Sarra Herzog, 46, and her husband, Marc, 44, appear to have achieved the dream of upper-middle-class financial success. They live in northern New Jersey, in a community noted for its charming Victorian houses, vibrant downtown, and excellent school system. She's a communications director for a biopharmaceutical firm, and he's an account executive.

But for the Herzogs, reestablishing financial security has been a 13-year struggle. Marc was downsized from his job in 2006. In the aftermath of the Great Recession of 2008 to 2009, he found new jobs only to be laid off twice, finally landing a new position earlier this year.

The couple have tried to preserve their priorities. To cope with long periods of reduced income, they slashed their spending while still maintaining college savings for their daughter, Sophia, now 12, as well as paying down credit card debt. "We had to make trade-offs," Sarra says. "I've lowered my 401(k) contribution just to pay the utility bills. We take virtually no vacations, and Marc just got his first pair of shoes in almost three years."

In addition to the years of scrimping, the Herzogs have had to significantly ratchet down their expectations for retirement. "My baby boomer parents recently took a monthlong trip to Australia, but that will never ever happen for my husband and me," Sarra says. "I believe the ability for our generation to achieve as much as the baby boomers did is just unreachable."

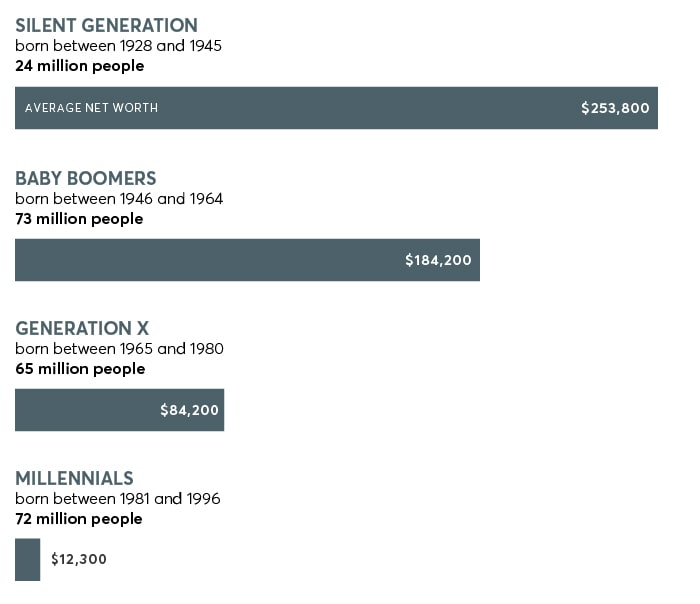

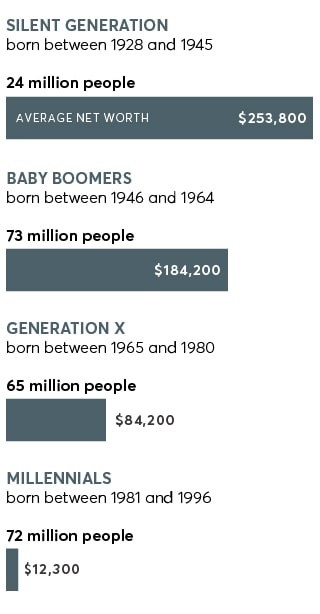

Source: Pew Research Center analysis of U.S. Census Bureau and Survey of Consumer Finances data.

Source: Pew Research Center analysis of U.S. Census Bureau and Survey of Consumer Finances data.

Dreams Derailed

The Herzogs' financial struggles are shared by many of their Generation X counterparts, a group ranging in age from about 39 to 54. Gen Xers are in quintessential midlife—making mortgage payments, funding college educations, and saving for retirement, which is looming ever closer. The difference between them and other generations is that the Great Recession hit them at a vulnerable moment, just as they were establishing themselves in the workforce and starting to buy homes. And that derailed their efforts to build wealth and long-term financial security.

It's no small wonder that Gen Xers lag behind other generations on most financial measures at this point in their lives. Only 65 percent of people between ages 40 and 51 owned their own home in 2016, according to a recent study by the Employee Benefit Research Institute (EBRI), a nonprofit group. But when today's baby boomers were in that age range, 75 percent owned homes. And fewer Gen Xers have a retirement plan: just 66.9 percent in 2016 vs. 71.5 percent of baby boomers when they were 40 to 51 years old.

Granted, Americans of all ages were hurt by the recession. Nearly 60 percent of workers 18 and older say that even now they haven't fully recovered, and 8 percent say they may never recover, according to a recent survey by the nonprofit Transamerica Center for Retirement Studies. Still, those furthest away from retirement—millennials and Gen Xers—seem to have found it the most debilitating. Almost 25 percent of them say they haven't begun to recover or think they may never recover from the recession vs. 19 percent of baby boomers.

Even those who have regained their footing have lost valuable time. Twelve years ago, Mark Schneider, 53, and his wife, June, 48, of Parker, Colo., never thought they would fall so far behind in reaching their goals. The parents of two children, now 14 and 16, they were working in what seemed to be secure jobs, Mark at an investment firm and June at a telecom company. "We were flush," June says. "We used my income for savings and travel, and we ate out a lot."

But in 2008, as the stock market tanked and investment firms cut staff, Mark lost his job. It was two years before he landed a new position, at an insurance company, and it paid far less than he was earning before. The couple couldn't keep up with their living expenses, including June's student loan payments and mounting credit card debt. They declared bankruptcy in 2011 and sold their house. "We survived," June says. "But I never want to go through that again."

After renting for several years, the Schneiders were able to purchase a smaller house last year—1,500 square feet vs. the 3,000-square-foot house they used to own. They're making improvements, including finishing the basement. Further bolstering their finances, they rebuilt their credit and accumulated enough savings for an emergency fund to cover a year's worth of expenses, and June paid down her student loans. "It's great that we're back on track," she says, "but we're only back to where we started." And they have fewer years to save for their kids' college education—and their own retirement.

The Rocky Road to Recovery

For many people, just getting back to where they started is a tough challenge. Median wage growth averaged just 0.3 percent a year between 2007 and 2018, according to the Economic Policy Institute. And yet other essential costs have skyrocketed. Average family healthcare premiums, for example, have climbed 55 percent since 2008, rising twice as fast as workers' wages.

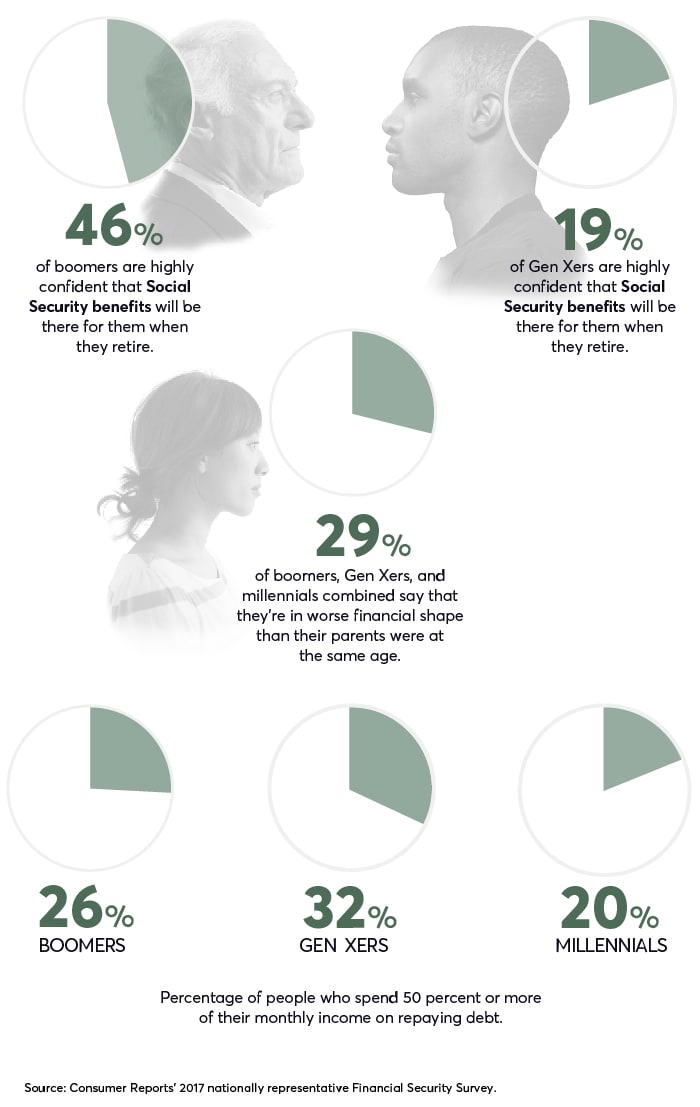

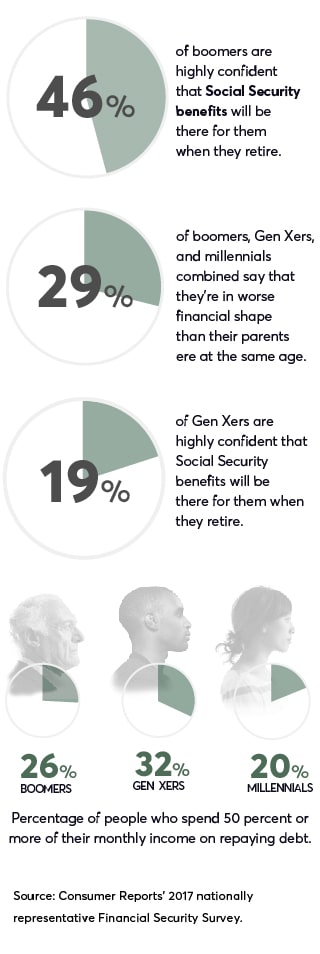

Then there's the recession's most enduring legacy—debt—which has also had a disproportionate impact on Gen Xers. One out of 3 Gen X households is spending at least half its income on debt, a higher percentage than baby boomers or millennials are spending, according to a 2017 nationally representative survey by Consumer Reports. And a recent study by Experian found that Gen Xers have the highest average total debt of all the generations—$138,916—nearly 50 percent more than the national average.

That burden of debt compounds an already precarious retirement. Gen Xers have skimpier retirement benefits than previous generations. Only 18 percent expect to receive a traditional defined benefit pension, compared with 30 percent of boomers, according to the Transamerica survey.

"Gen X is going to be the first generation to rely mainly on 401(k) and IRA savings for retirement," says Craig Copeland, senior research associate at EBRI. "Whether they can accumulate sufficient assets, as well as manage them for income in retirement, will be a test case going forward."

What's more, for those hit hardest by the recession, the very idea of trying to start saving may seem so daunting that they lapse into inaction. "It's not surprising that many Gen Xers are paralyzed," says Derek Tuk, a certified financial planner in Boulder, Colo., and a Gen Xer himself.

The statistics bear him out. Only 31 percent of Gen Xers have figured out how much they need to save for retirement, according to the EBRI survey. And that figure is lower than for boomers and millennials. With retirement just around the bend, only 56 percent of Gen Xers say they're doing a good job preparing for it financially, EBRI data show. Among Gen X households with retirement plans, the median account holds just $60,000. That compares with $115,000 for boomers and $15,900 for millennials.

Retooling Your Retirement

Despite the challenges, it's not too late to achieve a comfortable retirement. "Gen X is at an age where—if they focus—they have time to catch up," says Catherine Collinson, CEO and president of the Transamerica Center. For boomers and millennials as well, the key is to follow a disciplined savings and planning strategy, as we'll explain.

1. Scrutinize your finances. No matter how scary or depressing it seems, you have to face the financial facts of your life head-on. Get a handle on how much you bring home every month after taxes and deductions, and then how much you spend each month. You can do this relatively easily with online tools such as Mint (free) or YNAB ($84 per year), which can help you monitor your transactions. Your bank or credit card website may also track these numbers for you.

2. Cut the waste. The previous step may lead you to discover fat in your spending, such as paying for overlapping streaming services or making auto-renew payments for a service you no longer need. "I noticed there were Netflix charges month after month," says Guy Richie, 52, a Realtor in Brentwood, Tenn. "They weren't significant—$8 to $12—so I didn't spot them before, but it turns out my wife had signed up for a subscription but didn't even realize she still had it."

3. Deal with debt. If you have credit card debt at a high interest rate, say, 17 or 18 percent, make it a priority to pay that balance down as soon as you can. Mounting credit card debt can be a financial disaster at any age, but once you've reached midlife, it can wreck your retirement. "This is a Gen Xer's kryptonite," says Mari Adam, a certified financial planner in Boca Raton, Fla. "High-rate credit card debt is toxic."

The most effective strategy is to target the highest-rate debt first, which will result in a quicker reduction of the balance. But if you need a psychological kick-start, pay off smaller balances first. That "convinces people they're making progress," explains Ryan Marshall, a Gen Xer who's a certified financial planner in Wyckoff, N.J.

4. Take a hard look at big-ticket items. To free up significant amounts of cash, you might need to focus on your biggest budget items, which are typically cars, vacations, and housing. For many families, opting for a "staycation" or postponing a new-car purchase is relatively doable.

It's tougher to cut back on housing because home prices in many areas are rising. But downsizing may be a practical option, especially if you're willing to change neighborhoods. "It used to be mainly retirees who left for lower-cost areas," Marshall says, "but I'm seeing more people in their 50s considering this move."

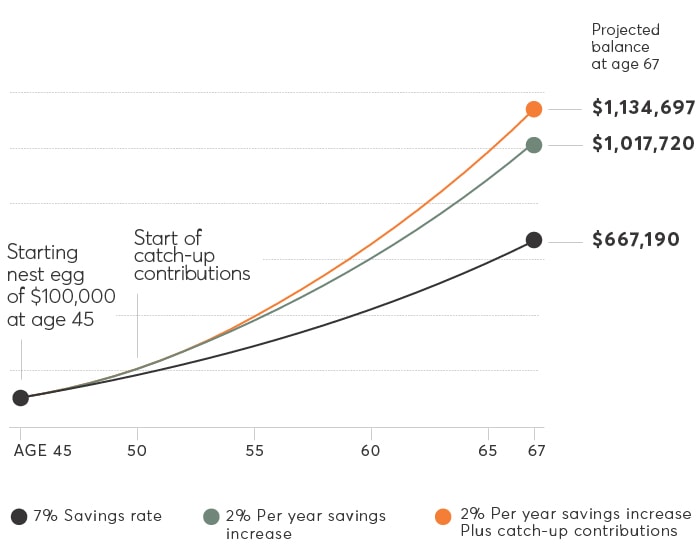

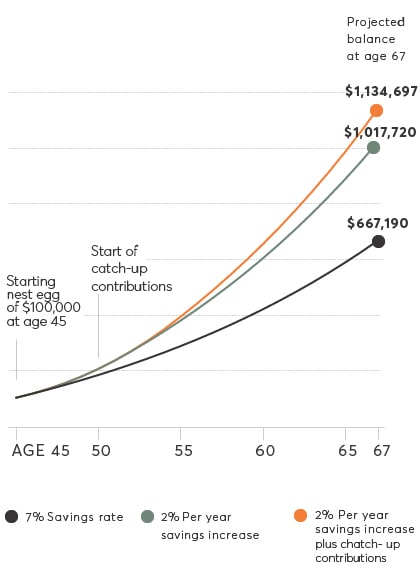

5. Treat retirement savings as sacred. For Gen Xers and baby boomers with employer-sponsored retirement plans, it's crucial to take full advantage of the opportunity to save in tax-deferred accounts and get any matching contributions. (If you don't have a company retirement program or you're self-employed, opt for an individual retirement account or a solo 401(k) plan instead.) If you're older than 50 and you have the cash to spare, socking away more with catch-up contributions (available to those in that age bracket) is also a great idea.

Many Gen Xers make the mistake of tapping their retirement accounts prematurely. More than 30 percent have taken a loan, an early withdrawal, or a hardship withdrawal from a 401(k) or an IRA, according to the Transamerica survey. Sometimes emergency withdrawals are unavoidable, but if you can, try to find another way. When Mari Berryman, a 44-year-old social worker in Los Angeles, wanted to save for a down payment as well as college costs and retirement, the divorced mother of four took part-time jobs in addition to her full-time job at a kidney dialysis center. "I'm trying hard not to touch my 401(k), so I pretend like it's not there," says Berryman, who expects to reach her down-payment goal in early 2020.

6. Stay employable. One of the most effective ways to improve your financial security is to work longer, says Geoff Sanzenbacher, associate director of research at the Boston College Center for Retirement Research (CRR). The average annual growth rate of workers 55 and older is projected to be 1.8 percent this year, more than three times the rate of growth for the overall labor force, according to the Bureau of Labor Statistics. Someone earning an average wage who starts saving at age 45 would need to put away 27 percent of his salary annually to retire comfortably at age 65, according to CRR's research. Aim to retire at age 70 and he would need to save just 10 percent.

But the harsh reality is that many older workers get pushed out of their jobs. In a recent AARP survey of 3,900 adults 45 and older, 61 percent reported they had experienced or witnessed age discrimination in the workplace. To stay employable, take advantage of training opportunities offered by your employer or develop new skills outside your workplace, says Kerry Hannon, author of "Great Jobs for Everyone 50+: Finding Work That Keeps You Happy and Healthy . . . and Pays the Bills" (Wiley, 2017). Or start planning to make a transition to a second career, a process that could take three to five years, or find a part-time job.

Editor's Note: This article also appeared in the October 2019 issue of Consumer Reports magazine.