Sign In

If you thought depositing checks into your bank account would never be anything other than a mundane but mandatory chore, perhaps you haven't heard of the bank-check selfie, more formally known among bankers as "remote deposit capture".

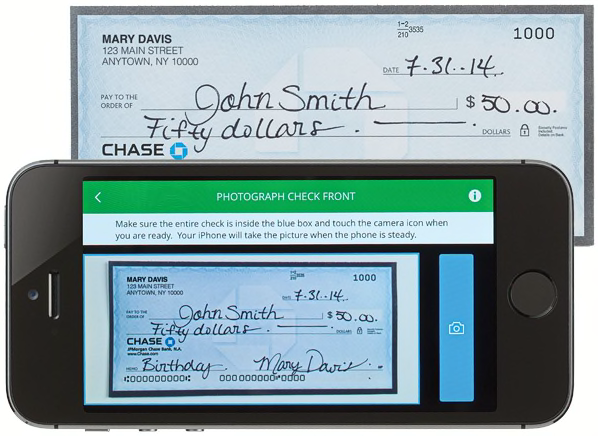

Use your mobile banking app and smart-phone camera to snap a picture of the front and back of a paper check, then electronically and securely deposit it into your account. You save time and hassles by not traveling to a bank branch and not waiting in a teller line.

More than 75 million U.S. consumers use their smart phones for mobile banking. But only 38 percent have tried depositing by cell phone in the past year, according to the most recent Federal Reserve survey. Not all banks offer the service, introduced by USAA Federal Savings Bank in 2009, but laggards are now scrambling to provide it. Frank Aloi, president of Ath Power Consulting, a financial-services-industry research firm based in Boston, says it's the feature most desired by mobile-banking-app customers.

But before you point and shoot, beware of some potential pitfalls, especially where personal checks are concerned.

Federal regulations dictate how long banks can hold checks before making the funds available—and it isn't very long. In general, the first $200 of a deposit must be available for cash withdrawal or check writing the next business day. The rest should be available on the second day for check-writing purposes and on the third for cash withdrawal, subject to certain exceptions and other details.

But the regulations were written before the advent of mobile banking and don't include it, creating a loophole big enough for certain banks to drive an armored car through.

For example, GoBank, a virtual bank whose customers access their accounts almost entirely via personal computer and smart phone, holds funds from personal checks hostage for up to 10 days. GoBank has no branches, and its nationwide network of 42,000 fee-free ATMs doesn't accept deposits, so remote deposit is the only way to get checks into a GoBank account.

Your account agreement generally governs this outside-the-regulations issue, and banks' voluntary rules aren't always anti-consumer. Many, including Chase, Citi, PNC, TD Bank, and U.S. Bank, as well as the virtual banks Ally and Simple, make funds available according to the standard regulations or better. TD Bank, for example, generally releases funds the first business day after deposit.

Certain banks place longer holds. BB&T generally makes remote deposit funds available within three business days. American Express Bluebird, a virtual checking account, holds funds until the sixth business day after deposit. Because that unavoidably stretches over a weekend's two nonbusiness days, the AmEx delay amounts to more than a one-calendar-week hold.

The more you use your smart phone for personal financial business, the more you need to keep your phone safe.

After you make your smart-phone deposit, hang onto the paper check for two weeks in case a problem arises. Date and mark it as a mobile deposit so that you or your significant other doesn't mistakenly deposit it again and incur returned-deposit fees. Shred or otherwise completely destroy the paper check (don't recycle it) so that a crook can't use it.

Remote-deposit fees appear to be uncommon, but at least one big institution, U.S. Bank, charges 50 cents per check. That's outrageous because digital deposits can be cheaper for banks to process than paper ones.

Ask your bank when funds from a remote check deposit will be available. If the smart-phone deposit hold is longer than usual and you need the funds now, deposit the check using a teller or an ATM; if you use a virtual bank and prefer that type, consider switching to Ally or Simple.

Use direct deposit. Have your paycheck, Social Security benefits, and other income electronically direct-deposited to your account instead of receiving paper checks that must then be deposited. Direct-deposit funds must be available to you the next business day after the bank receives them, and many institutions release them the day they're received.

Avoid delays. Cutoff times for deposit, say 5 p.m., bump your "day of deposit" to the next business day, which means the funds-availability clock doesn't start till then. So don't put off deposits until late in the day. And, of course, weekends and holidays don't count as business days.

This article also appeared in the September 2014 issue of Consumer Reports magazine.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop