How to Lower Your Medical Bills

As the cost of care rises, even insured people can be on the hook for huge healthcare expenses. But there are ways to save—before you seek treatment and after.

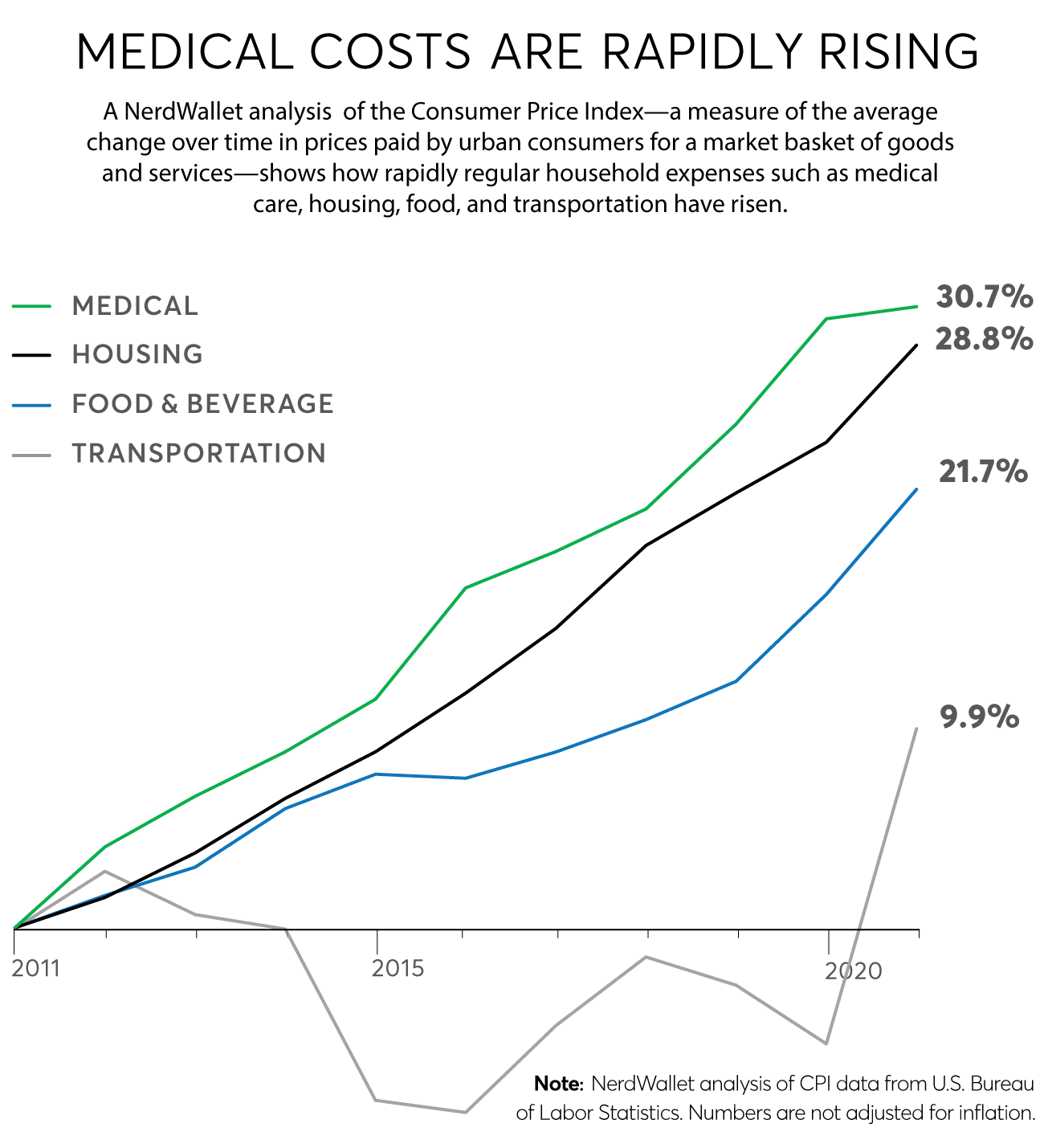

While more people in the U.S. have health insurance than ever—more than 90 percent—medical debt is a problem that has not gone away.

In fact, the reverse is true. Americans have more medical debt in collections—at least $140 billion—than all other types combined, according to a 2021 analysis in the Journal of the American Medical Association. That’s up from the $81 million a different study found in 2016. And almost 1 in 5 households has medical debt, owing a median of $2,000, according to 2019 U.S. Census Bureau data.

For people with health insurance, high deductibles and copays are a main cause. Another: “The cost of healthcare has risen dramatically in the last 10 years,” says Chuck Bell, senior policy analyst at Consumer Reports. “Every year, people have to reach deeper into their pockets to afford care, leaving many with big unpaid bills.”

One reflection of the problem is the high number of people reporting issues with medical debt to the Consumer Financial Protection Bureau’s complaint database. A Utah resident, for example, wrote that a growing stack of medical bills led to late mortgage payments; another, from Florida, said the debt hurt their credit score. “It was only when my health began failing and I began accruing medical bills that I started falling behind [on my] bills,” wrote a third, from Louisiana.

Get Ahead of Big Bills

A little planning can go a long way toward keeping costs under control.

Know the costs up front. A new law gives people without insurance the right to a “good faith estimate” of charges prior to a planned procedure or test. But there’s nothing that stops even people with insurance from asking for that information, says Patricia Kelmar, a health policy advocate at the U.S. PIRG (Public Interest Research Group), a consumer advocacy organization. Share that estimate—which includes everything planned for your medical care—with your insurer. This way you can find out what is covered, how well, and what you may be expected to pay out of pocket.

Speak up at the doctor’s office. More people report being afraid of high medical bills than being afraid of becoming ill, according to a 2019 study from the CFPB. Yet many are also afraid to discuss cost concerns with their doctors, says Caitlin Donovan, a healthcare policy expert at the Patient Advocate Foundation, which helps consumers with medical bills. Such a conversation could prompt your doctor to find ways to trim expenses, she says—for example, by prescribing less expensive medications or limiting office visits. “But they won’t know cost is an issue unless you bring it up.”

Make sure your provider has all your insurance information. You could have two, three, or possibly more types of insurance that could be applied to different aspects of your care. For example, you could have insurance through your employer and also be covered under your spouse’s plan. Or you may use traditional Medicare, a supplemental plan, and the Part D drug benefit. Busy doctors’ offices and the complexity of insurance can mean information about one or more of those plans doesn’t make it onto your record. Confirm with all your providers that your insurance profile in their system is complete, Donovan says.

If you’re on Medicare, consider buying supplemental insurance. Traditional Medicare—Part A for hospital care and Part B for other medical care—is what most people sign up for when they turn 65. In addition to premiums, with these plans you are also responsible for deductibles, copays, and coinsurance. To help with those costs, private companies offer coverage known as Medicare Supplement Insurance, or Medigap, which can run about $150 per month, says Jack Hoadley, PhD, research professor emeritus at the Health Policy Institute at Georgetown University in Washington, D.C.

Supplemental plans cover most of the costs traditional Medicare doesn’t—including the 20 percent you’d have to pay for physician bills, Hoadley says. About 1 in 5 beneficiaries of traditional Medicare had no supplemental coverage in 2018, according to the Kaiser Family Foundation. “For seniors, it’s really the biggest piece of the puzzle to avoiding large medical bills,” Hoadley says.

Good to know: It is important to sign up for Medicare supplemental coverage when you first become eligible, Hoadley says. During the initial enrollment period your application will be accepted regardless of your health status. After that you’re likely to be asked to get a health screening and could be denied coverage or charged more based on your conditions.

Illustration: Domenic Bahmann Illustration: Domenic Bahmann

Or consider Medicare Advantage. If you can’t afford a supplemental plan, this might be a less expensive option. Advantage plans cover Parts A and B, and sometimes D, and can cover some of the out-of-pocket costs that traditional Medicare doesn’t. Some charge no additional premium beyond what you already pay for Part B.

But because Advantage plans are offered by private companies that contract with Medicare, the network of doctors who take it is usually smaller and can change every year. “It can be a great deal if your doctors participate in the network,” Hoadley says.

Plans typically cover drugs and some dental, vision, and hearing care—and sometimes even extra perks, such as gym memberships—and have good coverage for everything else after your deductible is met, Hoadley says. Deductibles can be zero to several hundred dollars, depending on the plan, he says.

Good to know: You can sign up for an Advantage plan around the time you turn 65 regardless of your health status, Hoadley says. But if you decide to later switch to traditional Medicare, you may need a health screening for a supplemental plan to go with it, unless, for example, you moved out of state or your Advantage plan left the market.

See whether you qualify for a Medicare Savings Program. People with limited income and few assets beyond a home and car could qualify to have deductibles, premiums, coinsurance, and copayments covered, depending on the state where they live. To find out, get contact information for your state Medicare office at medicare.gov/talk-to-someone (select your state from the drop-down menu).

It’s possible, too, that you may qualify for Medicaid, especially because most states have expanded eligibility requirements so that coverage isn’t limited to those living at or below the poverty line.

What to Do If Bills Pile Up

You can take all the right steps and still get a big medical bill, of course. To keep financial trouble at bay, try the following.

Never automatically pay a hospital or provider bill. That’s because a doctor’s office or other facility should first send their invoice directly to your insurance—Medicare, supplemental Medicare, Medicare Advantage, or private insurer—to see how much of the bill will be covered, Donovan says. If you have insurance and get a bill from a hospital or doctor, contact the provider to make sure the bill was submitted to your insurance. Once it has been, your insurer should send you a summary notice or an explanation of benefits that shows any remaining amount owed.

Make sure the bill is correct. Almost half of all medical bills contain at least one error, including duplicate charges or charges for services you never received, Donovan says. If you face a high bill and are on the hook for some portion of it, request a bill itemizing everything you were charged for and go through it line by line, she says. Find something? Dispute any charges that shouldn’t be there with the provider.

Dispute charges related to medical errors. Say you developed an infection in the hospital after having your knee replaced. At the very least, you should challenge any extra charge for care needed to treat that infection. You could even consider asking about a discount for the original procedure, especially if the error caused you to miss work or triggered other financial harm. There’s no guarantee that even the extra charge will be forgiven or discounted, Donovan says, but it’s worth a try.

Ask about a hospital’s financial assistance programs. Nonprofit hospitals must by law provide financial assistance. Some states—California, Colorado, Connecticut, Illinois, Maine, Maryland, Nevada, New Jersey, New York, Rhode Island, and Washington—require all hospitals to offer discounted or free care to many people with low incomes. Even if you live in another state, “there’s no shame in asking for financial help,” Donovan says. The CFPB’s most recent report on medical debt found that hospitals didn’t always let patients know financial assistance was available unless they asked. And a 2019 Kaiser Health News analysis found that almost half of nonprofit hospitals billed patients who would have qualified for free or discounted care.

Negotiate. It’s in the provider’s interest to work with you to obtain payment, Donovan says. So determine what amount per month you can reasonably pay after accounting for housing, food, fuel, and other necessities. Also ask that no interest be charged. Or if you have the funds, you can also offer a one-time payment for a reduced total bill, she says. Doing so can save you 15 percent or more.

Get help. Free assistance is abundant. The Medicare Rights Center, for one, can walk you through the process of choosing among types of Medicare plans. Contact the center weekdays during business hours at 800-333-4114 or go to medicarerights.org.

Another option: State Health Insurance Assistance Programs, which are operated by qualified staff and volunteers to help you wade through all the Medicare choices in your state. They can also connect you with your state Medicaid office, says Hoadley, who volunteers in his state of Virginia. Find your state’s contact info at shiphelp.org.

Need a hand understanding and negotiating your medical bills? For many, the Patient Advocate Foundation provides those services and more, free of charge. Contact the organization at 800-532-5274 or go to patientadvocate.org.

Consider hiring an advocate. Look for a medical billing specialist through the Alliance of Professional Health Advocate. Then check to make sure that the specialist you find has credentials from the Patient Advocate Certification Board.

When it comes to paying a bill you can’t cover with money in your checking account, reaching for your credit card can be automatic. But there are serious reasons to think twice about doing that for medical bills, says Patricia Kelmar, a health policy advocate at the U.S. PIRG (Public Interest Research Group), a consumer advocacy organization.

The first is that you could wind up paying interest on a balance owed after 30 days, which, depending on the size of the debt and how long it takes you to pay it off, could cost you hundreds or thousands of dollars extra. That compares with payment plans that some hospitals or healthcare providers can arrange and that might charge low or no interest, Kelmar says. And, she says, those “will likely let you set an amount that you can afford to pay each month.”

Second, paying a medical bill with a credit card means it will be treated like any other debt if it goes unpaid, she says. It can wind up in collections and be reported on your credit report, potentially lowering your score. And because it is credit card debt and not medical debt, it can remain on your report for up to seven years even after it has been paid.

On the other hand, any payment plan negotiated with a hospital or doctor’s office will stay off your report altogether if you pay it off.

And if there is a billing or payment problem, you’ll have 12 months to resolve it before the debt appears on your credit report.

Editor’s Note: This article also appeared in the June 2022 issue of Consumer Reports magazine.

Correction: A previous version of this article, originally published on May 5, 2022, included the incorrect phone number for the Patient Advocate Foundation.