Jennie Stout, a nurse in Ocala, Fla., was finishing an afternoon shift when she got a panicked call from home. Her 13-year-old daughter, Ashlyn, had tripped and fallen into smothered embers left over from burning leaves in their backyard, scorching her hands, knees, and shins.

Ambulance paramedics on the scene when Jennie arrived said that Ashlyn should be sent by helicopter to a burn center in Gainesville for fast treatment.

Jennie was surprised: The hospital was only about 40 miles away and the burns didn't seem extensive to her. But in that situation, she recalled, "I'm a mom first," so she didn't question the decision.

Ashlyn left the hospital after four days and was back at school within two weeks. The Stouts' insurer, Blue Cross and Blue Shield, covered her hospital bills and outpatient therapy.

But two months later, the family got another shock: A notice from Med-Trans, the air-ambulance company, telling them that the transport was $24,000.

It turns out that medical-emergency helicopters are often "out of network" and not fully covered by insurance. Blue Cross and Blue Shield paid only $5,700, leaving the family with the balance: $18,300.

Today, four years after the accident, Ashlyn has only a few minor scars. But the unpaid balance has a left a lasting mark on the family. They hired a lawyer to challenge the bill, which has now gone to a collection agency.

And the debt has hurt Jennie's credit score, making it more difficult to get a loan for needed repairs to the aging roof on the family's house.

"I have never not paid a bill in my life," Jennie says. "I am not paying a dime because on principle the whole thing is just wrong."

Related Articles

The Worst Kind of Surprise

Getting hit with a medical bill you thought insurance would pay is all too common (get more information at the end of this article).

And air-ambulance bills can be especially difficult. Consumer Reports—which collects patient stories about surprise medical bills—has seen a spike in complaints about air ambulances in the last year, including the Stouts'.

Consumers seem to have plenty to complain about. For one thing, the bills are expensive, averaging more than $30,000, research shows. And consumers have little recourse. Deregulation of the airline industry in the late 1970s left states unable to regulate air-ambulance services or to protect consumers from predatory practices.

The most frustrating part, according to industry experts we spoke with, is that many people taken by air ambulance could have been safely transported by ground ambulance.

In Ashlyn's case, although her burns were painful, they covered just 12 percent of her body. Patients less than 200 miles from a burn center with burns covering less than 30 percent of their body can usually be safely transported by ground, says Gary A. Vercruysse, M.D., a trauma specialist at the University of Arizona Medical Center who has written about the overuse of air ambulances.

Being taken by air ambulance may actually increase the risk of something else going wrong. They crash more often than other air taxis, research shows. That's partly because of poor decisions pilots may sometimes make when they feel pressure to transport patients quickly, says Ira Blumen, M.D., medical director of the University of Chicago Aeromedical Network, who researches air-ambulance accidents.

But Consumer Reports' analysis of data from the National Transportation Safety Board on air-ambulance accidents between 2010 and 2016 suggests another reason. We found safety differences between for-profit operators and nonprofits.

Patients Caught in the Middle

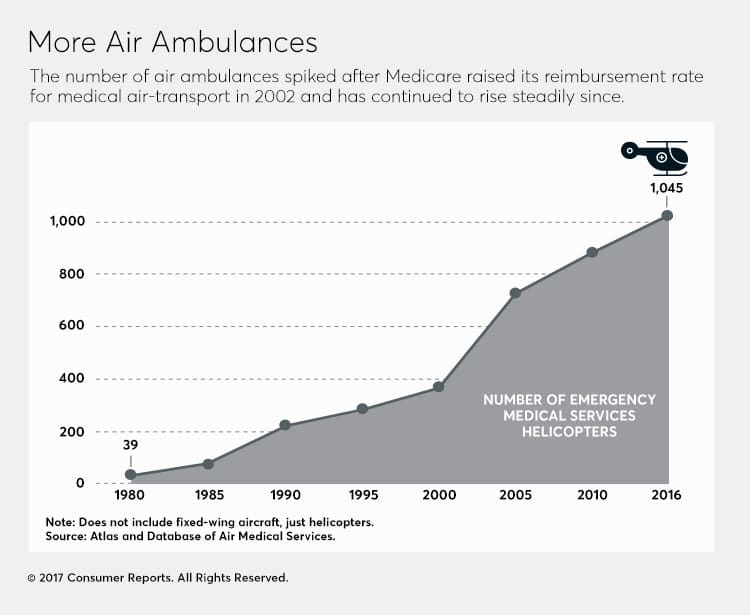

More than 1,000 air ambulances now operate in the U.S., twice as many as in 2000, according to industry data.

For-profit companies are a major factor in driving that expansion as they take over nonprofit programs run by hospitals and municipalities and buy up smaller operators. Today, four private air-ambulance companies—including Air Medical Group Holdings, which owns Med-Trans, the company that transported Ashlyn—account for half of the industry's revenue.

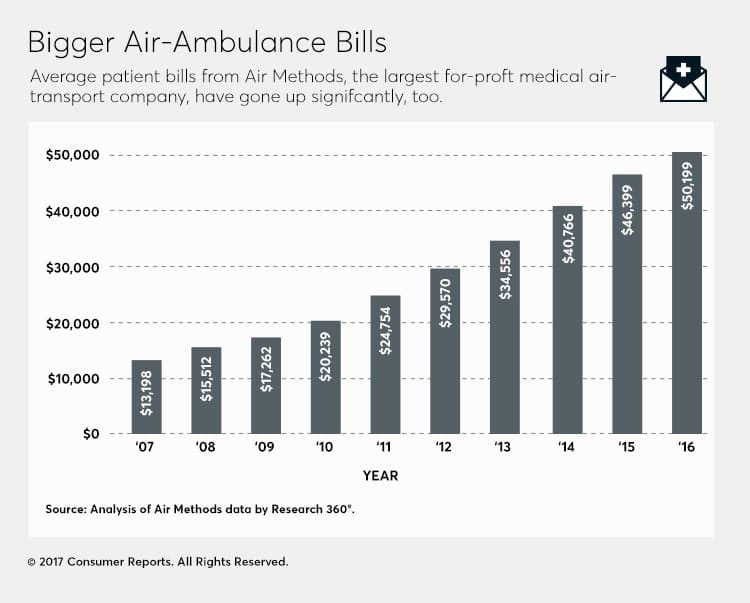

Bills for those services are growing. The average charge from Air Methods, the largest operator, rose from about $13,000 in 2007 to $50,200 in 2016, according to Research 360, an independent firm that tracks the industry. The average bill for the industry overall was $32,895 in 2014, the most recent year for which there is data.

The real cost of providing air transport averages about $7,000, according to Jon Hanlon, founder of Research 360. And analysis by New Mexico's Office of Superintendent of Insurance put the cost at an average of about $10,000.

Rick Sherlock, president and CEO of the Association of Air Medical Services, a trade group, says that many air-ambulance patients are on Medicare or Medicaid, and that those programs pay $200 to $6,000 per transport. So, Sherlock says, air-ambulance operators must collect more from people with private insurance to make up the difference.

As a result, patients who are privately insured are often stuck in the middle, paying the price for a dysfunctional system they have little control over.

An Unnecessary Cost?

When someone is traumatically injured and far from a hospital, air transport can be essential. And for people in rural areas, air transport may be their only hope in the event of a heart attack or other emergency.

But advocates and medical experts say that people with injuries that aren't life-threatening are too often flown when driving would be just as effective and much cheaper. "I see a lot of people brought by helicopter with very minor injuries," Vercruysse, a trauma surgeon who specializes in burn injuries, says. His March 2015 study in the Journal of Trauma and Acute Care Surgery concluded that almost one-third of air-ambulance rides weren't medically necessary.

In some cases, air ambulances are used even though it would be as fast—or faster—to go by ground. Ashlyn's father, for example, arrived at the hospital just as she was being wheeled into the ER, even though he drove a similar distance. The helicopter had been delayed as it looked for a safe place to land while Ashlyn waited in the ambulance.

Why the overuse? Many air transports occur when patients are transferred between hospitals, and some doctors, fearful of lawsuits due to a delay in care, resort to that option too often, Vercruysse says. Physicians and first responders need clearer guidelines on when an air ambulance is warranted, he says.

John Franchini, the chief regulator of insurance companies for New Mexico, says his office has seen an increase in consumer complaints about air ambulances, 12 of them from December 2015 to January 2017 alone. In six of those cases, insurance companies later determined the flights weren't medically necessary.

Billing consumers thousands of dollars for a service that they have no control over is wrong, Franchini says, especially if the service isn't needed.

High-Risk Flying

Then there's the issue of safety. The accident rate for medical helicopters has dropped in the past decade, according to Blumen's research. But they still crash at twice the rate of other air taxis, he says.

The National Transportation Safety Board says it recognizes the risks of these flights, citing, for example, the difficulty of flying at night, in unfamiliar terrain, or in bad weather.

And for-profit air-ambulance companies have a spottier safety record than nonprofit operators, according to a Consumer Reports analysis of recent NTSB data. We found that the four largest for-profit operators—Air Methods, PHI Air Medical, Air Medical Group Holdings, and Metro Aviation—accounted for 68 percent of industry accidents from 2010 to 2016 (37 out of 54 crashes), even though they account for 51 percent of the air-transport market.

Data from a 2014 study in the Journal of Trauma and Acute Care Surgery were even more lopsided. It found that of 139 crashes between 1998 and 2012, 118 involved for-profit operators. The authors said potentially preventable human errors related to the crashes are significantly higher among those operators. They attributed the increased risk to "deficiencies in training, reduced availability of equipment and resources, and questionable flight selection" among for-profit air-ambulance companies.

Sherlock from the Association of Air Medical Services says the study didn't take into account safety improvements, such as the installation of terrain awareness systems, directed by the Federal Aviation Administration in 2014. Though all of the regulations won't be fully implemented until 2018, he says many companies have voluntarily adopted many of those changes.

Consumers and Legislators Push Back

Consumers in at least five states who are suing Air Methods are seeking to turn their cases into class-action lawsuits. Several states have taken steps to help consumers facing high air-ambulance bills. There's also bipartisan support in Congress to investigate the problem and to give states more power to regulate the industry. Consumer Reports supports these efforts (see details below).

There's movement on the local front, too. Some local municipalities are taking back air ambulance services that had been outsourced. For example, in January, Monroe County in the Florida Keys, where the nearest trauma hospital is about 120 miles away, voted to expand its county-operated air-ambulance service after residents complained about bills from LifeNet, a private air-ambulance company owned by Air Methods.

Air Methods said in a statement that it bills only for what insurance won't cover as a last resort and that it works with patients to determine what they can reasonably pay.

Smart Steps to Battle Unwanted Bills

If you get stuck with a high air-ambulance bill, industry experts and consumer advocates say there are things you can do. Ask your insurance company to advocate on your behalf, or challenge the bill directly with the air-ambulance provider. To bolster your odds, file a formal complaint with the appropriate agency in your state government. Some air operators also offer charity-care programs.

To avoid these bills, you might want to consider a membership program offered by some air-ambulance operators, particularly if you live far from a hospital. The programs, which cost as little as $65 per year, are meant to cover costs that your insurance doesn't pay. But that works only if the ambulance company you sign up with is the one that arrives at your emergency, something you may have little control over.

As for the Stouts, they have exhausted their appeals and are now contemplating filing a class-action lawsuit. Jennie says she wishes she had questioned the need for an air ambulance the day her daughter was hurt. Her advice to others in a similar situation? "If it doesn't seem right, ask questions."

Protecting Consumers

Efforts to rein in excessive air-ambulance bills have rare bipartisan support in Congress.

Reps. Bill Shuster (R-Pa.) and Peter A. DeFazio (D-Ore.) recently asked the Government Accountability Office to investigate pricing and competition in the industry.

And Sens. Jon Tester (D-Mont.) and John Hoeven (R-N.D.) have introduced bills to give states more power to regulate how air ambulances operate and charge customers.

Consumer Reports supports those and other efforts to protect consumers from surprise medical bills.

"All Americans deserve access to affordable healthcare, including emergency medical transport," says Betsy Imholz, who oversees Consumer Reports' Surprise Medical Bills campaign.

Read more about our work on air ambulances. And learn more about our efforts to combat all surprise medical bills, and to share your story about one.

Editor's Note: This article also appeared in the May 2017 issue of Consumer Reports magazine.