How can relatives confront contentious money concerns without dynamiting family ties? Because personal finance is as much personal as it is finance, we asked experts from a range of disciplines—finance, law, psychology, and even preschool education—to address common family money scenarios. Here's how to handle a particularly difficult conversion with an elderly parent who may need to cede control of his or her finances to you. We've added our own practical advice.

Proud Parent, Delicate Conversation

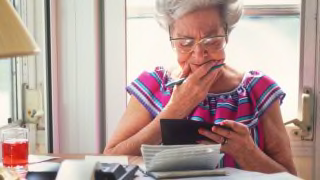

Your elderly mom lives alone and has been doing fine for years. But the last time you visited, you saw that she'd written a large check to a doctor—a bill you know insurance already paid. You suspect she might be losing her ability to handle her finances, and you fear she could be vulnerable to scams. But she has always been proud of her money-management skills and is unlikely to easily hand her purse strings to you.

A geriatric care manager's take. The best approach is a gradual one that doesn't make your mother feel criticized or disempowered, says Patricia Maisano, founder and chief innovation officer of Ikor International, a care-management company for seniors and those living with disabilities, based in Kennett Square, Pa. "Start by saying, ‘I know you're doing the best you can with your bills, but everyone needs somebody to check on things once in a while,' " Maisano says. She suggests that you correct the doctor's bill error and offer to help your mom with bill management. "You can say something like, ‘Bills can be difficult. I get overwhelmed. How would you feel if we sat down and looked over them together?' " You may progress to taking over the task eventually. "The secret to a successful transition," Maisano adds, "is to make your mom want your help, not force it on her."

More on Family Money Issues

Other Perspectives

An elder-law attorney's take. "Giving up an independent activity—driving, money management, food shopping—is a painful transition for any older person to make," says Bernard Krooks, an estate and elder-law attorney based in New York. "One way to get your mother's cooperation is to say, ‘I'm starting to talk to my kids about what to do if I'm incapacitated. I think we should talk about that, too.'" In Krooks' view, your goal should be to get your mom to let you see copies of her bank statements without making you a co-owner of the account. "That way she's still in control, but you're overseeing," Krooks notes. Tell her you want to work together with her. He adds: "To the extent she views you as treating her as a child, there will be resistance." Ideally, she would also grant you durable power of attorney, so you can make financial decisions on her behalf in the event that she becomes unable to make her own.

CR says. If you can't or don't want to handle your mother's finances, engage someone reliable who has trained in managing seniors' and disabled individuals' routine money tasks. The American Association of Daily Money Managers has a volunteer page that links consumers to individuals who will do the job free or for low fees in many states. You also can search for a paid professional daily money manager who has agreed to standards of practice and a code of ethics. Their hourly rates can range from $75 to $150 depending on the service; some charge a monthly retainer for, say, acting as power of attorney. Certified DMMs, also listed on the site, go a step further, having passed an exam and undergone a background check. They must have at least 1,500 hours of daily money-management experience.

Editor's Note: This article also appeared in the May 2017 issue of Consumer Reports magazine.