Before Lisa Beach, an assistant vice president for an Austin, Texas, credit union, had surgery for severe back pain two years ago, she did everything she could think of to make sure she wouldn't have to pay a lot out of pocket.

"I wanted to know the names of anyone who would have any kind of involvement in my surgery," she says. Then she ran the names by her insurance company, Aetna, to make sure the care would be covered.

In spite of her diligence, she received a $1,050 bill for services provided by an out-of-network doctor who, it turns out, wasn't even in the hospital during her surgery. That doctor had simply provided specialized equipment used during the operation.

Aetna refused Beach's appeal, she says, so she went straight to the equipment provider. They agreed to drop the bill to $700—but only if she paid that day. She handed over the last $522 in her flexible spending account but still gets bills for the remaining $178.

"I thought I did everything right, only to find out some information wasn't disclosed to me," Beach says.

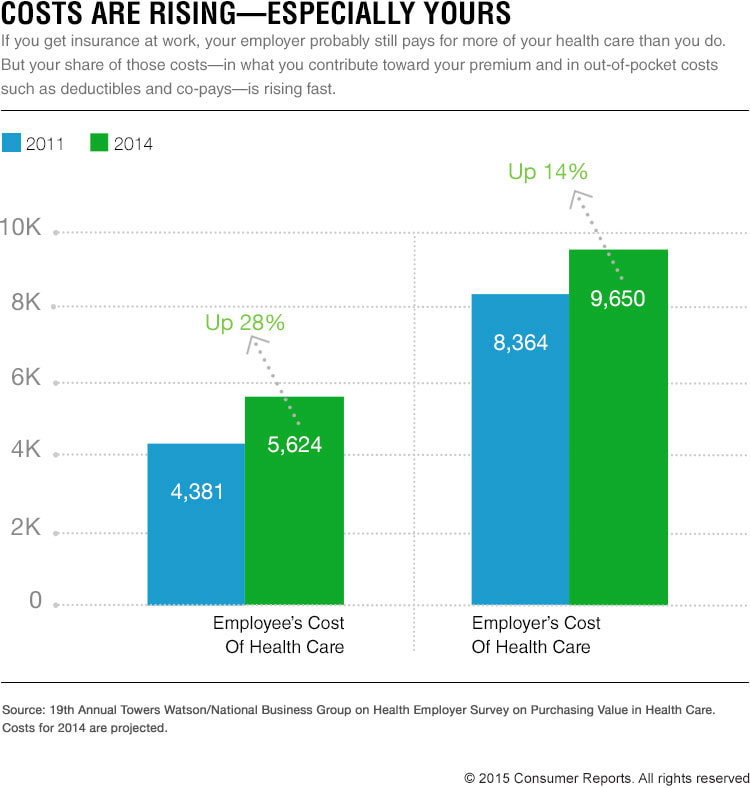

Beach's experience is all too common. A 2015 Consumer Reports survey of 2,200 Americans found that most with private insurance don't know where to turn with complaints about their health insurance, and almost a third had received a medical bill for which they had to foot more of the cost than they had expected. Many of those people ended up paying the bill in full.

"These problems are happening much more frequently," says Blake Hutson, who heads Consumer Reports' health insurance advocacy efforts. "We're expected to pay a larger and larger share of our health care costs, and getting hit with harsh penalties if, even unknowingly, we see providers outside of our network," Hutson says.

That's true not just for people who buy insurance on their own through state or federal marketplaces but for those covered through their jobs. Even people on Medicare face shocks if they don't understand the details of their plans—something that happens easily.

How can you troubleshoot the increasingly tricky health insurance system? We've pinpointed seven situations that can cause medical bill sticker shock—and have advice on how to handle each.

1. Your Insurance Company Pays the Surgeon for Your Knee Replacement—But You're on the Hook for the Anesthesiologist's Bill

Problem: You ended up seeing an "out-of-network" provider. Your insurance company has a list of doctors you're supposed to get all of your care from, and the anesthesiologist wasn't one of them. Though that scenario often happens with anesthesiologists, the provider could also be an assistant surgeon or someone you never even met in person, such as the radiologist who reads an MRI or a pathologist who analyzes the results of a biopsy.

How to prevent this shocker: If you're preparing for a nonemergency procedure—such as a joint replacement or having a baby—ask the person who handles your surgeon's billing for a complete list of the anesthesiologists, assistant surgeons, and everyone else who could conceivably be part of your medical team. Call your insurance company to determine whether all of those people are in your plan's network. Make sure you tell them the exact name of the plan that's on your insurance card, because insurers often have multiple plans, each with a different network of providers. If anyone on your list is not, ask the surgeon whether he or she can use network providers instead. If that's not possible, contact the non-network providers to determine how much you will have to cover so that you're not in for a surprise later. Or consider finding another surgeon who will use only in-network providers.

If it happens to you anyway: Tell the providers and your insurer that you didn't realize the procedure would involve doctors outside of your network. Some physicians may accept the insurance payment and forgive the balance, or the insurer and non-network doctor may negotiate a fee, leaving you with a smaller balance. If you have a plan that you bought on your own through a state or federal marketplace, contact your state health insurance department. Some states have rules for such plans, limiting how much you have to pay for out-of-network care.

Video: What If Your Pizza Place Billed Like a Hospital?

2. The Rheumatologist That You Saw Billed $1,500 for Your Visit, But Insurance Covered Only $1,000—and You Have to Pay the Balance

Problem: You're a victim of "balance billing," another way that going out-of-network can cost you. In that situation, your insurer allows you to use out-of-network providers but pays only the discounted rate that they've negotiated with in-network providers, leaving you with the balance. And that cost can be substantial, because the fees insurers set with in-network providers can be hundreds or even thousands of dollars less than what doctors charge directly.

How to prevent this shocker: See providers in your plan's network whenever possible. Call doctors and your insurance company—before your visit or procedure—to make sure that they are still in the network. (The insurer's online directory could be out of date.) If you decide to go out of network, call your insurer to confirm what your share will be. Most plans, by the way, have exceptions for problems that can't be handled by an in-network provider. Talk with your insurer if you think that applies to your situation.

If it happens to you anyway: If you saw a doctor in your plan's network, don't pay the bill. Instead, tell the provider and your insurer that they've made a mistake. If the doctor was out of your network, explain your situation to the doctor. You might be able to get him or her to forgive the bill, negotiate a lower fee, or offer a payment plan that makes the bill more manageable.

3. You Broke Your Leg, and Your ER Visit Left You With a Hefty Bill

Problem: This particularly nasty version of balance billing happens if the hospital you went to or the doctors who saw you in the ER are out of network. After all, in an emergency you may not have time to find an in-network provider. The Affordable Care Act has partially, but not fully, addressed the problem: It now requires insurance to cover ER care—but only at the rate paid to in-network providers. So if your ER doc is out of network, which they often are, you may be responsible for the difference.

How to prevent this shocker: If you live close to several hospitals, call your insurer now—before you actually need an ER—to find out which are in your network and employ network ER physicians. Then, in an emergency, try to go to one of those (in your own car, if it's safe; ambulances often aren't covered). Reserve ERs for true emergencies. If your regular doctor could handle the problem, go there instead. Urgent care centers can also be options, but check with your insurer to make sure you'll be covered.

If it happens to you anyway: Contact the insurer and the doctor and explain that you didn't have a choice because you needed emergency care. In some cases, the non-network doctor will accept the insurance payment, or the insurer and the doctor will negotiate an acceptable fee. In addition, call your state's insurance department to see whether it has passed a law that prevents balance billing in the ER. If it has, don't pay the bill, and lodge a complaint with the insurer. (See how to file a complainte in your state.)

4. You Saw an In-Network Provider—But Your Insurer Says You're Responsible for the Whole Bill

Problem: Your health plan probably has a high deductible that you haven't yet met. High-deductible plans can seem attractive because they often have low monthly premiums. And more Americans now have that kind of coverage because insurers and employers are trying to shift a greater portion of health care costs to consumers. But many people who sign up for high-deductible plans don't realize exactly how much they have to pay before insurance kicks in. The law currently caps total out-of-pocket spending at $6,850 for individuals and $13,700 for families.

How to prevent this shocker: The next time you sign up for insurance, whether through work or on your own from a federal or state marketplace, think hard about whether you really want a high-deductible plan. (For the factors to consider and more advice on how to pick the right health plan for you and your family, see "Shop Smart for the Right Health Insurance Plan This Year."

If it happens to you anyway: Call the insurer and ask whether you have reached your deductible, or check your insurer's website for a tool that helps you track your expenses. If you've met the deductible, let the doctor and insurance company know. If not, check to make sure you're being billed at the lower negotiated rate, not the out-of-network rate.

5. You Thought Medicare Would Cover Your Doctor Visit, But No Such Luck

Problem: You may have Medicare Advantage, not traditional Medicare. With traditional Medicare, you can usually visit any doctor and hospital you like as long as they accept Medicare—something almost all health care providers do. But when first enrolling in Medicare, you may have signed up for a Medicare Advantage plan thinking it was the same as traditional Medicare, perhaps in response to a pitch you received in the mail or on the phone. Medicare Advantage plans—which are run by private insurance companies such as Aetna or Cigna, not by the federal government—offer some advantages. But they do require people to use a specified network of providers. So if you signed up for Medicare Advantage and then see a provider outside of your network, you could be stuck with the bill.

How to prevent this shocker: If you're not sure whether you have Medicare Advantage or traditional Medicare, check your insurance card. It probably won't say "Medicare Advantage" but might list a plan name, such as "Secure Horizons." If you're still not sure, call 800-633-4227 and ask which one you have. If you have Medicare Advantage, stick with network providers if possible. If you're not satisfied with your Medicare Advantage plan, you can switch plans or enroll in traditional Medicare during the annual enrollment period. For 2016 coverage, that period runs from Nov. 1, 2015, to Jan. 31, 2016. Read more about Medicare Advangate vs. Traditional Medicare.

If it happens to you anyway: Find out whether your plan allows exceptions for visits to non-network providers and whether you qualify for the exception in this case. Contact the non-network provider and ask whether it is willing to accept the insurance payment and forgive the balance. Many are willing to do that, at least once.

6. You Saw Your Doctor for a Basic, 5-Minute Visit But Were Billed for an Expensive Procedure

Problem: You may be the victim of a fraudulent practice known as "upcoding." Every service performed by a health care provider has a code attached to it that's used for billing private or public insurers (Medicare and Medicaid). Upcoding occurs when the provider submits a billing code for a higher-paying service than what actually took place. For example, if your child has an earache, your doctor can often ease the pain by simply removing built-up earwax. But some doctors have been known to bill the procedure as "outpatient surgery," allowing them to get paid at a higher rate.

How to prevent this shocker: It's hard to prevent, unless you ask your doctor how he or she will be coding your visit or procedure—which is neither practical nor, usually, necessary. But if you have a history of that kind of problem with your health care provider, consider asking to put the office staff on notice that you're watching.

If it happens to you anyway: Check the Explanation of Benefits (EOB) form that you should get from your insurer after every doctor visit. If the charges on it seem unreasonably high, ask the doctor's billing department to explain why a certain code was used. It could be an honest mistake, or there may be a valid reason for the code. For example, the doctor removed a mole during an office visit—a procedure you consider simple but may have been more complicated than you thought—and a provider can legitimately bill for it at a higher rate. If you're not satisfied with the doctor's explanation and suspect fraud, contact your insurance company, Medicare, or Medicaid, or your state insurance department. And check past bills for a pattern of upcoding. Illegal upcoding costs consumers millions of dollars in increased premiums and misspent tax dollars for Medicare and Medicaid payments.

7. The Medication You Take Every Day Has Suddenly Shot Up in Price

Problem: Your plan could have updated its "formulary"—the list of drugs that your insurer routinely covers—and your medication is no longer on it. Most private health plans can adjust their formularies at any time; Medicare can do that only during the open enrollment period. Plans update their lists for many reasons: They negotiated a better deal with the drug company, new research shows the medication isn't as safe or effective as thought, or a generic (and cheaper) version of the drug hit the market that is just as safe and effective.

How to prevent this shocker: Before choosing a health plan, check its formulary to see which drugs are covered. That's essential if you have a chronic condition, such as diabetes or rheumatoid arthritis, that requires you to regularly take medications. You'll get the lowest out-of-pocket costs when you buy the coverage plan's "preferred" generic drugs, usually called "Tier 1." A drug that isn't listed on the formulary will often have the highest out-of-pocket cost and, in some cases, may not be covered at all. If you're dissatisfied with your plan's formulary, look for a better one at health insurance sign-up time. In addition, when your doctor writes a prescription, ask how much it costs and whether it's covered by your insurance. And always ask whether a low-cost generic is available.

If it happens to you anyway: If you find that the drug's price is much higher than you expected when you pick up your prescription, ask your doctor or pharmacist whether a similar drug covered by your plan will work. It may be as simple as switching to a generic. If no other drug is appropriate, ask for an exception from your insurer. You should also shop around. Consumer Reports' secret shoppers have found that doing so can save you hundreds of dollars. Costco, in particular, often has low drug prices, even for nonmembers. Last, try negotiating with the pharmacist. Our shoppers found that they could get discounts by asking, "Is this the lowest possible price you can offer?" (Read more about how to handle sudden spikes in your prescription drug costs.)

How You Can Help End Surprise Medical Bills

Consumer Reports is working to protect consumers from surprise medical bills in several ways:

• In New York, we helped pass a landmark law to prevent balance billing in hospital emergency rooms, and we're working on similar laws in states throughout the nation. You can join our efforts to stop surprise medical bills, share your billing story, and find out what's going on in your state by going to EndSurpriseMedicalBills.org.

• In California, we worked with the California Department of Insurance and the University of California, San Francisco on a tool that helps consumers there see what they might pay for health care and compare providers on quality. Try the California Healthcare Compare tool.

Editor's Note: This article also appeared in the November 2015 issue of Consumer Reports magazine.