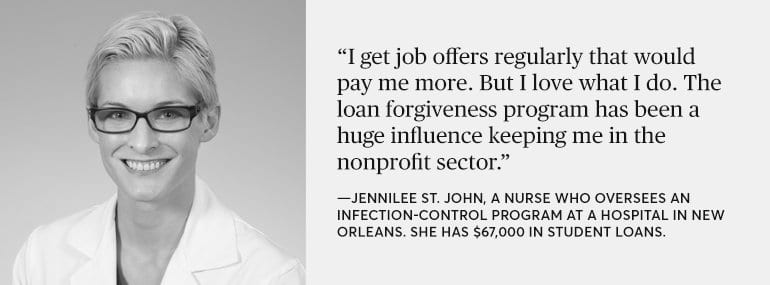

Jennilee St. John loves her work. A clinical nurse specialist, she oversees an infection-control program at a major medical center in New Orleans.

St. John, 30, made a big investment in her education to get where she is, taking out $58,000 in student loans to earn a master's degree in nursing in 2013. Though she says private-sector companies often try to tempt her away with much higher salaries, she plans to stay put at the nonprofit hospital.

Part of what keeps her there is the federal Public Service Loan Forgiveness Program (PSLF), which will wipe out your remaining student debt after 10 years of payments if you work in a qualifying public-service job and have remained current with your loan payments (more on how to qualify below).

St. John says PSLF was a major factor in her decision to get an advanced degree. "I knew I couldn't afford to take on the loans without it," she says. She has paid $14,000 on her loans so far, which have grown to $63,000 with interest, and hopes to have her portion of it paid off by 2023.

Millions Could Qualify

St. John is one of the more than 600,000 Americans who have signed up for the public service loan forgiveness program. But millions more could be eligible. Many are unaware of the program or are often given wrong information about it by the private companies that service their student loans.

It also can be difficult to navigate all of the program's different requirements. In some cases, people who thought they were enrolled in the program either didn't have the right type of loan or discovered that their job or payment plan didn't qualify.

The huge cost of the program, estimated to total $24 billion over the next 10 years according to the Congressional Budget Office, has also made it a target of the Trump administration, which has called for its elimination. Although nothing has been done yet, the uncertainty has left people like St. John worried about the future.

"I'm really afraid the program will go away and I'll be making these payments forever," says St. John. "I understand it was my financial responsibility to pay these loans when I signed on for them. But I have to think about my financial future." St. John says that if the PSLF program were cut, she would likely move into a private sector job so she could earn enough money to pay off the loans.

Missed Opportunities

The program marked its 10th anniversary in October, so only a small number of borrowers have met all the requirements to have their loans forgiven. But a 2015 report by the U.S. Government Accountability Office estimates that 4 million borrowers could qualify but don't know about the program.

Supporters of PSLF say the good the program does outweighs its cost. "It is a critical way to encourage people to work in the public sector and it's important for it to be protected," says Aaron Smith, co-founder of BySavi, a social impact startup which focuses on student loan consumer issues.

BySavi just launched a free tool called PSLF Checker, to help borrowers see if they qualify for the program. "The consumer information gap is the biggest challenge when it comes to this program," Smith says. "We want to try to fix that."

Servicer Woes

Much of the blame for why awareness of the program is low belongs to the companies that process the loan payments, known as student loan servicers, says Joshua Cohen, a consumer lawyer who specializes in student loan issues.

The servicers, private companies the Department of Education contracts with, are the main point of contact for people paying education debt. Servicers work with borrowers who are struggling to pay their loans.

Cohen says servicers aren't proactive about letting people know that PSLF is an option, or they give out incorrect information. "Servicers don't know or haven't been properly trained in how the program works," says Cohen. "They are there to make sure you pay your loan. They're not there to make sure you pay as little as possible and get your loans forgiven," says Cohen.

Servicers are facing increased scrutiny amid growing complaints about them. In a report issued in June, the Consumer Financial Protection Bureau looked at more than 11,000 education-loan-related complaints between March 2016 and February 2017 and found a wide range of problems regarding PSLF.

Borrowers reported that servicers give out inaccurate information about whether they qualify for PSLF, incorrectly process payments, and bungle job certifications needed to prove they work for a qualifying public sector organization.

In August, the attorney general of Massachusetts announced a lawsuit against FedLoan Servicing, the loan servicer that handles loans for borrowers seeking PSLF. The suit says FedLoan overcharged borrowers and prevented them from making qualifying payments that would put them on track for loan forgiveness.

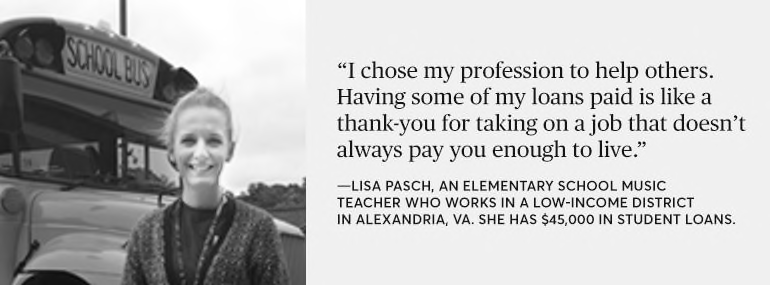

$45,000 in Debt and 7 Years to Go

Lisa Pasch, an elementary school music teacher in Alexandria, Va., knows too well about how servicers fall short. Pasch earned a bachelor's degree in music education in 2011 and a master's in choral music education in 2013.

She landed a job immediately at a school in a low-income district in Fairfax County. But with $45,000 in student loans and annual earnings of $55,000, she struggled financially.

Pasch contacted her loan servicer and on their advice consolidated her loans into one. She also switched to a graduated payment plan to stretch her payments out over 25 years instead of the standard 10-year payment plan. That reduced her monthly payment from $650 to $412.

Two years later, Pasch stumbled upon information about PSLF on online. But she realized that the graduated payment plan she chose when she consolidated her loans didn't qualify for the program. So she switched to an income-based plan that did.

Had the servicer had told her about PSLF when she consolidated, she says she'd be five years into meeting the requirement of 120 payments to get her remaining loan balance canceled instead of just two and a half years.

In the meantime, Pasch lives on a tight budget. She rarely travels or eats out. To help pay her bills, she works a second job as a fitness instructor. She didn't go home to visit her family in Memphis last Christmas because she couldn't afford the plane tickets.

Pasch will be 38 by the time she pays off her loans and estimates she'll be forgiven $15,000 to $20,000 of debt.

When that happens, "I could live a life like people do," says Pasch. "I chose my profession to help others. Having some of my loans forgiven is like a thank-you for taking on a job that doesn't always pay you enough to live."

It's too late for Cynthia Annis to benefit from PSLF even though she has worked as a social worker for the state of Texas the past 10 years. Annis, 66, went back to school later in life to get a degree in social work. She has nearly $30,000 in education loans but she knew about PSLF when she took out them out. Annis consolidated her loans after she graduated and hoped to have the remainder of her debt discharged by the time she retired next year.

Annis thought she was on track. Then, in August, when she contacted her servicer to find out what she needed to do to have the loans discharged, she was told the payment plan she chose doesn't qualify. Annis said when she consolidated her loans, she didn't think to ask that question.

"We thought we had all our ducks in a row for retirement," says Annis' husband Gary, who estimates that 20 percent of their retirement budget will go to loan payments. "She worked hard all those years making payments. It's not fair."

How to Qualify for Loan Forgiveness

If you think you might qualify for PSLF, here's what to do.

- Make sure you have the right type of loans: There are many different kinds of federal student loans, but only federal Direct Loans qualify for loan forgiveness. If you have another type of federal loan you may be able to consolidate it into a Direct Consolidation Loan to become eligible, but your previous loan payments won't count toward the 120 payments. If you don't know the type of loan you have, check the National Student Loan Data System. Student loans taken out privately don't count for loan forgiveness.

- Enroll in the right repayment plan: Income-driven repayment plans set the payments based on what you can afford on your income, which will reduce your monthly payment and maximize the amount forgiven. Other repayment plans, like extended or graduated repayment plans, don't qualify for public service loan forgiveness.

- Check if your job qualifies. You must work full-time—at least 30 hours a week—for a government agency or a qualifying nonprofit. Part-time work for several qualifying organizations can count too, as long as it adds up to 30 hours a week.

- Certify your payments. File an Employer Certification Form with your servicer every year or when you switch jobs to confirm that you are working for an eligible organization. The form is optional but it can flag problems early on. Your payments don't have to be consecutive—you just need to make an accumulated total of 120 on-time payments (i.e., no more than 15 days late).

- Keep good records: Keep copies of the certification forms and retain your W-2s that show proof of where you worked.

- Know where to get help. If you are having problems with your servicer, you can file a complaint online with the CFPB or by calling (855) 411-2372. The CFPB has a student loan ombudsman who monitors market trends and complaints and can be a resource to student borrowers and their families.

You should check in with your servicer regularly to make sure your payments are being tracked properly. "Unfortunately, this puts a lot of the burden on consumers," says Tobin Van Ostern, a co-founder at BySavi. "But when you have thousands of dollars in debt, it's worth it."