Brace yourself: Within a few years, your only choice for health insurance through your employer may be a high-deductible health plan.

These plans have smaller monthly premiums, but there's a trade-off: You have to pay a lot more out-of-pocket before your insurance begins to cover a portion of your bills. Those up-front payments, or deductibles, as defined by the IRS (PDF), are a minimum of $1,300 per year for individual insurance coverage and $2,600 for a family. And that's only the minimum.

In reality, individuals are paying an average $2,295 before insurance kicks in and families are ponying up $4,364 on average, according to the Kaiser Family Foundation. That's a heavy financial burden for many of them.

A result: More people are skipping or postponing medical care because they can't afford to pay so much up front.

Faced with steep healthcare costs, many companies are embracing these plans because they push more of the cost onto workers. That's a big deal, because more than half of Americans get health insurance through their employer.

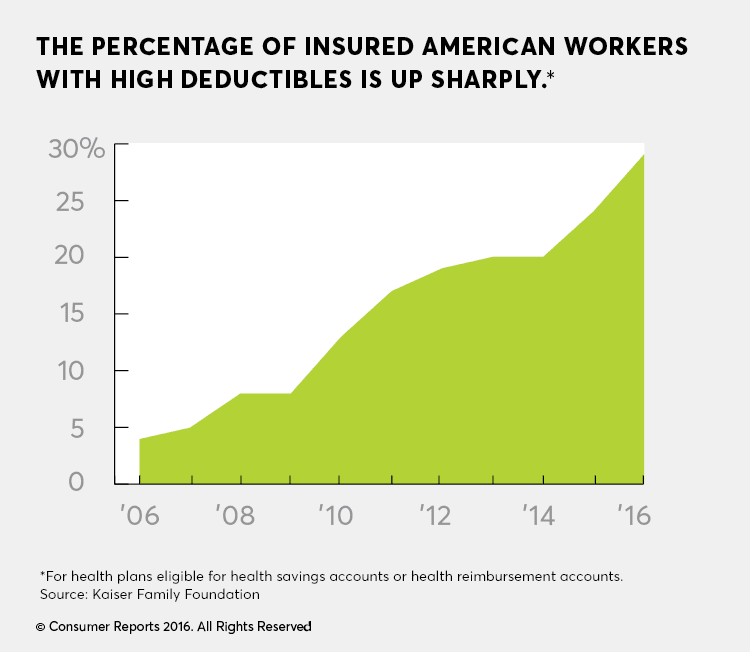

Within three years, almost 40 percent of companies that offer health insurance may make high-deductible plans the only choice, according to a survey by the consulting firm PwC. A quarter of all companies are already doing that. In 2012, it was just 13 percent.

High-deductible plans are also the norm on the Affordable Care Act (ACA) exchanges. Even though there is uncertainty about the ACA long-term, almost 14 million Americans (PDF) are expected to get health insurance on the exchanges in 2017.

In 2016, two-thirds of people on the exchanges were enrolled in Silver Plans, which have relatively low premiums. But the average deductible for a Silver Plan this year is $3,572 for an individual and $7,474 for a family, according to the health insurance data website HealthPocket. Those are eye-popping numbers, but individuals who earn less than $29,700 and families that make less than $60,750 may qualify for cost reductions on those deductibles.

Find out how to get high-quality, low-cost healthcare and where CR stands on high-deductible health plans.

The Downside of High Deductibles

Why are people who are shopping for insurance choosing high-deductible health plans? Sometimes it's because they like the idea of paying lower premiums, and they assume they will stay healthy enough so it will save them money, says Kim Buckey, vice president of client services at DirectPath, a benefits and compliance management firm. For others, there's no choice.

That was the situation two years ago for Monique Dow, a 46-year-old mother of two from Watsonville, Calif., who had a $6,000 deductible with her family's health insurance plan, the only option offered by her husband's employer.

For months she put off surgery to remove what her doctor thought were benign fibroid tumors and a polyp in her uterus. When she eventually scheduled surgery after working out a payment plan with a hospital, the polyp was found to be cancerous, requiring a hysterectomy.

"I waited all that time, not knowing that I had this growing in me," Dow says. "If we had a lower deductible, I probably would have been treated a lot sooner."

Dow is cancer-free but requires frequent monitoring. Now she's weighing another insurance dilemma because her husband started a new job. A high-deductible plan is one choice, but it's an option they want to avoid, she says.

#HighDeductible is a hot topic on Twitter. Join in the discussion with other people feeling the pain of a high-deductible health plan.

Are Consumers Really in Control?

High-deductible plans are part of a move to what's called consumer-directed healthcare. The idea is that if you're more on the hook financially for the medical choices you make, you'll take more control, for example, by shopping around for less costly procedures and providers, and by not running to a doctor every time you come down with a cold.

Sharing the cost of your healthcare, the thinking goes, should drive down your overall medical bills.

Only that's not what's happening. Faced with daunting deductibles, many people like Dow are postponing the care they need and sometimes ending up sicker and with bigger bills down the road, a growing body of research is finding.

A 2015 survey by Families USA found that almost 30 percent of people with deductibles higher than $1,500 for individual coverage avoided medical care—tests, treatment, follow-up care, and prescription drugs—because they couldn't afford the out-of-pocket costs.

That kind of cost-sharing encourages people to use fewer services, according to Gary Claxton, a vice president at the Kaiser Family Foundation. "Some of that is appropriate," he says, "but it can lead to some really bad choices. When someone puts off care, they may end up needing more care and spending more later on."

How to Make the Best of an HDHP Plan

It's not that high-deductible plans are a poor choice for everyone. If you're healthy, you don't need to go to a doctor for more than routine screenings, and you have a savings cushion to cover your deductible, paying lower monthly premiums may be a reasonable option.

Still, Consumer Reports and other consumer advocates say that too many people have plans they can't afford or don't understand. (Read about where CR stands on high-deductible health plans.)

For now, if you have a high-deductible plan or think you will soon, you'll have to be more involved in decisions about your healthcare. But there's a lot you can do to make the plan work better for you.

Consumer Reports consulted health-policy and insurance experts, talked with doctors, and conducted our own research to uncover the most cost-effective ways to use your high-deductible plan while getting the medical services you need.

Know what's free. Many routine health services intended to keep you well or catch problems early (including colonoscopies, mammograms, and vaccinations) are free in all insurance plans now. Yet only one in 10 people in high-deductible plans said they knew such screenings were free, and almost 20 percent said they avoided preventive tests because they thought they would cost them, according to a 2012 study published in the journal Health Affairs. So make sure you go to a doctor for the care you're entitled to get.

Comparison shop. High deductibles are supposed to nudge you to shop around for lower prices for nonemergency care. But few people are doing that. Most health insurance sites provide information on where to find in-network services. And some offer cost-estimator tools that give the price you'll pay different providers for, say, an MRI or knee surgery. But a Consumer Reports Health Ratings Center study of 21 insurance plans found that only 13 percent of people used the tools on their insurer's site, even though 75 percent said they were concerned about cost and the quality of service. One reason is that people simply aren't aware that those tools exist. (If your health insurance company doesn't offer one, call your insurer directly to ask for quotes.)

Spending the time to research costs can be worth it. Prices for medical treatments can vary considerably from provider to provider, even within the same city. In Kansas City, Mo., for example, the average price for bunion surgery is $4,094, but it ranges from $3,136 to $8,150, according to Gooru.com. For medication, one of the biggest out-of-pocket expenses for consumers, check GoodRx, a website where you can compare prices for thousands of prescription drugs at more than 70,000 pharmacies in the U.S.

But don't shop by price alone. Among the insurance websites Consumer Reports evaluated, a majority scored well on price information. But users said that the sites were difficult to navigate and that they lacked information on the quality of services from sources, such as independent ratings of doctors and hospitals, and user reviews. (See our ratings of six national insurer websites.)

"Prices vary a lot, but quality does, too," warns Orly Avitzur, M.D., a neurologist and medical director of Consumer Reports. When one of her patients, Amir Goen, 42, of Tarrytown, N.Y., needed an MRI recently, he found that the prices for the test in his area varied by hundreds of dollars. He consulted with Avitzur, who advised him to ask about the strength of the magnets used in the imaging. Goen discovered that the cheapest MRI didn't use the highest-strength magnet—but neither did the priciest one.

For California residents, check out our cost estimator tool that allows you to find both quality information and cost information for providers and healthcare services in your state.

Interview your doctor. As Goen learned, doctors can be a valuable resource for patients trying to balance cost with quality of care. Researchers at Duke University analyzed recorded conversations from 1,800 doctor visits. Cost came up 30 percent of the time. And in almost half of those conversations, doctors offered ideas about how patients could find less expensive prescriptions, diagnostic tests, or other health services. You can also use online resources such as ConsumerHealthChoices.org, which Consumer Reports created as part of its partnership with the ABIM (American Board of Internal Medicine) Foundation's Choosing Wisely campaign. Those resources provide questions to ask your doctor about medical tests and treatments that are frequently overused. Many of them might waste your money and do more harm than good.

Get care on the calendar. Keep track of your spending against your annual deductible, which resets every year. If you expect you'll need an expensive procedure that will get you close to or over your deductible, schedule it early in the year if you can. That way, if you need more care later in the year, your insurance will kick in. And don't put off making doctor appointments. Make sure your physician has room in his or her schedule before January 1, when your deductible resets.

Leverage tax breaks. You can ease the pain of high out-of-pocket costs by putting money into a health savings account (HSA), which most people in IRS-designated high-deductible health plans are eligible for. That's pretax money—up to $3,400 annually for individuals and $6,750 for families—that you can use to pay for qualified medical expenses, including your deductible. And if you don't use your HSA funds, they roll over and can grow tax-free, year after year.

Employers don't have to set up HSA accounts for their employees in high-deductible plans, but about 63 percent do. (You can also open an HSA on your own.) The account is portable, so the money is yours if you change jobs. To encourage the use of HSAs, about half of employers offer seed money. Some will deposit additional money into your HSA if you take advantage of preventive services like screenings and wellness visits. "Employers don't want workers to skimp on needed care," says Steve Wojcik, vice president of public policy at the National Business Group on Health.

Don't freak out. High-deductible insurance can be hugely expensive, but at least there's a limit to how deep you'll have to dig into your own pocket for health services. The Affordable Care Act mandates that almost all insurance plans cap out-of-pocket costs (not including premiums or out-of-network care). After you've hit the max, the insurer must pay 100 per-cent of in-network costs.

For 2017, all ACA plans have an out-of-pocket maximum of $7,150 for individual coverage and $14,300 for family plans. Employer plans can vary, but only 18 percent of those with out-of-pocket limits make you responsible for more than $6,000 for an individual, according to the Kaiser Family Foundation. Remember that only in-network charges count against your out-of-pocket limits (or your deductible, for that matter). So stay in-network. That's good advice for all of us, whether we're in a high-deductible plan or not.

Where CR Stands On High-Deductible Health Plans

There's no argument that high healthcare costs need to be reined in. But Consumer Reports doesn't think consumers should bear the brunt of that responsibility through insurance plans with enormous out-of-pocket costs. Instead, we believe that employers, the government, and medical-service providers—as well asconsumers—must work together to lowerthe underlying costs of healthcare.

The idea behind high-deductible plans (or HDHPs) is that if consumers face the consequences of their health spending, they will spend their dollars more wisely.

Instead, those cost-sharing plans are causing considerable consumer harm, says Lynn Quincy, director of CR's Healthcare Value Hub. Almost all of the savings that they generate are due to people cutting back on healthcare services. They postpone going to a doctor, don't fill prescriptions, or cut back on preventive care. Most troubling is that the sickest workers may cut back on care. What's more, several studies have found that consumers in HDHPs do no more price shopping for medical services than the average person. They also fail to use free preventive services.

To control spending and bring better value (not just lower costs) to our healthcare system, CR believes we need a different vision of what the consumer's role in healthcare should be. These are some strategies we suggest:

Focus on the root of the problem. Encourage healthcare providers, hospitals, drugmakers, and medical-device makers to address high healthcare costs. We need to cut unnecessary spending and reduce expenses, not just push the cost onto consumers.

Change plan designs. Make costs more predictable by using co-payments (a flat charge you pay each time you go to a healthcare provider) instead of coinsurance (which requires you to pay a percentage of the cost of a covered health service). Make more services not subject to a deductibles. And give consumers timely, accurate, and actionable information to help them make decisions and find high-value care.

Involve state regulators. They need to gather data to understand healthcare spending in their state, see where consumers are experiencing high costs, and determine which markets lack competition, which holds down prices.

Go to ConsumersUnion.org/highhealthcosts for more information.

Editor's Note: This article also appeared in the January 2017 issue of Consumer Reports magazine.