Now that the House and Senate have passed the $1.5 trillion tax bill, which President Trump is expected to sign into law soon, millions of Americans are wondering how the new rules will affect their finances.

In the near term, not a lot will change, since most provisions in the new tax law won't apply to your 2017 taxes. But your 2018 taxes may look quite different depending on where you live, whether you have kids, and other factors.

Among the major changes: The new bill nearly doubles the standard deduction and hikes the child tax credit. In addition, the deduction for state and local taxes and property taxes will be limited to no more than $10,000. And the mortgage interest deduction is limited to mortgage debt of no more than $750,000 vs. $1 million previously. (If you took out a mortgage before Dec. 15, 2017, you can still deduct interest on up to $1 million.)

What the GOP Tax Overhaul Means for Your Healthcare Costs

For most filers, these changes are likely to result in lower taxes for the next few years. A recent study by the Tax Policy Center, a research group, found that on average all income groups would see a tax cut in 2018 and 2025, the last year before the tax cuts for individuals expire.

That said, the wealthiest taxpayers will benefit most. In 2018, someone in the top 1 percent (income of $732,800 or more) would get an average tax reduction of $51,140, or an income boost of 3.4 percent, the Tax Policy Center found. By contrast, someone in the middle quintile (income between $49,000 and $86,000) would receive a tax cut of about $900, or 1.6 percent.

The big winners also include corporations, whose taxes will be lowered from the current top rate of 35 percent to 21 percent. That tax cut is permanent, while the individual tax breaks are scheduled to expire after 2025. As a result, by 2027 some 53 percent of filers would be paying more in taxes, according to the Tax Policy Center.

Those are just average numbers, of course, and they may not tell you much about how your family will fare under the new law. So we revisited our analysis of earlier versions of the tax bill, which looked at the impact of the rules on several specific but representative households, to see how things change under the final bill.

Once again we asked Phillip Schwindt, principal tax research analyst at Wolters Kluwer, a tax software and information company based in Riverwoods, Ill., to help us update the numbers for our hypothetical families.

These scenarios may offer insight into your own situation. And at the very least, you may get a better understanding of how the new tax law works and how it may affect your financial plans.

Download this PDF to see details of how we arrived at our figures.

How the Tax Law Could Affect You

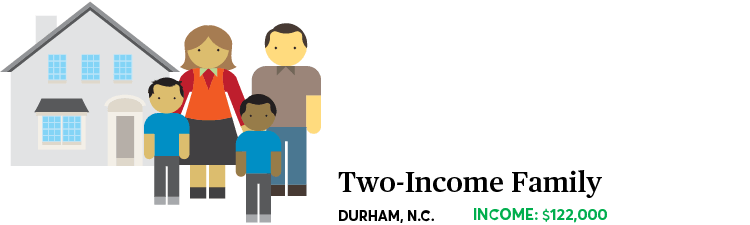

This married couple with two school-age kids would likely to see their taxes cut in half, despite losing their itemized deductions for mortgage interest, property taxes, and charitable contributions. That's mainly because they would benefit from the increased standard deduction and child tax credit.

| CURRENT TAX | $4,037 | ||

| NEW LAW | $1,939 | ↓ $2,098 | -52% |

Assumptions: Homeowners, ages 42 and 43, with two school-age kids. 401(k) contributions: $22,000. Dependent care flexible spending account contribution: $5,000. Investment income: $400. Property taxes: $3,900. Charitable contributions: $2,900. Mortgage interest deduction: $6,000. Child-care expenses $6,000. Annual tuition and fees: $10,500.

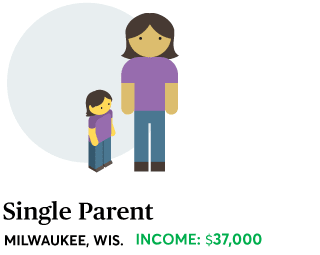

This head of household would get a refund under the new tax law, thanks mainly to the higher standard deduction, and the larger child tax credit.

| CURRENT TAX | $649 | ||

| NEW LAW | -$536* | ↓ $1,185 | -183% |

Assumptions: Single parent, age 27, with one school-age child, renting a home.

*Refund

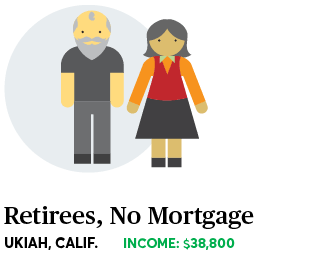

This couple pays no federal income tax now, which is the financial situation for some 44 percent of Americans, according to the Tax Policy Center. Under the new tax law, nothing would change for these retirees.

| CURRENT TAX | $0 |

| NEW LAW | $0 |

Assumptions: Married couple, ages 72 and 74. Social Security income: $25,900. Pension income: $9,400. IRA income $5,900.

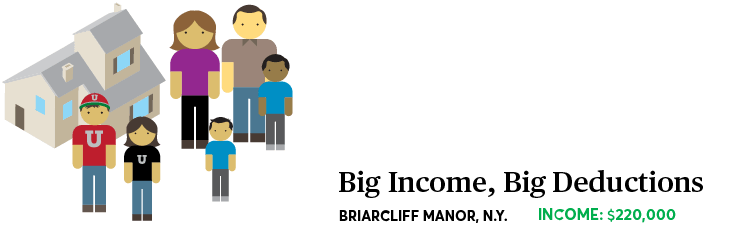

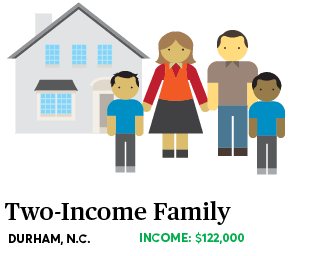

This family, which has relied on lots of deductions and personal exemptions, would see a slight increase in taxes next year. The new law would allow them to write off only $10,000 of their $22,000 property tax bill and $9,700 state income tax bill. Still, the family will benefit from no longer owing the Alternative Minimum Tax—the law limits the impact of this parallel taxation system, so fewer people will have to pay AMT. The new tax brackets also hold down this family's tax bill, since the bulk of their income will be taxed at a 22 percent rate rather than 25 percent.

| CURRENT TAX | $23,082 | ||

| NEW LAW | $23,675 | ↑ $593 | + 2.6% |

Assumptions: Married couple, ages 48 and 51, filing jointly, with two school-age kids. The 51-year-old spouse works. 401(k) contributions: $24,000. Dependent-care flexible spending account contribution: $5,000. Medical flexible spending: $2,500. Long-term capital gains: $10,000. Charitable contributions: $5,700. Property taxes: $22,000. Mortgage interest: $16,000.

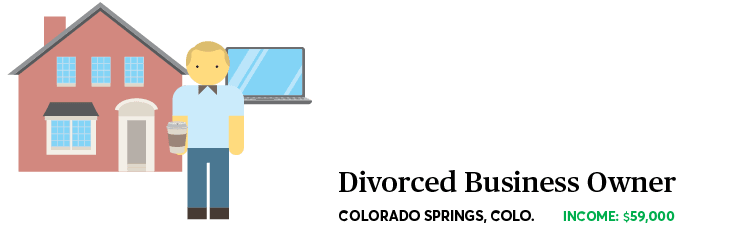

This business owner would be able to take a new business income deduction under the new law. But because he is no longer allowed to deduct his student loan debt or alimony payments, he will end up paying more in taxes.

| CURRENT TAX | $10,260 | ||

| NEW LAW | $11,620 | ↑ $1,360 | + 13.3% |

Assumptions: Divorced taxpayer with $59,000 in net self-employment income. Long-term capital gains: $600. Student loan interest: $950. Property taxes: $800. Charitable contributions: $2,200. Mortgage interest: $6,228. Uses Roth IRA for retirement savings. Alimony/spousal support payments: $18,000/year.

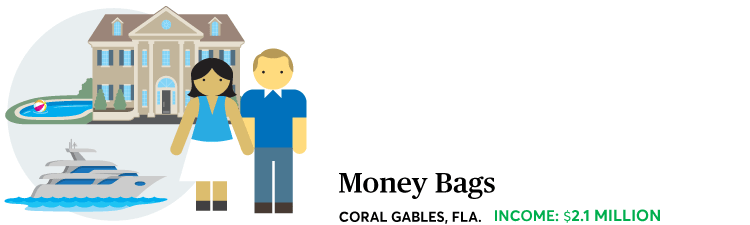

This couple, who earn most of their income from investments in a small business partnership, or "pass-through" entity, would end up paying far less in taxes. Under the new tax law, they will be allowed to exclude 20 percent of their pass-through business income, subject to certain limitations, from taxation.

| CURRENT TAX | $753,507 | ||

| NEW LAW | $595,311 | ↓ $158,196 | -21% |

Assumptions: Married couple, ages 60 and 62, no dependent children. One works. Wages: $500,000; pass-through income: $1,600,000. (For this example, "reasonable compensation" was not considered in determining the income amount upon which the pass-through tax was determined.) 401(k) contribution: $24,000. Long-term capital gains: $25,000. Interest income: $28,000. Sales tax: $2,818. Property taxes: $30,000. Charitable contributions: $70,000. Mortgage interest: $35,000; assumed attributable to $1 million mortgage debt incurred in 2018. All of the business income is non-passive. Business income deduction is $250,000, based on the assumption that the business paid $500,000 in qualified wages and the deduction was limited to 50 percent of the $500,000 in wages paid.

The new tax law will lower the medical-expense deduction threshold for the next two years to 7.5 percent of adjusted gross income, down from 10 percent currently, which will make it easier to itemize. That will help with this widow's assisted-living bills. But the elimination of the personal exemption means that her taxes still rise.

| CURRENT TAX | $679 | ||

| NEW LAW | $923 | ↑ $244 | + 36% |

Assumptions: Widow, age 88. Long-term care expenses: $59,300. Health insurance and other medical expenses: $5,000. Social Security: $24,000. Pension and interest income: $48,000.

Phillip Schwindt, principal tax research analyst, and Mark Luscombe, principal analyst, tax and accounting, at Wolters Kluwer Tax &Accounting; Steven Garcia, CPA; Michael Kresh, CFP; Robinson & Henry P.C.; Internal Revenue Service; United States Census Bureau; City-Data.com; Economic Policy Institute; Social Security Administration; Pension Rights Center; HSH.com; Zillow.com; Avalara.com; U.S. Government Accountability Office; Genworth.

ILLUSTRATIONS: CHRIS PHILPOT

<

<This married couple with two school-age kids would likely to see their taxes cut in half, despite losing their itemized deductions for mortgage interest, property taxes, and charitable contributions. That's mainly because they would benefit from the increased standard deduction and child tax credit.

| CURRENT TAX | $4,037 | ||

| NEW LAW | $1,939 | ↓ $2,098 | -52% |

Assumptions: Homeowners, ages 42 and 43, with two school-age kids. 401(k) contributions: $22,000. Dependent care flexible spending account contribution: $5,000. Investment income: $400. Property taxes: $3,900. Charitable contributions: $2,900. Mortgage interest deduction: $6,000. Child-care expenses $6,000. Annual tuition and fees: $10,500.

This head of household would get a refund under the new tax law, thanks mainly to the higher standard deduction, and the larger child tax credit.

| CURRENT TAX | $649 | ||

| NEW LAW | -$536* | ↓ $1,185 | -183% |

Assumptions: Single parent, age 27, with one school-age child, renting a home.

*Refund

This couple pays no federal income tax now, which is the financial situation for some 44 percent of Americans, according to the Tax Policy Center. Under the new tax law, nothing would change for these retirees.

| CURRENT TAX | $0 |

| NEW LAW | $0 |

Assumptions: Ages 72 and 74. Social Security income: $25,900. Pension income: $9,400. IRA income: $5,900.

This family, which has relied on lots of deductions and personal exemptions, would see a slight increase in taxes next year. The new law would allow them to write off only $10,000 of their $22,000 property tax bill and $9,700 state income tax bill. Still, the family will benefit from no longer owing the Alternative Minimum Tax—the law limits the impact of this parallel taxation system, so fewer people will have to pay AMT. The new tax brackets also hold down this family's tax bill, since the bulk of their income will be taxed at a 22 percent rate rather than 25 percent.

| CURRENT TAX | $23,082 | ||

| NEW LAW | $23,675 | ↑ $593 | + 2.6% |

Assumptions: Married couple, ages 48 and 51, filing jointly, with two school-age kids. The 51-year-old spouse works. 401(k) contributions: $24,000. Dependent-care flexible spending account contribution: $5,000. Medical flexible spending: $2,500. Long-term capital gains: $10,000. Charitable contributions: $5,700. Property taxes: $22,000. Mortgage interest: $16,000.

This business owner would be able to take a new business income deduction under the new law. But because he is no longer allowed to deduct his student loan debt or alimony payments, he will end up paying more in taxes.

| CURRENT TAX | $10,260 | ||

| NEW LAW | $11,620 | ↑ $1,360 | + 13.3% |

Assumptions: Divorced taxpayer with $59,000 in net self-employment income. Long-term capital gains: $600. Student loan interest: $950. Property taxes: $800. Charitable contributions: $2,200. Mortgage interest: $6,228. Uses Roth IRA for retirement savings. Alimony/spousal support payments: $18,000/year.

This couple, who earn most of their income from investments in a small business partnership, or "pass-through" entity, would end up paying far less in taxes. Under the new tax law, they will be allowed to exclude 20 percent of their pass-through business income, subject to certain limitations, from taxation.

| CURRENT TAX | $753,507 | ||

| NEW LAW | $595,311 | ↓ $158,196 | -21% |

Assumptions: Married couple, ages 60 and 62, no dependent children. One works. Wages: $500,000; pass-through income: $1,600,000. (For this example, "reasonable compensation" was not considered in determining the income amount upon which the pass-through tax was determined.) 401(k) contribution: $24,000. Long-term capital gains: $25,000. Interest income: $28,000. Sales tax: $2,818. Property taxes: $30,000. Charitable contributions: $70,000. Mortgage interest: $35,000; assumed attributable to $1 million mortgage debt incurred in 2018. All of the business income is non-passive. Business income deduction is $250,000, based on the assumption that the business paid $500,000 in qualified wages and the deduction was limited to 50 percent of the $500,000 in wages paid.

The new tax law will lower the medical-expense deduction threshold for the next two years to 7.5 percent of adjusted gross income, down from 10 percent currently, which will make it easier to itemize. That will help with this widow's assisted-living bills. But the elimination of the personal exemption means that her taxes still rise.

| CURRENT TAX | $679 | ||

| NEW LAW | $923 | ↑ $244 | + 36% |

Assumptions: Widow, age 88. Long-term care expenses: $59,300. Health insurance and other medical expenses: $5,000. Social Security: $24,000. Pension and interest income: $48,000.

Sources: Phillip Schwindt, principal tax research analyst, and Mark Luscombe, principal analyst, tax and accounting, at Wolters Kluwer Tax & Accounting; Steven Garcia, CPA; Michael Kresh, CFP; Robinson & Henry P.C.; Internal Revenue Service; United States Census Bureau; City-Data.com; Economic Policy Institute; Social Security Administration; Pension Rights Center; HSH.com; Zillow.com; Avalara.com; U.S. Government Accountability Office; Genworth.

ILLUSTRATIONS: CHRIS PHILPOT

Editor's Note: For the most part, these scenarios are based on average figures for income, home prices, and other factors, provided by the Internal Revenue Service, the Bureau of Labor Statistics, and other sources. In these examples we assume that each household has private health insurance, except for the retired couples, who are insured by Medicare.