Before you throw away any more of the credit card offers landing in your mailbox, take note: You might be overdue for a credit card makeover. Adding a new card or two to your wallet can reward you for your spending or win you valuable new benefits, such as cell-phone insurance. Yet 20 million consumers have never changed their preferred credit card, and an additional 25 million have held on to their favorite card for at least 10 years, according to a 2016 CreditCards.com survey.

Among the most popular rewards is cash back for purchases. About half of all credit cards that offer rewards now offer cash back, up from around 25 percent in 2013. "Some of the cash-back credit card programs being offered today are the most lucrative we've ever seen," says Marc Bellanger, senior strategy director with Merkle, a marketing agency that works in the credit card and banking industry. (For non-cash-back cards with generous rewards, see "6 Cards With Other Benefits Worth Considering," below.)

Unlike cards that compensate you with points or miles that can be redeemed only for merchandise or travel, cash-back credit cards refund a percentage (typically 1 to 2 percent, but up to 6 percent) of your charges, usually in the form of a statement credit, a check, or a deposit into your bank account.

The way they work is simple, but finding the card that's right for you may not be. Some cards reward a flat rate back on all of your purchases; others give you a modest percent back on some categories of purchases and a higher percent back on others, such as gas or groceries. Sometimes the amount you'll get back changes each quarter. And some cards offer big bonuses if you spend a certain amount within the first few months. In terms of costs, there are cash-back cards that charge an annual fee and others that require you to maintain another account at a particular financial institution, so you also have to consider those possible costs.

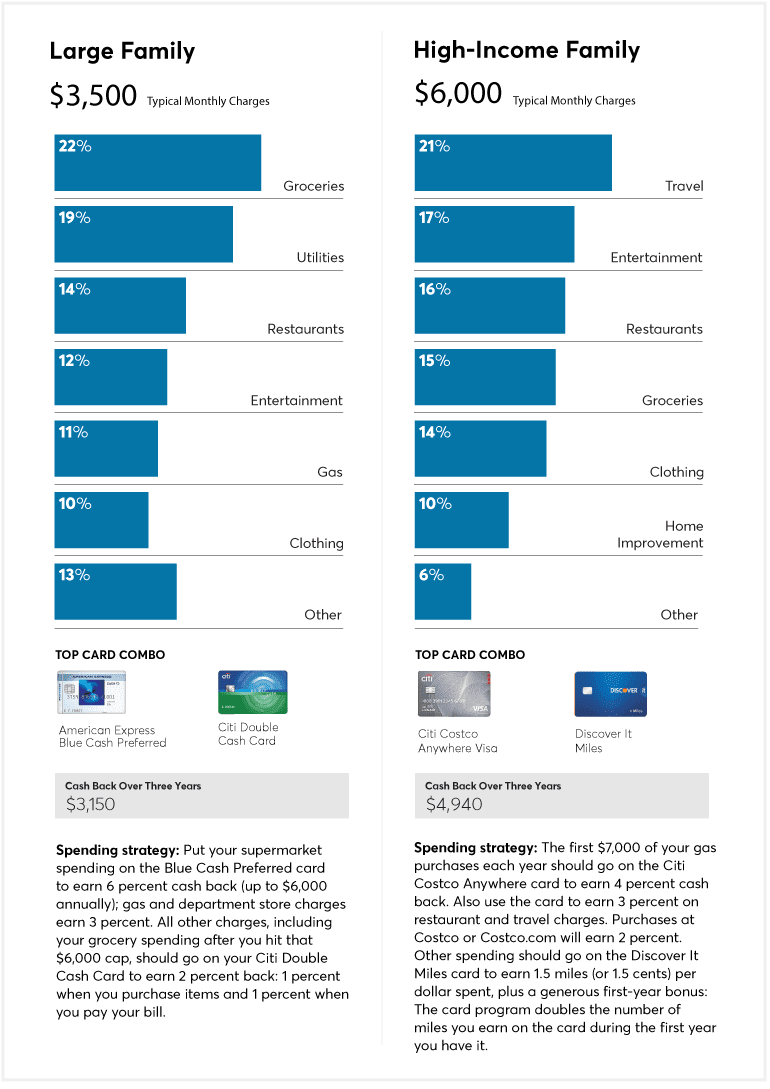

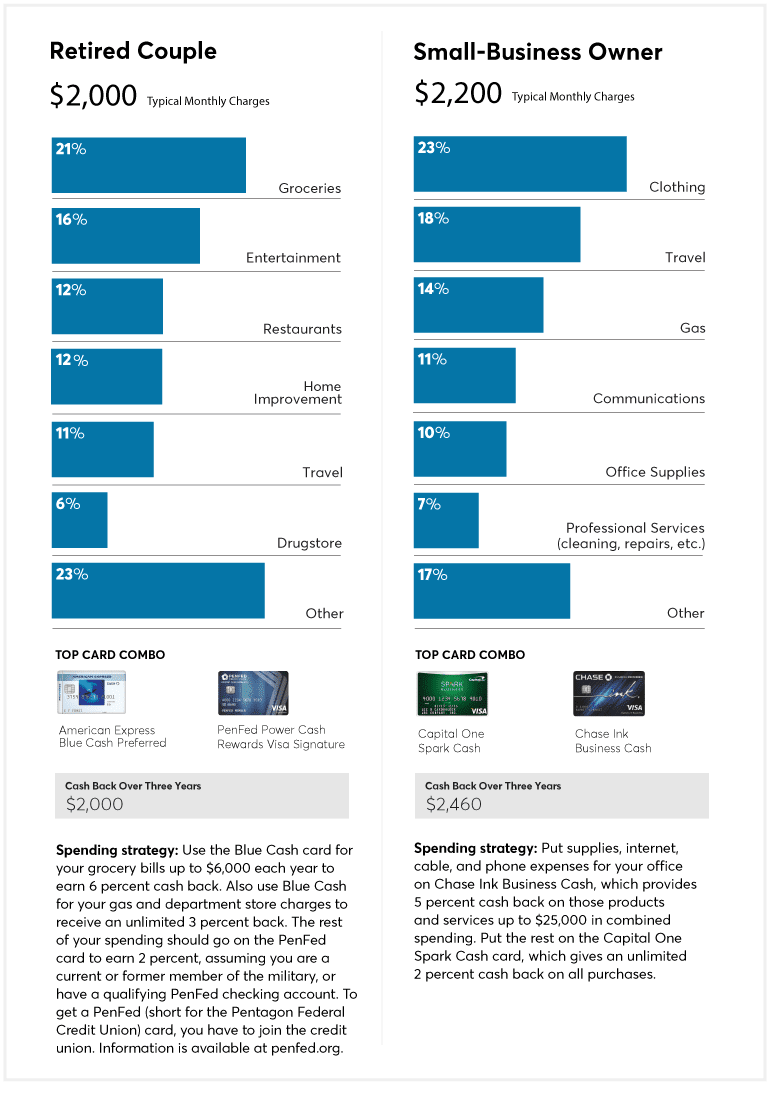

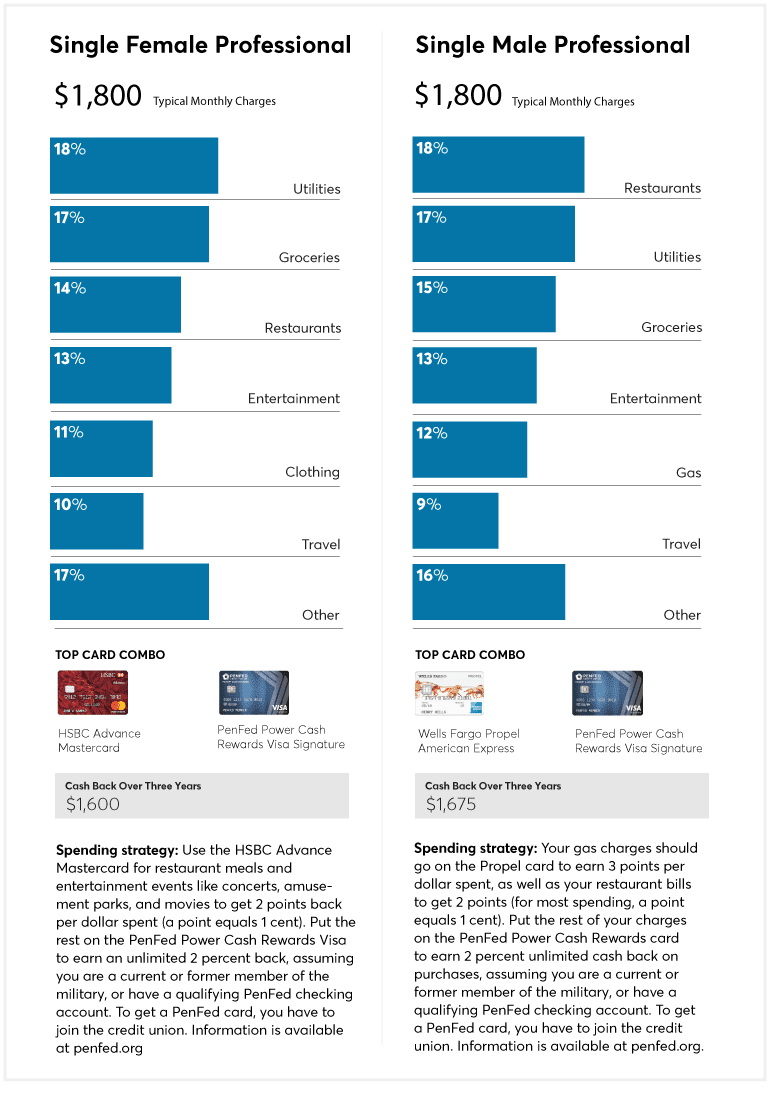

All of that research can be labor-intensive. To help make finding a more rewarding card less daunting, we used our proprietary credit card comparison calculator to review 83 rewards-card programs for six common spending scenarios based on data from the Bureau of Labor Statistics. And because we found that you can earn up to 40 percent more cash back by strategically using two cards instead of just one, we came up with card pairings that will increase your refund. (See "How to Stack the Cards in Your Favor," below.)

When Canceling a Credit Card, Use Caution

We evaluated the programs over a three-year period because certain cards offer a generous sign-on bonus but more limited rewards in subsequent years. We also assumed that cardholders don't carry balances (finance charges can swallow up any rewards). And in the case of cards that award points or miles but allow you to convert them to cash, we considered the actual dollar value of the rewards.

A few generous rewards cards came up more than once because they work well for more than one kind of spender.

We also provide a spending strategy for the two cards, because even the best pair is only as good as the way you use it. (To remind yourself which card to use for which purchases, keep a note in your wallet.)

For a more customized search for a cash-back card, try our easy-to-use Credit Card Adviser Comparison Tool, powered by a version of the software we used for this analysis.

The tool compares the benefits of cash-back cards and lists them in order of best to worst based on your actual spending data. It also estimates for each card the total cash back you'll receive after one year and after three years. To use the tool, first review your credit card statements to determine your total yearly spending on gas, groceries, restaurants, and travel. (The rest of your spending goes into one category that the tool calls Everything Else.) Then divide the totals by 12, plug in the monthly figures, and voila!, it will show you which credit card will pay you the most cash back in the first year and after three years. (Unlike the spending profiles below, our Credit Card Adviser Comparison Tool will recommend only one card, not a pair.)

Follow our guidance, and within a few months you'll see the cash start piling up.

6 Cards With Other Benefits Worth Considering

Cash back on purchases isn't the only smart reason to choose a card. Some cards provide other generous benefits—especially for travel and business—that could quickly offset the cost of any annual fee. Cards appear here in alphabetical order.

(If you're reading this article on your smartphone, we recommend you rotate your phone to landscape mode to better view the tables below.)

Update: Please note that the Credit Card Comparison Advisor Tool is not currently available.

How to Stack the Cards in Your Favor

To find a credit card pair that maximizes your cash-back rewards, pick the spending pattern that most resembles your own. (Note: Spending patterns are based on the top seven expenses for each consumer type. Data from Bureau of Labor Statistics. Some totals don't add up to 100 percent due to rounding.)

Editor's Note: This article also appeared in the September 2017 issue of Consumer Reports magazine.

Update: Please note that the Credit Card Comparison Advisor Tool is not currently available.