Sign In

If you've leaned heavily on fixed-income investments in retirement, you have probably had to economize during the downturn, or dig into your principal. But you may be able to gain a higher total return—and reduce the likelihood of losing money—without changing the percentage of your fixed-income holdings. To achieve that, you'll need to adjust the lineup of your investment mix—just a tad. And further, if you're willing to invest a bit more in stocks and less in bonds, you stand to gain more in returns. Done properly, you can do that without significantly increasing your risk.

Fixed-income investments, with their predictable returns, typically address the risk of interest-rate and income volatility. As long as you hold a bond, you should get the same income regardless of the bond's underlying value. But by misunderstanding other kinds of risk—such as inflation and taxes—you can put your retirement finances in greater peril.

A small uptick in inflation, for instance, can wipe out the effective yield on a bond or fund that looked attractive when you bought it. Bond interest income shrinks once it's taxed at ordinary income tax rates. What's more, as the Fed decides to raise rates, the principal value of your bonds will also decrease; in mutual funds it can create losses.

To reduce their tax risk, many people invest in tax-free municipal bonds, in spite of their lower returns. But retirees in lower tax brackets may be chasing a tax break that's not worth much. For example, if a taxable bond fund paid 4 percent and a tax-free bond fund paid 3 percent, the spread would be 25 percent. A client with a 15-percent top tax rate makes more by sticking with the taxable choice. At a 25-percent tax rate, the client can invest either way. At a 33 percent rate, he's better off with the tax-free investment.

Read about the fallacy of "risk-free" mutual funds. And check out our investing center for insights into investing for and in retirement.

Advisers say investing with sensitivity to the investment risks can help you gain better returns and sleep at night. It doesn't mean you'll avoid risk entirely. But you can be smart about where you'll take it.

Long-term bonds are an example of purchases that are currently not worth the risk. As rates rise, the bonds' value drops. The lost value can have a real and psychological impact even if you plan to hold the bonds to maturity. Robert Fragasso, a financial adviser based in Pittsburgh, says he recommends only CDs and U.S. Treasury bonds of no more than three years' maturity. Because investors can be charged more to buy an individual bond, they should own bonds through mutual funds only, purchased through an institution or brokerage, he says.

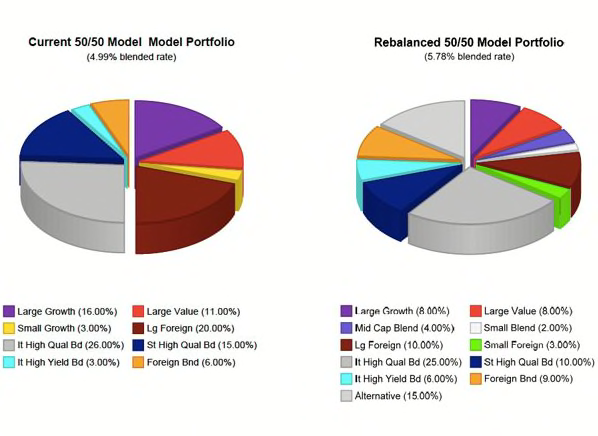

By rearranging and adding to your portfolio—and not changing the ratio of bonds to stocks—you may actually raise your return and reduce your risk. Fragasso illustrates that with the case of a client with 50 percent in equity funds (large growth, large value, small growth, and large foreign) and 50 percent in bond holdings (intermediate high quality, short-term high quality, intermediate high yield, and foreign). By keeping the 50-50 mix and adding three new funds with more potential for growth—mid-cap blends, small-cap blends, and alternative investments such as real estate—he increased the portfolio's expected return to 5.78 percent from 4.99 percent. Due to greater diversification, the projected risk of the portfolio dropped.

In the model portfolio above, for example, Fragasso shows how he was able to increase expected returns by changing allocations in some types of funds, removing others (a small growth fund) and diversifying—adding small blend and small foreign equity funds, as well as alternative funds that might include real estate holdings, convertible bonds and commodities. (See Fragasso's disclaimer for this graph and one the below.)

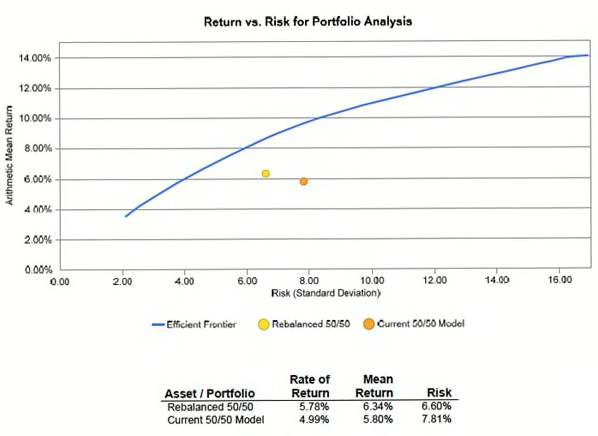

Notably, the change could mean slightly less risk for the investor. When Fragasso crunched the numbers to create the graph below, the new portfolio's standard deviation—a proxy for risk— appears slightly lower. (Check Investopedia's explanation of the "efficient frontier" line.)

Often, though, diversification means accepting more stock into a portfolio. A 50-50 mix might have been right years ago for a new retiree; it now may be far too conservative, says Angie Stephenson, a partner with ParenteBeard Wealth Management in Lancaster, Pa.

Retirees who might have held just 25 percent in the stock market in the past are now adjusting their holdings to 35 percent. The new mix includes more alternative funds, such as real estate investment trusts and convertible bonds. Stephenson says that although adding stock increases the risk of losing principal, it provides the opportunity for greater growth, decreasing the risk that inflation and rising interest rates will erode savings.

—Tobie Stanger

This article also appeared in the July 2014 issue of Consumer Reports Money Adviser.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop