The Internal Revenue Service has released its new tax-withholding tables, giving Americans a first look at how the tax-cut law will affect their take-home pay this year.

But anyone who wants to get a sense of what their paycheck may actually look like will find the process tedious and inexact.

The tables, published this week, offer just a rough draft of what taxpayers will owe the government, says Mark Luscombe, principal federal tax analyst for Wolters Kluwer Tax & Accounting, a tax software company based in New York.

"They're just going to give you a number that you can compare with your current withholding and say, ‘My take-home pay will go up or down,'" he says.

But because of the many other changes in the tax law—for instance, the higher standard deduction and increased child tax credit—taxpayers won't know for sure whether they've under- or overwithheld until they prepare their taxes next year, he says.

"As is always the case, it won't tell you everything," Luscombe says.

The Wait for Paycheck Updates

Now that the new withholding tables are out, employers will be scrambling to update paychecks for employees reflecting the new tax rates and brackets. The Treasury Department has said it expects employers to have made those changes by Feb. 15, though it has yet to create new W-4 withholding forms to reflect the new law.

Until those forms are out, employees won't be able to make changes themselves to get closer to their proper withholding.

The IRS' online withholding calculator also won't be ready until mid-February, the agency says. Once that free interactive tool is ready, the agency encourages taxpayers to use it to determine their proper withholding. (It requires no input of personal information such as your name or Social Security number, though you will have to input your income and some other particulars.)

Figure It Out Yourself If You Dare

If you are itching to get an idea of how much money you'll have, use the tables to do the figuring, Luscombe says. Here's how:

• To find out what your withholding will be, first ask your employer how many personal withholding allowances you've claimed in the past.

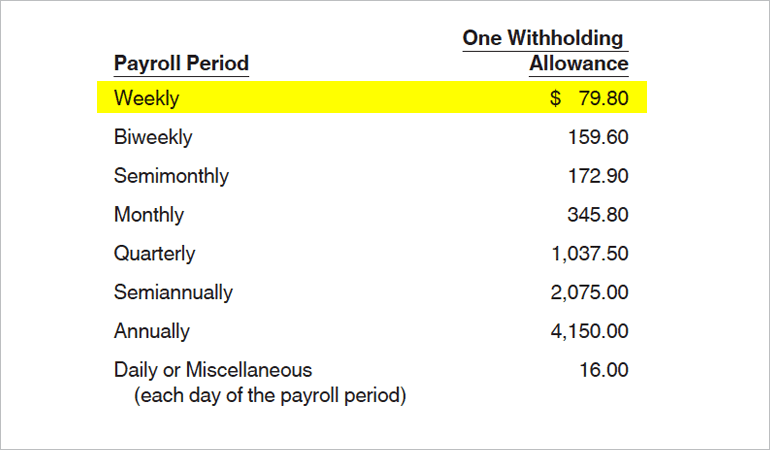

• Download IRS Notice 1036, which is linked on the top line of this page.

• On page 1 of Notice 1036, multiply the number of your withholding allowances by the figures in the chart. For instance, if you get a weekly paycheck and claim two withholding allowances, you would multiply $79.80 times 2 to get $159.60, which is your new withholding allowance.

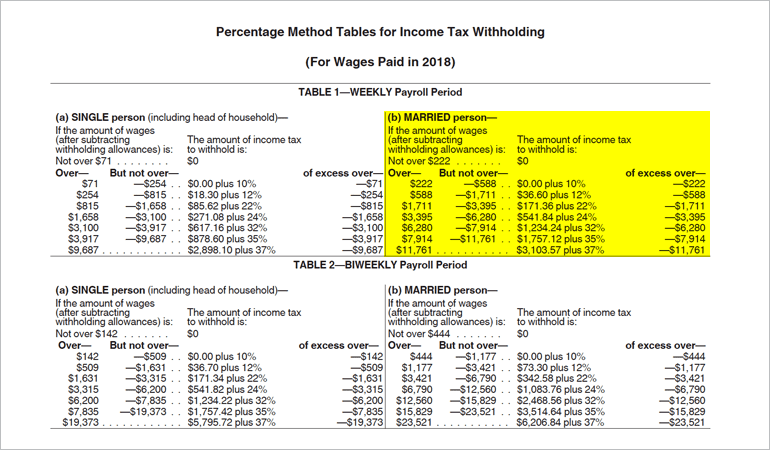

• Now you have to find the right tax table. Using the tables on page 2, find the profile that best fits you. For example, if you're married and file a joint tax return and you get a paycheck weekly, use Table 1, right-hand side.

• Now subtract your withholding allowance from your gross pay. In the above example, if you make $1,000 per week and have two withholding allowances equal to $159.60, what's left over is $840.40. That's the sum that will get taxed.

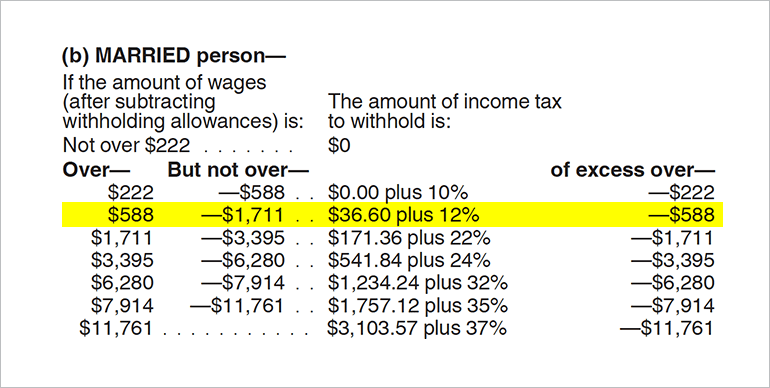

• Choose the row in the table that matches your weekly taxable income, and follow the instructions. Continuing with the prior example, you'd choose the second row (below) because your taxable income of $840.40 is between $588 and $1,711.

• Subtract the first number in that row from your taxable income. In this case, you'd subtract $588 from $840.40 to get $252.40.

• Then multiply that figure by the tax rate shown on the line. In this case you'd multiply $252.40 by 12 percent to get $30.28.

• Finally, add that result to the figure in the third column to get your weekly withholding. In this example you'd add $30.28 to $36.60 to get your new weekly withholding: $66.88.

"It's tedious," Luscombe says. "That's why most people will wait for the calculator."

You Still May Have to Make Changes Later

Whether you use the calculator or the new tables, keep in mind that the withholding for January will be under the old, less generous tax rates, so you could end up overwithholding by the end of the year, Luscombe says.

"People will have to either adjust their withholding on their own later in the year or wait for a bigger refund next year," Luscombe says.