Sign In

You can now get financial help to lower the cost of your monthly health insurance. These FAQs will explain what you need to know when applying for financial help for health insurance. They will help you understand how to report your income.

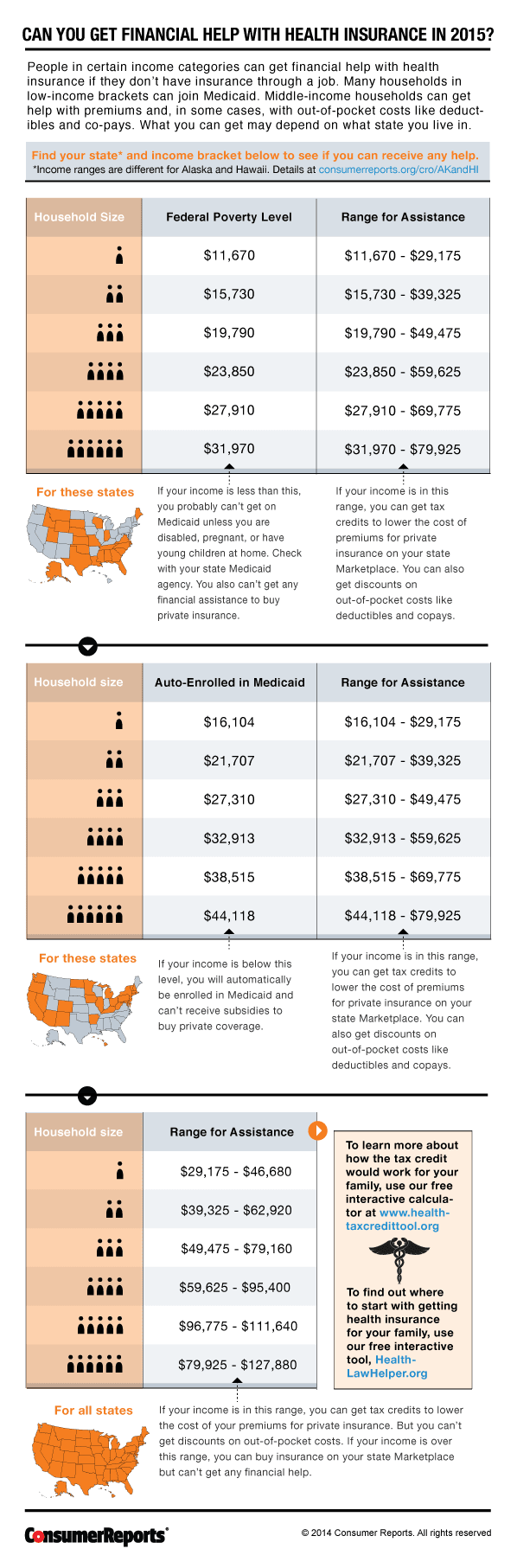

The health care law (known as the Affordable Care Act, ACA, or "Obamacare") offers special financial assistance to help people pay for insurance. To get the help, you have to buy insurance on your state's Health Insurance Marketplace. For 2015, tax credits are available to single people who make up to $46,680 a year. A family of four can make up to $95,400 a year and get tax credits.

You can use these tax credits several ways to reduce the cost of your health insurance. For people whose income is lower, you can also get cost-sharing reductions (lower co-payments, co-insurance or deductibles). A single person can make up to $29,175 a year and get lower cost-sharing and tax credits. A family of four can make up to $59,625 a year and get cost-sharing reductions in addition to tax credits.

To figure out if you qualify for financial assistance for 2015, your Health Insurance Marketplace needs to know your household income. The Marketplace needs to know how much you expect your tax household's income will be for the year you will have the insurance. (For Medicaid, they will look at your current monthly income.) That's an easy question to answer if you have a steady income from a job or other regular, predictable income. But it is not so easy if you have unsteady or hard-to-predict income from self-employment, sales commissions, seasonal work, or another form of income.

The Health Premium Tax Credit is a new way to lower the cost of health insurance when you buy it through the Marketplace. Because it is a tax credit, it lowers the total amount of tax you owe the IRS. Or, if you don't owe any tax, it increases your refund. You can use the tax credit even if you did not make enough to file taxes last year.

There are two ways to use the tax credit. You can get it "in advance" and use it to lower your monthly health premiums right away. Or, you can wait until tax time and get the full amount as a refund when you file your taxes. Keep in mind, if you use it "in advance" you should call your Health Insurance Marketplace to report any changes in income or family size during the year. Take a look at our tax credit tool to help you understand better how the tax credits work.

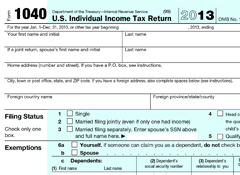

The ACA counts income based on something called your "Modified Adjusted Gross Income" (MAGI). MAGI is your taxable income, the income you report on your tax return. For most people, MAGI will be the adjusted gross income (AGI) that is on your federal tax return. You can find your adjusted gross income in the following places:

All Social Security benefits count towards MAGI, not just the taxable amount. Here's an annotated version of Form 1040 that we marked up to show what goes into MAGI.

If you don't have a previous tax return to use or you think you may be eligible for Medicaid, this worksheet can help you learn more about MAGI.

Just like when you complete your income taxes, for the tax credits you report everyone in your tax household's income. That means you report your income, your spouse's income and the income of any dependents who are on your tax return.

The income that you report should be for the year that you want health insurance. If you apply in November 2014 for insurance to start in January 2015, you will need to estimate your future income for 2015.

If you are applying during the same year you will have insurance (for example, applying in February 2015 for insurance that would start in March 2015), you would report your expected income for 2015.

If your income is from a regular paycheck, it will be easy to estimate your income even if the year hasn't ended. But if your income is unpredictable, you may not know your exact income because it has not come in yet. You might have to guess. Think about what jobs you expect to work this year and how much you think each job might pay.

If you filed a federal tax return last year, you can use it as a starting point. Look for the Adjusted Gross Income you reported. Then add or subtract, depending on how you think your income might change. Which jobs will be different this year? Which jobs will be the same? Don't forget to deduct self-employment expenses.

It is important to be as accurate as you can when estimating your income. If you get advance tax credits and guess your income too low on your application, you may get too much tax credit. If you do, then you might have to pay all or part of the advance tax credits back when you file your taxes. The amount you owe will depend on what your final income turns out to be.

But, if you guessed your income too high on your application, the advance tax credit may be less than what you should get. If that's the case, you will get the rest of the tax credit when you file your taxes. You may even get a tax refund.

One way to avoid owing all or a part of your tax credit later is to only ask for part of it in advance. You can still lower your monthly premiums that way. And you will get the rest of your tax credit when you file your taxes. You can also take none of the credit in advance. Then you would get the whole tax credit when you file your taxes. We have an interactive online tool that explains more about how the tax credits work.

The Marketplace will check the income you reported on your application and compare it to what the IRS has on file for you. This is called "income verification." The Marketplace does this by electronically asking the Internal Revenue Service (IRS) database and other databases if what you reported is the same as what they have on file. The IRS will not share your personal tax data with your Marketplace. They will just tell the Marketplace if the income you reported does or does not match what they have on file for you.

The IRS information comes from your latest income tax return. When you apply for coverage in 2015, that's probably going to be your 2013 tax return. If your income has changed since then, your reported income may not match the data on file.

If the Marketplace can't verify your income, you might have to give them documents to show them what you say is likely true. Many kinds of proof are acceptable.

| If you have… | Acceptable forms of proof might include… |

| Wages (income an employer pays you) |

|

| Self-employment income |

|

| Social Security |

|

| Other income |

|

If you cannot get any of the listed documents, do your best to give the Marketplace something that shows that you expect to make the amount of money you put on your application. Your marketplace will give you instructions on how to send in your documents. Follow them carefully so your paperwork doesn't get lost.

This fact sheet was produced by Julie Silas, Senior Attorney, Consumers Union at jsilas@consumer.org. It is also available as a downloadable .pdf in English and Spanish.

Visit our health insurance center to find out how to select, obtain, and use all kinds of health insurance, including private insurance, employer insurance, Medicare, and Medicaid.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop