Sign In

Until recently, home buyers occupied the sweet spot in the housing market. They were able to choose from a glut of available homes that were severely devalued during the recession, and they could lock in historically low mortgage interest rates.

But the landscape is shifting. Through May of this year, home prices rose almost as fast as they did during the peak bubble years that ended in 2006. The national median closing price for an existing single-family house was up 15.4 percent from May of 2012. And that was the largest year-over-year gain since the end of 2005, according to the National Association of Realtors. In addition, more people are buying: Monthly sales of existing homes, which include single-family homes, town houses, condominiums, and co-ops, were up 4.2 percent from April to May.

Home prices usually rise as the demand for them increases. But declining inventories are driving this housing recovery. Last spring there were 15 percent to 20 percent fewer homes available than in the spring of 2012, says Steve Cook, managing editor and co-publisher of RealEstateEconomyWatch.com, which tracks trends in the housing market. Because some homes were worth less than what people paid for them, many have been waiting to sell.

That's great news for those who are ready to list. It's not uncommon for sellers in many areas to receive multiple bids today, and in hot markets some homeowners are even lucky enough to experience bidding wars, says Walter Molony, economic issues media manager and spokesman for the National Association of Realtors. But it's tougher now for buyers to secure financing, which can cause deals to implode. In 2006 almost anyone could get a loan; now lenders are scrutinizing a buyer's ability to repay with more diligence.

Whether you're buying or selling, we have a variety of tips that will help you get the best deal. If you're not planning to move, you may still find it makes sense to refinance if you can lock in a lower interest rate.

If you've checked your home's value on these websites, you might have noticed very different results. These services aggregate data from several sources, including Multiple Listing Services. To come up with your home's value, they use the MLS estimate of what similar homes are selling for in your area, then apply other proprietary criteria. The amount varies because their data and formulas vary. For a rough estimate of your home's value, take the average of what Trulia and Zillow say, as well as similar sites like Homes.com and Realtor.com.

Home prices may be up, but in many markets they're still below where they were seven years ago. And mortgage interest rates are still low: The National Association of Realtors predicts that 30-year fixed rates will rise from their recent 4.29 percent national average to about 5 percent by the end of 2014. So the housing market will stay affordable for many people at least for the next year or so, says Steve Cook of RealEstateEconomyWatch.com. Here's how to close the deal on the home you want.

Scores have a big impact on the total amount you'll pay for a loan. If your score is 760 and you apply for a $300,000 30-year fixed mortgage, you could recently qualify for a 4.25 percent interest rate, with monthly payments of $1,476. But if your score was below 620, your interest rate would have been 5.84 percent and your monthly payment $1,768. Over the 30-year life of the loan, that would cost you more than $105,000.

Even if you have good credit, you might pay more than you should if there are errors on your credit reports. Five percent of consumers who checked their reports from the three major credit bureaus found errors that were serious enough to affect their credit scores, according to a recent study by the Federal Trade Commission. So examine your reports from all three—Experian, Equifax, and TransUnion—at Annualcreditreport.com. Report any errors, and check to make sure they are corrected.

Get pre-approved. That was always a good idea, but now it's a must, says Ron Phipps, a real-estate agent in Warwick, R.I. Sellers tend to take buyers who are pre-approved for a mortgage more seriously, a competitive edge over those who fail to take this step.

Do some digging to find out where you can get the best rates. Check several lenders, including national, local, and online banks as well as credit unions. We generally don't recommend that you hire a mortgage broker to do this for you because he may be more focused on selling you a mortgage than getting you the best deal.

Knowing your monthly payment amount isn't enough. Also get an estimate of the closing costs and all the additional fees you'll owe. Many of the fees involved are negotiable, such as the home inspector's fee, the cost to do a title search, and your attorney's fee, so get the best deal you can.

Use an agent. Working with your own real-estate agent can be helpful in a seller's market, when competition is high and homes sell quickly. An agent can clue you in to market conditions and will know which homes will cost you more than you might think because, for example, flood insurance might be required. You might also pay less for a home. A survey conducted a few years ago by the Consumer Reports National Research Center asked readers about their experiences buying and selling homes. It found that 66 percent who used a real-estate agent to buy paid an average of $5,000 less than the listing price. The buyers who negotiated their own deals without an agent (34 percent) paid close to the asking price.

Consider going right to contract. If the market in your area is especially hot, buyers should skip making an offer and write up a contract for a seller to review, says Robert Bailey, co-owner of Bailey Properties in Santa Cruz, Calif. Just make it contingent upon a home inspection. Also try to find out why the owner is selling, and add something to the deal that reflects his needs. If he wants more time to live in the house, for example, say you'll postpone the close. "I sold one house because a buyer agreed to take care of the family's pet until they were settled in their new home," Bailey says.

If you've wanted to put your house on the market, now may be the time to act. Here's how to get the most on your sale.

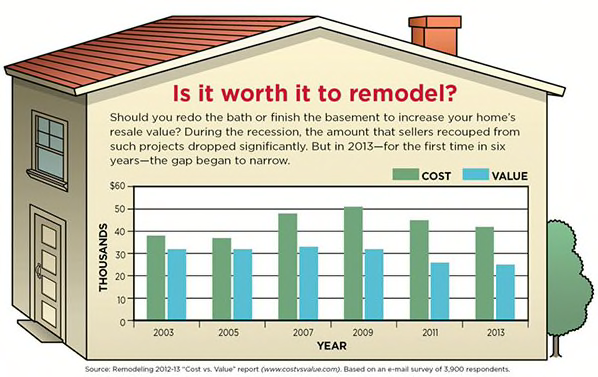

Pick the right improvements. "Curb appeal is crucial today," says Walter Molony of the National Association of Realtors. "Buyers get a lot of information from the Web, and they drive around to decide which ones they want to see." Remodeling magazine's annual "Cost vs. Value" report for 2013 found that sprucing up the outside of your home with new entry doors, fiber-cement siding, wood decks, and garage doors tended to recoup the most value when you sell.

You'll also want to clean, remove clutter, give overgrown trees and shrubbery a trim, and paint where needed. According to the Realtors association, the right color palette can raise your home's value by 10 percent or more. For interiors, warm beige colors appeal to the greatest number of people.

Interview more than one agent. Ask friends and family members for recommendations and meet with several candidates. They should explain how they would market your property—how they would advertise your home on social media, how they would handle open houses, and what they would say in Internet and newspaper listings. After you select an agent, make sure the marketing plan is part of the listing agreement, so if it's not followed you'll be able to take your business to another agent. Also try to negotiate the commission. Our survey found that many agents were willing to cut a deal. Readers who successfully negotiated a reduction often cut the traditional 6 percent to 3 or 4 percent, and they tended to be just as satisfied with the result as those who paid more.

Pay for an inspection. To spot expensive repairs, get a home inspection, which might run about $275 to $500 or so. Then you can make the repairs or, if you don't want to, you can share the information with potential buyers early in the process. "We've found buyers are most likely to accept flaws when they are most in love with your house, which is when they first want to buy it," says Robert Bailey of Bailey Properties in California. Buyers are less likely to gloss over shortcomings a few weeks later.

Assess your need for staging. You may want help to present your home in its best light. A two-hour consultation with a professional stager will cost about $300. A full staging, which includes renting furniture, can run from $500 to several thousand. You can search for a stager on the website of the International Association of Home Staging Professionals at iahsp.com/membersearch.php. What's more, you may be able to write off their fees (but probably not the paint or accessories they suggest you buy). Home staging is considered an "advertising fee" and can be subtracted from a gain on the sale of your home, along with agents' commissions and legal fees.

Price it right. Trying to make your house stand out by offering potential buyers enticements like a free set of golf clubs is so 2009. Today the listing price is critical, Bailey says. Homes sell most quickly if they are put on the market at a price that's right at, but not higher than, those of similar homes in the area. Have your agent do a market check of homes that have sold in the past few weeks.

Use round numbers. Most people buying homes today get information by searching online sites like Trulia.com. To conduct a search on that site, buyers specify a price range, beginning and ending with round numbers. So if you price your home that way, more people will see it. Instead of putting it on the market for $349,000, use $350,000 instead. That way people shopping online for houses from $300,000 to $350,000 will see your home, and so will people looking between $350,000 and $400,000.

Dodge low-appraisal nightmares. One of the downsides of today's sellers market is the tendency for appraisers to undervalue a property. That happens when prices have been rising quickly and appraisers who aren't familiar with the area use comparable transactions that don't reflect the latest price trends. So when a prospective buyer schedules the appraisal, make sure you are present to share data on comparable properties and home improvements you have made that may be overlooked.

You may have missed last year's record-low mortgage rates. But there's no need to panic.

You can still consider refinancing, says Walter Molony of the National Association of Realtors. Although you might get a 30-year fixed loan at about 4 percent now vs. last year's 3.24 percent, you can still lower your payments if your interest rate is currently 5 percent or more, he says.

HSH.com, which publishes mortgage and consumer loan data, has a refinancing calculator that can help you decide if a refi makes sense. You fill in the details about your current loan and the refi you're considering, and it estimates how much less your monthly payments will be, and how long it will take you to break even—in other words, recover your closing costs. A refi doesn't make sense if you plan to move before your break-even date. If you decide to proceed, check with your current lender to see if it charges a prepayment penalty. If it does, it will obviously increase the time it will take you to break even.

Whether you're a new or current homeowner, you should check your homeowners insurance coverage. Outdated assumptions about your coverage can cost you a bundle. Experts for Consumer Reports Money Adviser off these important points and tips for buying homeowner's insurance. Keep in mind:

While you search for the best coverage, keep in mind that rates can vary widely. You can compare rates at Insure.com, InsWeb, and NetQuote.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop