How to Shop for a Car Loan

Follow these 9 expert tips to get the lowest interest rate and monthly payment

Whether you’re buying a new car or a used one, there are always ways to get a better interest rate on a loan.

Consumer Reports consulted experts to give you the best advice on how to find the best loan. Read on to see what they said.

Review Your Credit Report and Credit Score

Typically, a higher credit score means you’ll get a lower interest rate. The opposite is true for those with lower credit scores. That’s because a good score, which is based on a history of paying bills and debts, indicates to lenders that you’re more likely to pay bills on time and in full. But a study Consumer Reports conducted a few years ago found that even people with good credit scores can sometimes pay too much for auto loans.

Improve Your Score

This is especially important if you’ve had credit problems in the past. Sometimes improving a low score is as simple as correcting mistakes or discrepancies in your credit report. Most corrections and disputes are completed in 10 to 14 days, Takeyama says, and credit reporting agencies generally must complete their investigations within 30 days. Paying down existing debt can also give you a last-minute bump. As always, pay bills for credit cards, utilities, and other companies promptly to avoid late fees and further damage to your credit score.

Set a Budget and Stick to It

As the staffers who buy CR’s test cars know, car dealers can be masters of the art of upselling. Consider your needs today and how they may evolve. Resist the urge to indulge in extras or buy a bigger or fancier vehicle than you need because you’ll probably pay on that depreciating asset for years to come through a loan, car insurance, and potential local vehicle taxes.

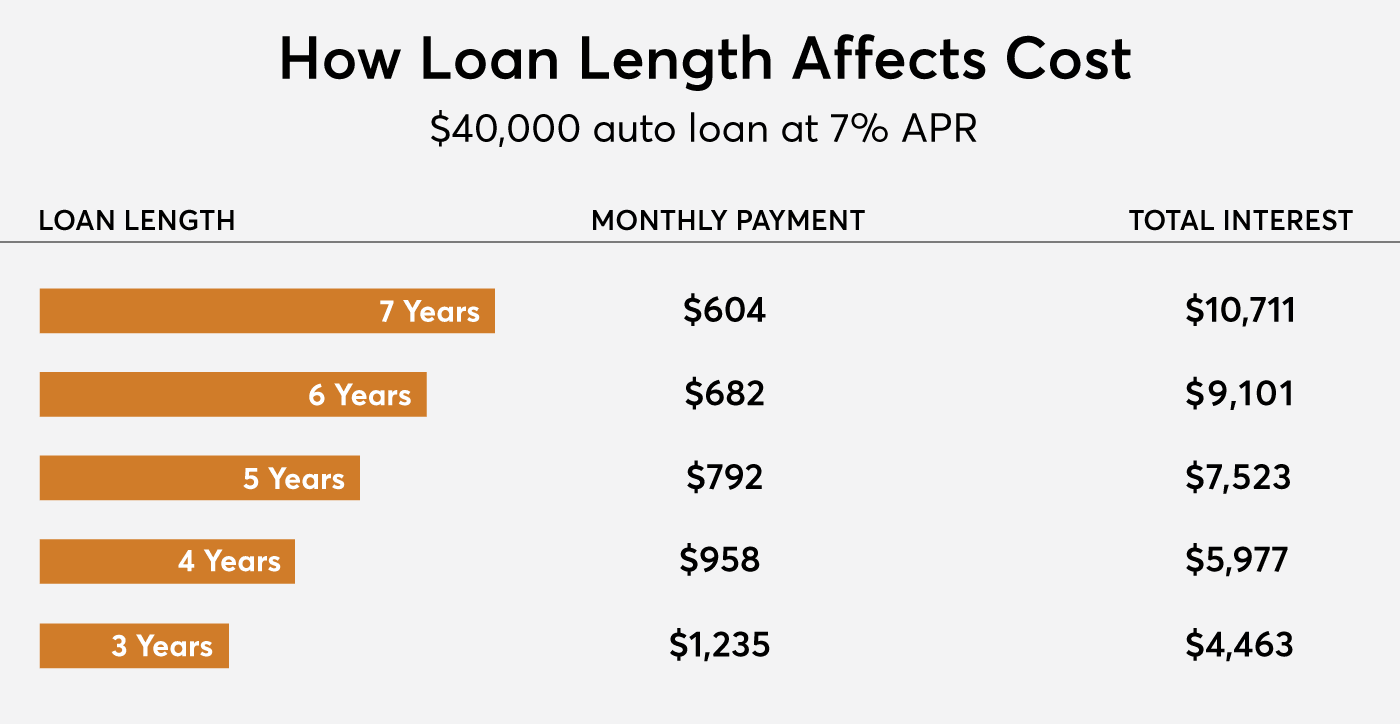

Don't Focus on Just the Monthly Cost

Dealers often try to sell you on a loan by emphasizing what you will have to pay each month. While that’s important for household budgeting purposes, to secure low monthly payments, you’ll most likely have to extend the loan over a longer period. One drawback of this is that the overall cost of the loan will increase. Another downside to a long-term loan is that it increases the chance that you will end up “underwater” or “upside down” on your loan. This is when you owe more on the car than what it’s worth. Of course, a monthly cost that you can afford is also important, so consider both factors when choosing a loan.

The example below explains how longer loan terms lower your monthly payment but increase the overall cost.

Make the Biggest Down Payment You Can

That shortens the time you’ll be paying interest on the loan, says Alain Nana-Sinkam, co-founder of Remarkit Automotive, a firm that analyzes market trends. Putting down more money up front also means you’ll be paying interest on a smaller amount, which will result in lower overall costs.

“With interest rates trending higher, CR recommends that buyers make a down payment of at least 15 percent when buying a vehicle, and 20 to 25 percent if you can afford it,” says Chuck Bell, programs director for advocacy at Consumer Reports.

Get Preapproval From Your Bank

Before you set foot in a dealership—either physically or virtually—contact your bank or credit union and get preapproved for a loan. The dealer may be able to offer a better deal on financing, but having a loan secured ahead of time gives you a strong starting point for negotiating financing terms.

If Your Credit Isn't Great, Check Carmakers for Special Deals

Sometimes automakers or their dealers will offer special financing for subprime borrowers, although it’s usually focused on entry-level models. Nana-Sinkam says that while buying a used car will likely decrease the amount of your loan, some subprime lenders may favor new-car loans because the cars have robust warranties, making it less likely that mechanical problems will make it more difficult for the borrower to pay on time. Bell says that, like anyone else, subprime borrowers should shop around. “Oftentimes, the best rate is going to come from a credit union, bank, or third-party lender, rather than from dealer-based financing,” he says. “Know what the prevailing interest rates are for borrowers in your credit score range, and seek multiple offers before heading to the dealership.”

Consider Buying a Used Car

CR members report higher levels of satisfaction with newer used cars, but you can save money by buying an older model. Although interest rates tend to be higher on loans for used cars, lowering the amount you’re borrowing can result in significant savings. But beware: Interest rates can be significantly higher at some used-car lots, especially so-called “buy here, pay here” dealerships, according to research from the Consumer Financial Protection Bureau.

Stop Overcharging for Car Loans!

Sign CR’s petition to the Consumer Financial Protection Bureau to ensure that auto loans are fairly priced.

Report Suspected Discrimination

Black and Hispanic borrowers with the same creditworthiness as white ones pay almost 1 percentage point more interest on car loans, according to a 2021 study. The study also found that borrowers of color were slightly more likely to be denied a loan outright. If you suspect discriminatory lending, file a complaint with the Consumer Financial Protection Bureau or the Federal Trade Commission.

More on Car Insurance

• CR’s Car Insurance Ratings and Buying Guide

• Best Car Insurance Companies

• Cheapest Car Insurance Companies

• How to Lower Your Car Insurance Rates

• Best Car Insurance Companies for Seniors

• Everything You Need to Know About Teen Car Insurance

• Proven Ways to Save on Car Insurance Even If You’re a Safe Driver

• How to Keep Your Car From Getting Stolen

• How to Prevent Catalytic Converter Theft