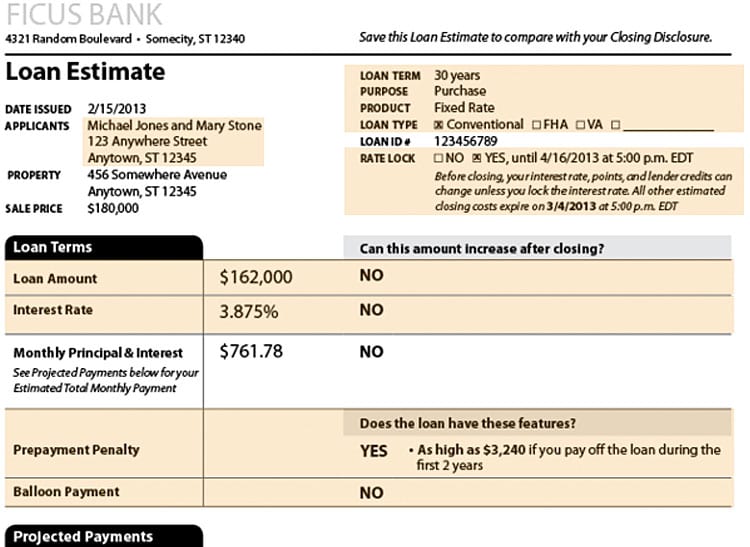

Shopping for a mortgage became easier in early October when the Consumer Financial Protection Bureau began mandating that lenders provide a new, simplified disclosure form to help consumers compare home loans. This disclosure (see below) is most useful after you've found the home you want and need a solid estimate of borrowing costs from a variety of lenders.

But before you get to that stage, you'll need to prove to a seller that a bank will lend you what you need to close on the deal. To avoid miscommunication snarls, you have to understand the difference among lender guarantees.

The Prequalification

A prequalification is really just to get you started, so you have a ballpark idea of how big a mortgage you can afford.

When a bank prequalifies you, it's giving you a preliminary statement of how much you could borrow, based on income and asset information you've provided. It is not based on any hard evidence, because at this point, you haven't given your bank statements or had bank officers request your credit report. (For more information about the prequalification process, watch this Chase Bank video.)

The Preapproval

When the bank tells you you're prequalified, it may ask for your employer's name and your Social Security number to verify your income and creditworthiness, as indicated by your credit reports. That's to start the mortgage preapproval process.

A bank will issue a mortgage preapproval once it has all your documents in hand. These could include income verification from employers, recent tax returns, bank and brokerage statements, and credit reports. The bank will then have a specialist call an underwriter to determine how much you're capable of paying and how big a mortgage loan you can afford. That assessment will result in a preapproval letter from the lender that you can present when you bid for a home.

Having a preapproval in hand gives you a jump on other potential buyers. It lets the seller know you're a good candidate, and that the bank is likely to award you a loan. It'll also make you feel more prepared to buy.

However, complicating matters, banks don't always define the terms in the same way, according to the Consumer Financial Protection Bureau. EverBank, the online lender, for instance, doesn't use the word, "prequalification." Instead, it uses the term "preapproval" for what other banks define as prequalification. And what most banks call a "preapproval" EverBank terms a "credit only approval," which means it has verified your income and creditworthiness.

Keep in mind that you're not required to borrow from the bank that issues your prequalification or preapproval.

How to get started mortgage-shopping

Consider these tips before you shop for a home or mortgage:

• Understand what the bank means by preapproval and other terms, and properly communicate to the seller or seller's agent the type of approval you have in hand.

• Months before you apply for mortgage preapproval, get at least one of your credit reports. This will allow you to troubleshoot any errors in advance of a bank's review. You are each entitled to a free credit report from each of the three credit reporting agencies—Equifax, Experian, and TransUnion—once a year; go to AnnualCreditReport.com, the official, federally-authorized site managed by the three agencies. Your spouse or partner should pull his or her reports as well. We recommend staggering requests so you get one of the three every four months. That way, you can be generally on top of problems.

• When shopping for mortgages, don't worry that your credit score will take a hit due to multiple inquiries by mortgage lenders. Normally, multiple inquiries can affect your credit score, but the three credit reporting agencies consider multiple inquiries in a short period of time for the same reason—in this case, mortgage shopping—as if they were one inquiry.