Buying solar panels requires an investment and more decision-making than leasing, but over the long term the benefits of owning your system are hard to beat.

Best Ways to Pay for Your Panels

Cash

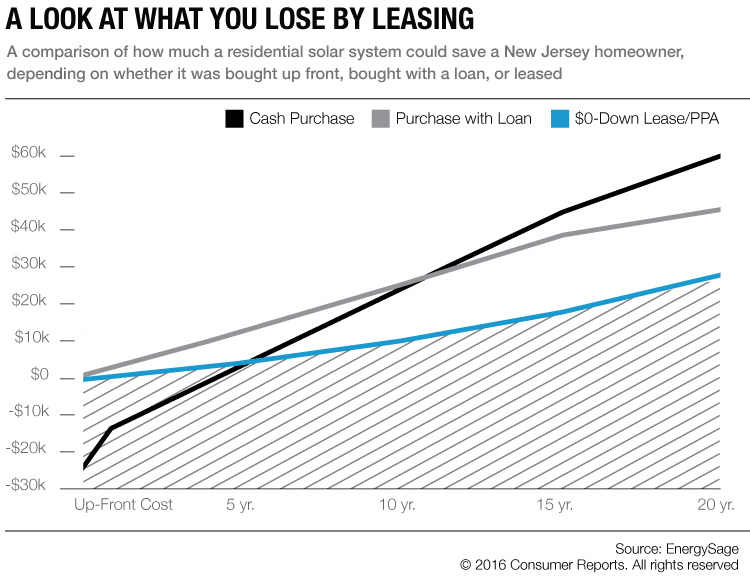

Buying your solar electric system outright is best. It usually costs $15,000 to $20,000 after tax credits and can reduce your electricity bill by 70 to 100 percent, depending on the size and orientation of your roof and local regulations. Most systems pay for themselves in five to seven years.

Home Equity Loan

If you need to finance your solar panel purchase, the most cost-effective way to do it is to use a home equity loan or a home equity line of credit. Because your house serves as collateral, these options have low interest rates (currently about 3 to 5 percent). The interest you pay is tax deductible. Equity loans range from 5 to 20 years and usually have fixed interest rates. Equity lines last 10 years and have variable rates (so the interest may increase).

Solar Loan

There are unsecured and secured solar loans. With an unsecured loan, your house doesn't act as collateral and the interest isn't tax deductible. Many solar installers work with lenders that offer solar loans, but you'll probably find better rates by directly checking with banks, and credit unions. Watch out for high origination fees. Fannie Mae also offers consumers financing for solar system installations through its HomeStyle Energy Mortgage Program when they buy a new house or refinance.

Why Leasing Isn't a Bright Idea

The steep up-front costs for a residential solar system can make a leasing company's sales pitch sound pretty appealing: Pay little or nothing and save hundreds of dollars per year on average. (The premise is that you save because the combination of your lease payment and your electric bill is less than what you currently pay for power.) Leasing can also look seductively simple compared with buying: There's no need to shop separately for an installer and financing; you just sign on the dotted line. So it's not surprising that 72 percent of the people who installed residential solar systems in 2014 did so through leasing or another type of third-party arrangement. But the reality is not quite so sunny.

Your Savings Will Be Modest

People who lease their solar systems save far less than those who buy them outright or with a loan (they also miss out on federal tax benefits and any local incentives). Many leases contain an escalator clause that can further reduce savings by increasing payments 3 percent per year. So if you're paying 12 cents per kilowatt-hour in year one, with a 3 percent escalator, you'll be paying 18.2 cents in year 15. That means that if the cost of energy doesn't rise as quickly as the contracted lease payments increase, your savings could evaporate.

You Lose Control of Your Roof

Leasing companies want to maximize their profit, so there's a chance you could wind up with more panels than you want and that they could be installed in highly visible places—such as facing the street—without any regard to appearance. To avoid that, check the final system design and placement before signing the lease. It could be different from the initial mock-up.

Leases Can Scare Off Home Buyers

If you put your house on the market before the lease is up (usually 20 years), you will either have to buy out the lease or the person purchasing your home will have to assume it—which some are reluctant to do.

That's what happened to Andrew and Nora Barber, who had to buy out the lease on the solar system on their Clovis, Calif., home after two prospective buyers were frightened away by it. "I offered the solar company $16,000, which was the total of all the payments for the remainder of the contract," Andrew says. "But $21,000 was the buyout price in the contract, and the company wouldn't budge."

Some solar leasing companies may offer to relocate their systems from one house to another. That could cost $500 for an initial audit and another $500 to transfer the panels, if the leasing company determines it can be done. You would also need approval from your utility and local landmarks commission or the condo or homeowner's association, if applicable. Plus the new house must be able to accommodate the old system.

And remember: At the end of the lease, the solar company could remove the system—and your savings along with it.

Service Plans Don't Serve You

Though leasing companies tout their service plans, maintenance is a red herring. "Generally, there's really no scenario where the maintenance plan is going to kick in," says Joshua Pearce, an engineering professor and solar expert at the Michigan Tech Open Sustainability Technology Lab. Equipment problems aren't covered by the maintenance plan, they're covered by the warranty. And if a storm destroys your panels, the damage may be covered by your homeowners insurance.

That's why—whether you buy or lease—it's essential that you inform your insurer. (Roof-mounted solar is generally added as part of a standard homeowners policy at no additional cost; ground-mounted solar may require an insurance rider.)

More on Alternative Energy

Editor's Note: This article also appeared in the August 2016 issue of Consumer Reports magazine.