Sign In

Mortgage foreclosures and credit-card debt have drawn the spotlight since the financial collapse of 2008. But there's another type of debt that could have potentially crippling ramifications for the U.S. economy: student debt.

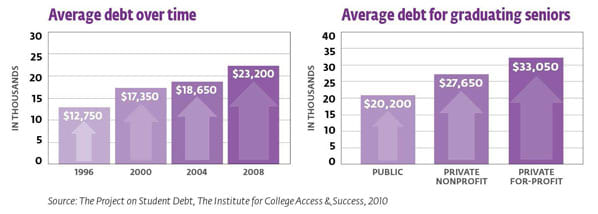

How bad is it? The amount of student debt owed by Americans exceeded outstanding credit-card debt for the first time in 2010. Two-thirds of college graduates carried some debt at commencement, and the Class of 2010 had an average of $25,250 in student debt, up 5 percent from the previous year, according to The Institute for College Access & Success (TICAS), a nonprofit policy research group in Oakland, Calif. All in all, it's estimated that Americans owe more than $900 billion in federal and private loans.

At the same time, the depressed job market makes repaying those loans harder than it has been in decades. Two-year default rates on all student loans hit 8.8 percent for those starting repayment in 2009, with 15 percent defaulting at for-profit institutions, according to the Department of Education. Unlike most consumer loans, student debt generally can't be discharged by declaring bankruptcy. Lenders can recover the funds by garnisheeing wages, tax refunds, even part of Social Security checks.

All of this has consequences not just for graduates but also for the larger society. Some economists fear that lingering student debt will force many young adults to delay or defer important milestones, such as marriage and starting a family, which can impede a full economic recovery. Young workers with wrecked credit from unaffordable student loans, for example, won't be able to get mortgages to purchase homes, which could make it even tougher for retirees and others to sell theirs.

Jeff Macaluso, 42, a website designer from Dobbs Ferry, N.Y., says his student debt, about $59,000, is "like a prison sentence." His monthly payment is $430 under an income-contingent repayment option for a federal consolidation loan he took out about a decade ago, although he tries to pay $630 a month to keep the interest down.

Macaluso, who earned a master's degree in fine arts in 1997, says he's happy with the career opportunities his education afforded him. But paying off the debt is preventing him from saving for retirement and might deter him and his wife from buying a home. The debt, with more than 6 percent interest, "just grew and grew and grew," he says, "and I'm saddled with it unless I make twice as much as I'm making."

Student indebtedness has been rising sharply since the early 1990s. Skyrocketing college tuition and fees, which have risen faster than inflation, are factors. And government grants and scholarship aid haven't kept pace with costs, resulting in a greater reliance by students and parents on borrowing to fill the gap. And in recent years, as home values have declined, more families that may have relied on home equity for financing are looking to student and parent educational loans from government and private lenders.

TICAS estimates that at least 22 percent of student debt from nonprofit four-year colleges for the Class of 2010 was composed of private loans outside the federal student loan program. Those private loans often come with high variable interest rates, additional loan fees, and strict repayment requirements, even if borrowers are unemployed or can't afford the payments.

Spiraling student debt is also linked to the growing number of for-profit colleges, whose students have a much higher rate of borrowing than those at public and private nonprofit institutions and are more likely to be steered to private lenders. In 2011 the National Consumer Law Center addressed why students at for-profit colleges defaulted on their debt at a higher rate than those at other types of educational institutions. The NCLC attributed this to poor academic completion and job placement rates at many for-profit schools.

Whatever type of college students attend, they don't always understand what they're getting into when they take out loans. Kristine Beckford, 22, a senior majoring in communications at Lehman College in the Bronx, N.Y., part of the public City University of New York, says she already owes $60,000 to $70,000 in student loans for two other colleges she attended before transferring to Lehman. She's not certain whether they are federal or private loans ("What's the difference?" she asked). The first in her family to attend college, Beckford says she received virtually no financial-aid counseling.

For the more than 36 million people saddled with federal student debt, what's the best strategy for digging out of the hole? "There are ways to manage it in tough times if you don't stick your head in the sand," says Lauren Asher, president of The Institute for College Access & Success.

Complicating matters is the fact that the various types of student loans have different repayment options. Most federally backed student loans must be repaid starting six months after the borrower leaves school or drops below half-time status. Some private loans and unsubsidized federal loans require interest payments even while the student is still enrolled.

The average college student has eight to 12 loans for his undergraduate education, says Mark Kantrowitz, publisher of FinAid.org, a financial-aid website, and Fastweb.com, a scholarship-information site. Borrowers can begin to get a handle on their debt by following these steps:

1. Find out how much you owe and to what lenders

Upon graduation or sooner, line up all your student loans and determine the loan servicers, balances, interest rates, repayment options, and grace periods. You might have a combination of private loans and those that are backed by the federal government. If you don't know the types of loans you have, call or write to the student-aid office at your college or your lenders, or go to the National Student Loan Data System, a database of federal loans (private ones aren't included).

2. Choose a repayment option

Federal loans, which include Perkins and Stafford loans and Direct PLUS loans (usually taken out by parents), offer several repayment options. The standard term is 10 years, and the minimum monthly payment is $50. Stretching out your payments over a longer period reduces the monthly amount but results in higher total interest expenses over the life of the loan.

Take a hard look at your financial situation and your income potential for the next few years. You'll save money and get out of debt faster by paying off your highest-interest loans as quickly as possible, which you can do by making the largest payments you can afford each month and applying extra to the principal.

If your total debt exceeds your first-year income after graduation, you probably won't be able to afford payments under the standard 10-year repayment plan. In that case, you may want to consider these repayment options, which result in smaller, more affordable monthly payments:

3. Explore options if you can't afford payments

For federal loans, you can request a deferment or forbearance. Under a deferment you may be permitted to stop making payments temporarily if you meet certain requirements. Under forbearance you may be allowed to stop making payments temporarily, make smaller payments, or extend the time for making payments if you don't qualify for a deferment. Forbearance is for a maximum of three years at the discretion of the lender, and you must reapply each year. "This is a last resort before default or for short-term financial problems," Kantrowitz says.

Most private loans don't offer deferment, and forbearance terms are limited. Quarterly fees may also apply, and interest accrues during the forbearance.

Don't reduce or skip payments without permission or you might be reported delinquent or in default. National credit bureaus could be notified of your default, which would adversely affect your credit score and also prevent you from qualifying for additional federal student aid.

4. Consider jobs or volunteer programs that qualify for deferment or forgiveness

Certain public-service and nonprofit-sector careers, such as teaching, police and fire services, working in public-interest law or public health, or joining the military, may qualify you for cancellation of federal loans. Generally, if you make 120 on-time payments, you might be eligible to have the outstanding loan balance (principal and interest) forgiven, and you could be exempt from taxation on the discharged amount.

You can find more information on the Department of Education's Public Service Loan Forgiveness page. Not all federal loans are eligible.

5. Consider loan consolidation

You can combine loans into one payment, which is more of a convenience than a cost savings, unless you still have unconsolidated loans that originated before 2006. Students and parents can't combine their loans; only loans taken out by the same borrower can be consolidated. And private student loans usually can't be consolidated with federal student loans.

6. Think twice about going back to school to avoid unemployment

College enrollment increases during recessions as young adults seek additional degrees and others seek retraining. But incurring more student debt might not pay off. See How to avoid borrowing for advice on ways to avoid borrowing.

Erin Button, 23, of Chicago, an administrative assistant at the Public Interest Research Group, is rethinking plans to go to law school after graduating from Cornell University last year with $78,000 in private and federal loans for her bachelor's degree in anthropology. She gets a repayment benefit of $200 a month from her nonprofit job and pays $450 a month in debt service, more than she pays in rent. Button, who earns less than $25,000 a year, carries five loans with interest rates ranging from 3.8 percent to 6.8 percent and terms of 10 to 30 years. "It's daunting," she says, "but I'm taking it one month at a time."

7. Contact your lender immediately if you can't pay

Skipping out on a student loan won't solve the problem. Defaulting will add late fees and collection costs to your outstanding balance. Parents or grandparents who want to help recent graduates should consider helping to pay back loans instead of giving cash.

• Opt for a community college for two years and then transfer to a four-year institution, or attend an in-state public university.

• Fill out the Free Application for Federal Student Aid, or FAFSA, as soon as possible after Jan. 1 for each coming academic year to determine your eligibility for need-based assistance, which doesn't need to be repaid. Take advantage of all grant, scholarship, and work-study opportunities.

• Choose thriftier meal plans and housing if you can. Don't take out loans to cover such nonessentials as entertainment and room furnishings. Consider working part-time to cover incidentals.

• If you must borrow, avoid using private loans except as a last resort, even though their interest rates may be lower than federal loans now. That's because federal loans issued after July 2006 have a fixed rate of 6.8 percent, while most private loans have variable rates often tied to the London Interbank Offered Rate (LIBOR). Home-equity loans, which may be cheaper now, are also riskier because they can cost you your home if you default.

Mark Kantrowitz, publisher of FinAid.org, suggests that students not borrow more than they can earn in their first full year of employment. A higher debt-to-earnings ratio would probably need to be paid off over 20 years rather than 10 years.

A version of this article appeared in the May 2012 issue of Consumer Reports magazine with the headline "Student Debt: Your Threat."

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop