent them from participating in rent-a-bank schemes, she says. “As the OCC well knows, nearly every state in the country has no cap on the interest rates for banks, and the law allows banks to charge any rate their home state allows, no matter where they lend,” she says.

“If what the OCC says is true, the rule falls short by not expressly prohibiting rent-a-bank schemes,” agrees CR’s Carrejo. “In fact, the rule represents a complete abandonment of a two-decade-old policy of explicitly banning rent-a-bank schemes.”

Strategies for Avoiding the Payday Debt Trap

It remains to be seen whether payday lenders take advantage of the apparent loophole on a large scale. For now, no matter what state you live in, be extremely wary of taking out high-interest, short-term loans. Here are some ways to avoid doing so.

Build up an emergency fund. The best way to avoid high-interest loans is to have money set aside in advance to cover a surprise budget shortfall or emergency expense. Start small by squirreling away $10 here and $50 there. Then try to stash enough away to cover a month’s worth of bills. After that, aim for three months' worth, then six.

Try negotiating. You might find that your landlord will give you a discount or more time to pay, or that a creditor will agree to a repayment plan that you can afford.

Try selling some stuff. Yard sales, eBay, and Craigslist are effective ways to raise some quick cash without going into debt. Even pawn shops are a better option than payday loans.

Look for interest-free loans. Family or friends may be able to help. Some employers offer advances. And many local nonprofit and community groups have programs that offer interest-free emergency credit. If you have any retirement funds stashed away, you may be able to borrow from yourself. You risk having to pay fees or penalties if you don’t pay yourself back in time—not to mention undermining your retirement—but it may be a better option than paying triple-digit interest.

Seek out lower-cost loans. If you have to borrow from a financial company, look for types of lenders that charge less—hopefully much less—than payday storefronts. The best options, like home equity lines of credit, generally need to be set up well before you’re facing a shortfall. If you have access to a credit union, it may be able to offer relatively inexpensive, short-term loans, sometimes called Payday Alternative Loans (PALs) or Quick Loans.

Credit cards charge fairly high interest rates, with APRs ranging from the mid-teens to the mid-30s, but that’s far less than payday rates. Last, some traditional banks offer moderately priced installment loans as well; though generally more expensive than credit cards, they usually cost far less than payday loans.