Retirement planning has always been full of uncertainties: How much longer will you be able to work? How much savings will you have when you stop working? How many decades will that money need to last? But for anyone nearing retirement, or already there, the level of uncertainty has rarely been greater than it is right now.

Most significantly, Congress and the White House have been overhauling many rules that have a big impact on consumers generally and retirement savers in particular. One of the most sweeping changes is the new tax law that will greatly limit deductions and other breaks. That could have a major impact on your taxable income.

Investing is also more challenging. After a nine-year bull run, the benchmark Standard & Poor's 500 stock index is at record highs, so returns are likely to be lower in the years ahead. "There's a growing risk of a market correction in the future," says David Blanchett, director of retirement research at Morningstar, an investment research firm.

Don't let these worries paralyze you. "The most important thing people can do is control what is controllable," says Andrew Jamison, a certified financial planner with Main Avenue Financial Services in Beaverton, Ore. And the truth is, the things you can control—your day-to-day saving, investing, and planning decisions—are what's most critical to your retirement success.

Whether you are still working and plowing money into your 401(k), or enjoying your retirement now, here are smart strategies that will help ensure your financial security.

Below you can read about three phases of retirement planning, starting with when you're 50 to your early 60s, then from when you're 60 to your early 70s, and from when you're 70 and older.

Working and Saving: 50 to Early 60s

On average, men claim retirement benefits at age 64.2 and women at 64, Social Security data show. For nearly half, retirement comes sooner than expected, often because of poor health or a layoff, according to a 2017 report by the Employee Benefit Research Institute. But nearly a third of retirees leave their job because they can afford to. To improve the odds that you can retire on your own schedule, follow these steps.

Assess Your Assets

Add up your retirement savings to see whether you're on track to meet your retirement goals. As a benchmark, at 50 years old someone seeking to retire at age 65 should have stashed away the equivalent of 5.2 times their household income in financial assets, according to financial adviser Charles Farrell, J.D., LL.M., author of "Your Money Ratios" (2010, Avery). So if you're 50 years old and earning $100,000, having a $520,000 portfolio would leave you in good shape. (This calculation assumes you'll be living on about 80 percent of your preretirement income, including Social Security benefits.) Use an online tool, such as the T. Rowe Price Retirement Income Calculator, to see how your savings stack up.

Boost Your Savings

If you're falling behind on savings but you're still working, ramp up now by making the most of tax-advantaged retirement plans. Max out your 401(k) if you can—you can stash away as much as $18,500 in 2018; those 50 and older can put away $6,000 more in catch-up contributions.

Don't have an employer plan? Opt for an individual retirement account. You can save up to $5,500 per year in an IRA, plus a $1,000 catch-up contribution for those 50 and older. A traditional IRA lets you save pretax; a Roth IRA lets you put away after-tax dollars that grow tax-free. If you have any extra savings, put money in a taxable account.

Of course, saving more requires cutting back on your spending. But there's a double benefit to doing that, says certified financial planner Michael Kitces, director of wealth management at Pinnacle Advisory Group in Columbia, Md. By living a more frugal lifestyle, you not only free up savings but also won't need as much money to live on in retirement because your scaled-down spending has become your new normal. So consider downsizing your house now that the kids have moved out, or cook more at home rather than eating out. These savings will make reaching your retirement goals more doable.

Consider Your Longevity

If you need more incentive to save, think about how long your money will have to last in retirement—it could be two decades or longer. According to the Social Security Administration, the average 65-year-old man today is expected to live until 84.3, and a 65-year-old woman to 86.6. If you're a couple, one of you has a 47 percent chance of living until age 90.

Of course, average life expectancies won't tell you much about any individual—that's impossible to predict with any accuracy. Still, you can get a rough idea by running numbers at livingto100.com. The calculator there factors in data about your health and lifestyle. Most financial advisers typically plan for a retirement that lasts until age 90 or 95, Kitces says.

Understand Your Spending

Once you have a rough idea of how long your money will need to last, you can create a retirement budget. Start by tracking what you're spending now, using software such as Mint or YNAB. "Most people have no idea where their money is going," says Scott Cole, a certified financial planner in Birmingham, Ala., "so this process helps clarify."

With a budget in hand, you can think about ways that spending might shift in retirement. Many financial planners suggest you aim to replace 70 to 80 percent of your preretirement income, assuming that retirees usually spend less. But many people spend as much as they did before because of higher travel and entertainment expenses, especially in the early retirement years. Spending tends to drop off in the middle phase of retirement, only to rise in later years as healthcare expenses increase—a pattern that Morningstar's Blanchett calls the "retirement spending smile."

Design Your Retirement Life

"You need to understand that you are not just retiring from something but also retiring to something," Cole says. So take the time now to fine-tune your vision of retirement and share your ideas with your spouse to see whether you're on the same page. If you're dreaming of moving to a beach town, for example, test-drive that life in an extended vacation. And if you intend to volunteer or build a second career as a small-business person, join organizations or take courses in relevant topics so you can gain experience over the next few years.

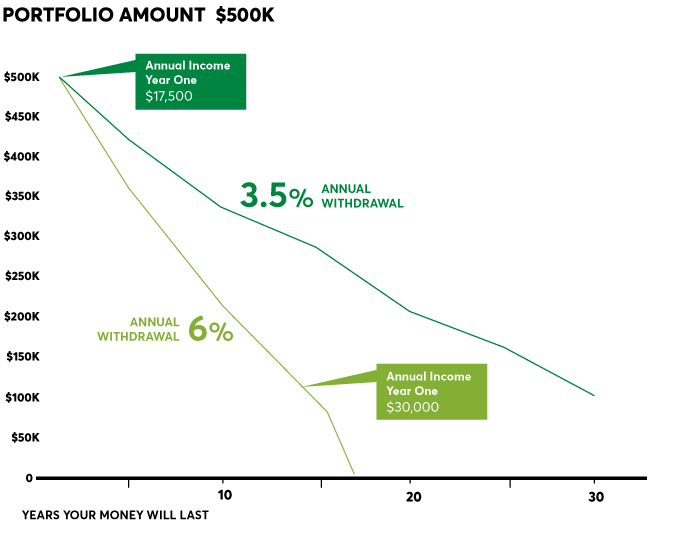

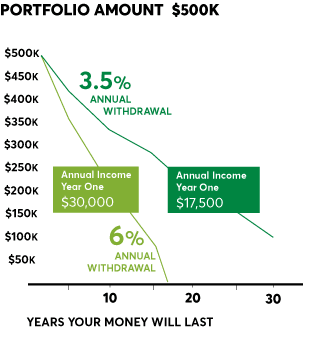

How Much Will You Have to Live On?*

The rate at which you take income from your savings can determine whether your money will last your lifetime—or not. This chart shows withdrawals from a $500,000 portfolio at different drawdown rates over 30 years.

Note: Both portfolios are assumed to be composed of 40 percent equities and 60 percent bonds, and resulting projections are based on benchmark returns. The initial withdrawal is set at a fixed percentage of the initial amount and is then inflation-adjusted annually over the period at 2.5 percent. Source: David Blanchett, director of retirement research, Morningstar.

Note: Both portfolios are assumed to be composed of 40 percent equities and 60 percent bonds, and resulting projections are based on benchmark returns. The initial withdrawal is set at a fixed percentage of the initial amount and is then inflation-adjusted annually over the period at 2.5 percent. Source: David Blanchett, director of retirement research, Morningstar.

Easing Into Retirement: 60 to Early 70s

As you close in on your retirement date, you have less time to recover from a financial setback. So make sure you have these bases covered.

Stress-Test Your Finances

How well would your retirement plan withstand a layoff or a market downturn? "It's important to think ahead about your options," says Anne Lester, head of retirement solutions at J.P. Morgan Asset Management. Run different scenarios on an online retirement calculator—using an earlier retirement date, lower returns, or the need to purchase health insurance prior to Medicare. A bad couple of years may not derail your finances if you can ratchet down your spending without giving up essentials. If not, you may want to work a year or two longer to avoid an uncomfortable encounter with a worst-case scenario. "People underestimate what a powerful lever delaying retirement can be," Lester says.

Review Your Social Security Options

There's another reason to consider putting off retirement: By claiming Social Security later, you can receive more in benefits. Between ages 62 and 70, for each year you delay filing, your payment increases by 6.5 to 8 percent a year. If you can bridge your finances before claiming for even a year or two, it can be worth it. "There aren't many other ways to get higher inflation-adjusted lifetime income," says Sheri Conklin, a certified financial planner in Roseville, Calif.

Granted, not everyone can put off claiming Social Security, and the decision gets more complicated when you factor in a spouse's benefits. So it can be smart to get help with this decision. One option is to use an online tool, such as the one at maximizemysocialsecurity.com ($40 per year) or socialsecuritysolutions.com ($50 for comparative reports), which provides customized advice. Or you may want to hire a financial adviser.

Reset Your Portfolio Risk Level

As you reach retirement, pay extra attention to the amount you keep in cash or short-term bonds vs. stocks. That's to protect against what's known as sequence of return risk: Poor stock returns early in retirement, combined with withdrawals to fund your expenses, raises the odds that you'll dangerously deplete your portfolio. Even if returns recover, you may not have enough savings left to catch up.

To avoid panic selling, build up cash in taxable accounts that can cover your expenses for a year or longer, says Harold Evensky, a certified financial planner with Evensky & Katz/Foldes in Lubbock, Texas. A 2013 study by Evensky found that having those reserves raised the odds that a nest egg would be as much as 6 percentage points higher at the 30-year retirement mark vs. not having that cash on hand.

Choose a Sustainable Withdrawal Rate

When figuring out how much money you can safely pull from your portfolio, one common starting point is the 4 percent rule—in your first year of retirement, take out 4 percent of the initial amount, then increase that amount by inflation each year to make your money last at least 30 years. Today a more prudent starting point may be 3.5 percent.

Living in Retirement: 70 and Beyond

Once you're retired, your main concern will be making sure your retirement income keeps flowing, especially if your health expenses rise. A recent survey by the investment firm Capital Group found that more than 4 out of 10 retirees were spending more than they expected on healthcare.

Mind Your RMDs

Starting in the year you turn 70 ½, the clock begins ticking on the required minimum distributions you must take from your 401(k) and individual retirement accounts, which has to happen by the end of that year. (You can defer your first RMD until April 1 of the next year, but you'll have to take a second one before year-end.) Miss an RMD and you'll pay a 50 percent penalty and taxes on the money you should have withdrawn. Your RMD amounts are based on the market value of your accounts and your life expectancy (and that of your spouse if he or she is the sole beneficiary and more than 10 years younger than you). RMD percentages increase as you age. A single 70-year-old with a $100,000 IRA portfolio, for example, would be required to withdraw $3,650, and an 80-year-old would have to take out $5,348. You can find RMD worksheets at irs.gov, and most brokerage firms will help you calculate the amounts.

Simplify Your Finances

Consolidating accounts at a single brokerage will make it easier to coordinate withdrawals, Kitces says. And your larger balance may qualify you for lower fees, which will boost your returns.

Editor's Note: This article also appeared in the March 2018 issue of Consumer Reports magazine.

*Correction: The "How Much Will You Have to Live On?" graphic has been updated to include the initial annual income in year one for a 6 percent withdrawal rate.