Sign In

Prepaid cards are no longer just for people who don't have bank accounts. They're the fastest-growing payment method in the U.S., and they're attracting those who want to budget their spending. And our new report has some positive news for consumers: Fees have declined, and many prepaid cards offer more features.

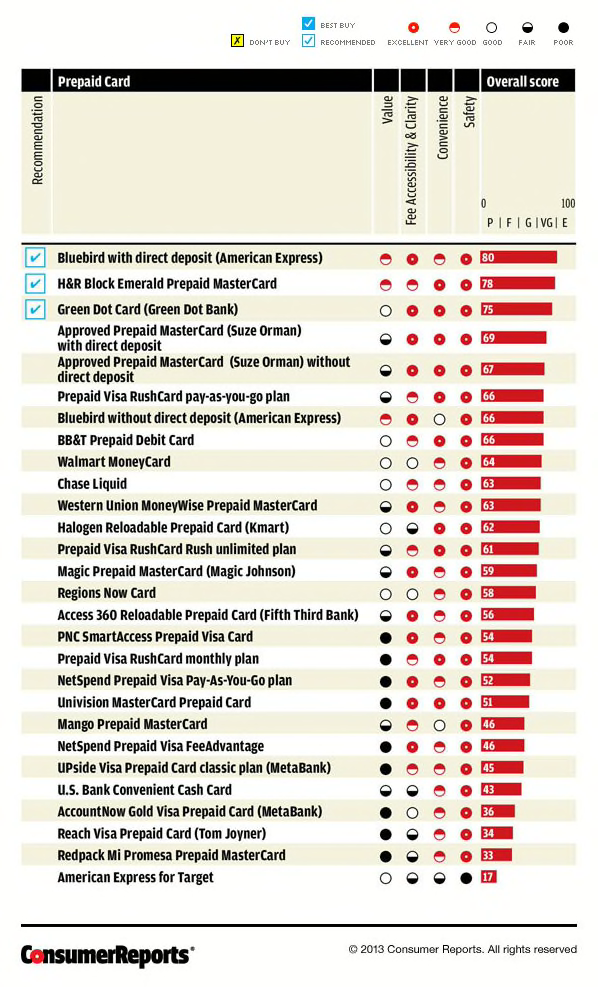

Consumers Union, the policy and advocacy arm of Consumer Reports, has tracked the prepaid-card market for years, and previous analyses found that checking accounts (which prepaid cards aim to replace) provided guaranteed protection, at a lower cost, than most cards. But this year's ratings of 26 cards found that some are now more competitive with checking accounts. Read the full report.

Prepaid cards are often given to teenagers and the college-bound because parents can reload them from afar and oversee spending. Big banks such as Chase and US Bank have recently joined the ranks of smaller companies to roll out their own cards. In 2012 about $77 billion was loaded onto prepaid cards in the U.S., according to the Mercator Advisory Group.

Prepaid cards often look like debit cards, with American Express, MasterCard, or Visa logos. They can be used to withdraw cash from an ATM, pay bills, or make purchases online and in stores. Unlike debit cards, they're not linked to traditional bank accounts. But some cards are still quite expensive, and not all of them offer the conveniences that consumers might expect.

One big knock against the cards are the fees: for activation, monthly maintenance, reloading, and ATM use. The Prepaid Visa Rush Card monthly card option, for example, has a one-time activation fee of $3.95 or $9.95, depending on the card design, and a monthly fee of $9.95. But it can get worse. For example, the NetSpend Prepaid Visa Pay-As-You-Go card carries a $1 or $2 "swipe" fee every time it's used to make a purchase. That can add up. The top cards in our survey do not charge purchase fees.

Issuers have added features for some cards that rival those of bank accounts, such as paper checks. Two-thirds of the cards in our survey allow the use of ATMs free or for a reduced fee. Text and e-mail alerts give account information. When considering a card, check to make sure your funds will be FDIC-insured.

For more news and articles about personal finance, subscribe to our feed.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop