Sign In

The Great Recession that started in late 2007 turned the American shopper—famous for our free-spending ways—into the American scrimper. Thanks to the downturn we've been buying less of everything from housing to haircuts, driving our cars till they drop, and putting off big life moments such as getting married and having babies.

But guess what? After seven years of belt tightening, Americans are showing a new optimism. We're ready to shop again. But we're not the same old spendthrifts we used to be; this harrowing economic era has changed America's buying habits, perhaps permanently.

These were among the findings of a groundbreaking study, done in June, by the Consumer Reports National Research Center. We wanted to determine, first of all, whether consumers have rebounded from the recession. The answer is yes. Our nationally representative study of 1,006 Americans shows that people are now in the market for homes, cars, and appliances—and that they plan to shell out even more money in the coming year.

The vacations, home renovations, even divorces that seemed out of reach during the recession are now on the front burner; seven out of 10 people told Consumer Reports that they finally feel flush enough to make purchases and decisions they've put on hold for as long as five years. Younger Americans—those 18 to 34—are particularly anxious to start spending: One in four told Consumer Reports they're ready to buy a home, and one-third believe they can buy a car. And the shopping has already begun: Six in 10 people told Consumer Reports that in the past year they'd dropped big bucks on a major purchase—everything from cars and condos to refrigerators and TVs.

But just as the Great Depression scarred an older generation of Americans, so too has this country's most recent economic contraction left behind a more cautious nation. Carl Van Horn, who is distinguished professor of public policy at Rutgers University and director of the John J. Heldrich Center for Workforce Development, and author of the book "Working Scared (or Not at All)," says that almost 75 percent of Americans either lost a job or had a relative or close friend who did in the last few years. "People have just been traumatized," he says. "They're still struggling, worried, and anxious. Even though they're working, they don't believe their jobs are stable, they fear layoffs, and there's a sense of impermanence."

What's the last thing you'd cut back on to save money? Take our quick poll and let us know.

That mingling of hope and caution can be found in consumers like Terry Manies, 47, of Lawrence, Kan. In 2009 Manies lost her $58,000-a-year job as grants director for Baker University. She took a temporary post, and a $5,000 pay cut, at the University of Kansas, followed by another lower-salaried job so far away that she was able to return home only on weekends.

Today Manies is working closer to home, in a retirement community, and actually earning a bit more than she did at Baker. She's spending again—and has stepped up her charitable donations as a result of her experience—but she's always looking over her shoulder. Still, for her and her husband, she feels the economy is turning. "But this notion of getting ahead, I don't think that exists anymore," she says.

In fact, pockets of woe remain. The majority of people—almost eight in 10—told us there were still certain things they couldn't afford: For more than a third of people, the out-of reach dream was a new home; for others it was a pricey vacation or a flat-screen TV. But despite lingering worry, the national mood overall is upbeat. "Consumers are talking more positively about their personal financial situation now than at any time since the recession began," says Richard Curtin, director of the Thomson Reuters/University of Michigan Surveys of Consumers, which has been monitoring public sentiment for 60 years. The reasons? "Greater jobs availability, rising home prices, and a booming Wall Street, whether people own stocks outright or through their pension plans."

For a closer look at the new American shopper, and how things have changed, read on. (And be sure to read "How Shoppers Spend Today" to see what consumers have to say about their spending habits.)

The purchases that define American consumers more than any other? Our cars and our homes. Car sales are skyrocketing today: 46 percent of people we surveyed bought a new or used vehicle in the past year or intend to buy one in the coming year.

Necessity is driving some sales. The average vehicle on the road is 11.4 years old, according to industry analyst IHS Automotive. (In cushier 2007 the typical car was 9.9 years old.) Sales bottomed out in 2009, but now that the economy is in recovery mode, "people are focusing once again on trading in or trading up to a new vehicle," says Steven Szakaly, chief economist for the National Automobile Dealers Association.

Real estate is picking up, too. The dire images of the recent past—block after suburban block plastered with For Sale signs; people paying on mortgages worth more than the homes themselves—are fading. Twelve percent of survey respondents said they'd bought a residence in the past year or plan to do so in the year ahead.

That sunnier outlook also shows up in a study done in June by Thomson Reuters/University of Michigan: Half of all homeowners said that for the first time in eight years, prices had improved to the point that the idea of selling their home was attractive.

No surprise, then, that in 2013 existing home sales finally topped the 5 million mark, the first time since the downturn that sales reached levels set in 2007. Despite a slight dip in sales in 2014 because of higher interest rates, the National Association of Realtors' chief economist, Lawrence Yun, expects a big rebound in 2015 (to 5.29 million). Also, foreclosures and serious mortgage delinquencies are roughly half of what they were in 2008 to 2009. Existing homes are getting a makeover, too: One-third of those we surveyed said they recently completed or are ready to do a major home-remodeling project.

Jennifer Lee, senior economist, BMO Capital Markets: "It certainly helps that overall job growth has been improving. At the end of the day, steady income speaks volumes for consumer confidence; [so does] having your home worth something now, compared to five years ago." Consumer Reports' findings that people are spending their tax refund money on living expenses, "is telling about how cautious consumers have become. There's still a sense of hesitation. People are still remembering the past several years."

Barney Frank, former U.S.representative from Massachusetts and chair of the House Committee on Financial Services: "Yes, consumers are back—some [consumers]. Income disparity is still a problem; lower-end economic activity has not come back as much as upper end. [One reason for optimism is that] the Fed has kept interest rates low. It was one thing to keep them low when things were tough, but they've kept them low as things have started to improve."

Stephen Moore, chief economist, the Heritage Foundation: "People's thoughts about the economy can radically change in a matter of days and weeks. Consumer sentiment rises and falls like a roller coaster. It may be that we're turning the corner. The economy has been stagnant for so long—we've been skinflints for so long—that people are sticking a toe back in the water. That would be a welcome development."

Once we moved beyond the biggest-ticket items, we found that Americans are spending their money very pragmatically. Almost half of respondents told us that during the past few years they've been spending more on groceries; one-third are spending more on wellness products such as vitamins and moisturizers.

Consumers are also stretching their dollars by focusing on items the entire family can use, says Susan Viamari of global market research firm IRI. For example, she says, a household will buy a single bottle of shampoo that appeals to everyone rather than individual products for dry or colored hair. They're also watering down those products to wring out every last drop of soap or cleanser.

Additionally, we've adopted other more frugal habits. People are going longer than they used to between haircuts (41 percent), taking "staycations" rather than big trips (43 percent), and packing a brown-bag lunch instead of eating out (48 percent). The biggest cutback? Fifty-seven percent of women we surveyed said they are painting their own nails rather than going to the salon.

There was a time when many consumers would blow their tax return on a cruise or other goodies. No longer: Of the Consumer Reports respondents who got a tax refund, more than half used the cash to cover everyday expenses such as food and energy bills, for rent or their mortgage, or to pay off debt.

The new practicality has even permeated Americans' fantasies of sudden wealth. Asked what they would do if they won a $100,000 lottery prize, half of those asked told Consumer Reports they'd use it to buy a new home or renovate an existing one.

But if we're getting more realistic, we're also giving ourselves more room for love. During 2013 American women gave birth to 3.94 million babies—a number that's down 10 percent since the record-setting year of 2007. Now, it seems we're ready to start procreating again. Twelve percent of survey respondents said they can finally afford to have children because their personal situation has improved. Twelve percent also said they were ready to marry—while 5 percent said they could now afford a divorce.

"People become more cautious and conservative, psychologically, when they sense they can lose a job at any point," says W. Bradford Wilcox, University of Virginia associate sociology professor and director of the National Marriage Project. Men, in particular, he says, perceive themselves as less worthy marriage material if they're not steadily employed and earning a good wage. "Decision making," he says, "is very much tied to the ebb and flow of the economy."

No matter how good we get at pinching pennies, there are still some things Americans hate to give up. Our caffeine habit, for instance.

"People aren't trading down; they're trading off," says IRI's Viamari. "There's been a huge surge in gourmet bagged coffee sales."

Our survey found that Americans hold tightest to at-home entertainment: When asked, "What is the last thing you would cut back on in order to economize?" 38 percent of people said they'd never ditch pay television, including premium cable, satellite, and streaming services like Netflix and Hulu.

So there you have the American shopper in 2014: overwhelmingly cautious but also optimistic enough to take the plunge on purchases big and small. "We've had four or five years of people being skittish about the economy," says Stephen Moore, chief economist at the Heritage Foundation. His take on Consumer Reports' finding that consumers have a sense that they can spend again: "It's encouraging, to say the least."

"People love coffee," says Helvia Vega, owner of a coffee shop in New York City's SoHo neighborhood. They love it so much, she says, that her business really wasn't affected by the recession. Her top seller right now: lattes, at $4.50 a pop.

More than one in 10 Americans told Consumer Reports that their Starbucks/Dunkin' Donuts habit would be the last thing they'd cut back on. Coffee's addictive qualities are legendary, but who knew we are even more hooked on pay TV? Almost four out of 10 people said they'd be extremely reluctant to drop pay television, including premium cable, satellite, and streaming services such as Netlix and Hulu.

A Baylor University marketing professor, James A. Roberts, says it's a case of things that started out as indulgences having morphed into necessities. Pam Danziger, president of Unity Marketing, a consulting firm, sees them as part of some- thing called the lipstick effect. "When women can't afford expensive shoes or a handbag, they still feel they can treat themselves by splurging on a tube of lipstick that costs $5 or even $25," Danziger says. "They feel entitled to those little treats and rewards, and hold on to them dearly."

A Cornell University marketing professor, Brian Wansink, has a different take. "Whether I'm springing $4 a day for coffee or $1.33 a day for pay TV, it's really not much to justify," Wansink says. "It's a small enough amount that doesn't add up in our internal calculus. I can say ‘I deserve it,' and nobody is going to complain that I'm overindulging as they might if I go out to the movies or a fancy restaurant."

She went from pricey vacations to giving homemade gifts. How the recession changed one woman's spending habits.

In March 2009, Rosette Montes-Hempler was laid off from her position as a website manager at Fujitsu. Montes-Hempler, who had started with Fujitsu in San Jose, Calif., but had telecommuted for years from her home in Las Vegas, was in shock. She and her husband, Tom, had built their dream house on a half-acre of property. The couple had a mortgage, and their children were involved in pricey sports and extracurriculars. "We were worried we might lose the house," she says.

Within six months, Montes-Hempler was re-employed, although with a $25,000 pay cut. Even though her husband was earning about $150,000 a year, the couple feared that neither job was secure. They decided to re-orient their entire family's spending habits. For starters, they no longer took their yearly vacations together to the Cayman Islands or Mexico. Instead, they road-tripped to visit family in California. The pricey birthday and Christmas gifts Montes-Hempler used to lavish on her family—IPads and even appliances—now became homemade blankets and photo albums. "Our family used to compete to see who could give the most expensive presents," she says. "Now it became about giving meaningful thoughtful gifts."

Today, Montes-Hempler believes the economy is changing for the better and is planning their first family holiday abroad since before 2009. But she doesn't plan on doing much else.

"I learned some hard lessons in the past few years," Montes-Hempler says. "Lessons I will keep for a long time."

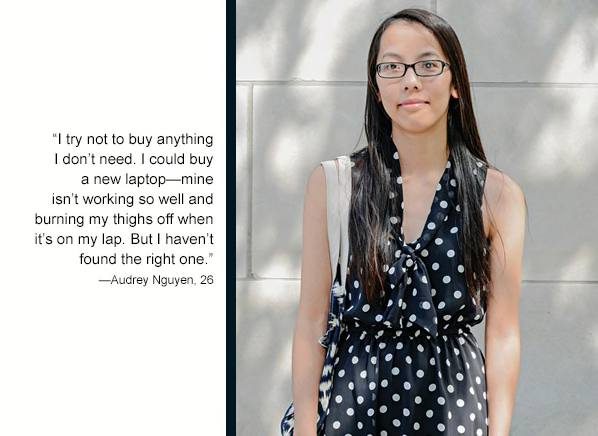

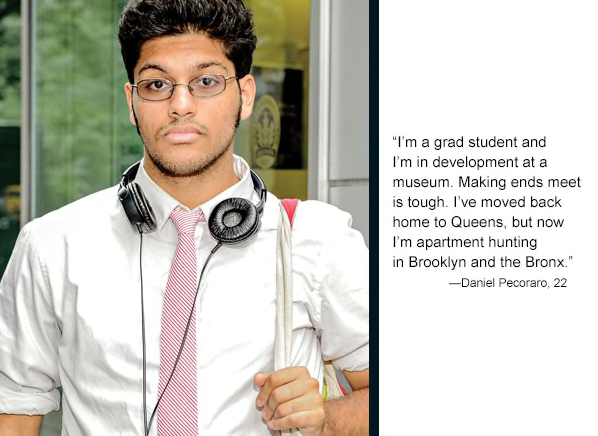

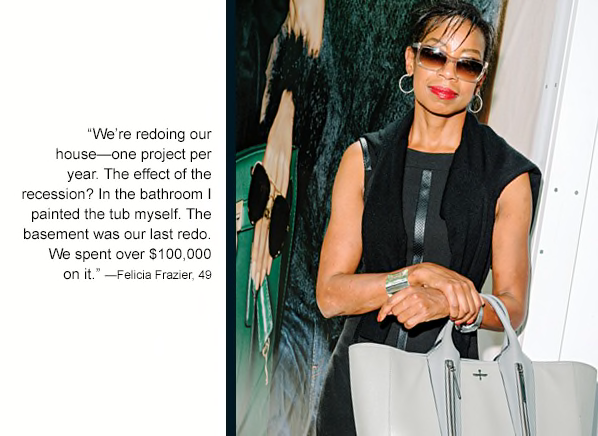

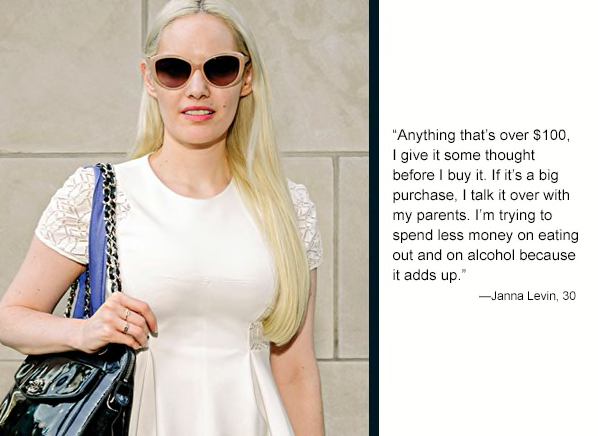

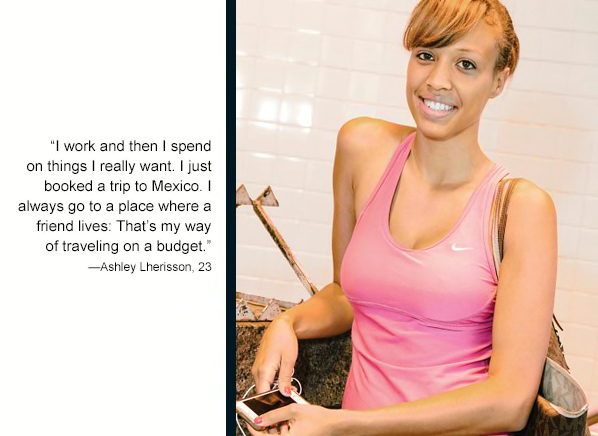

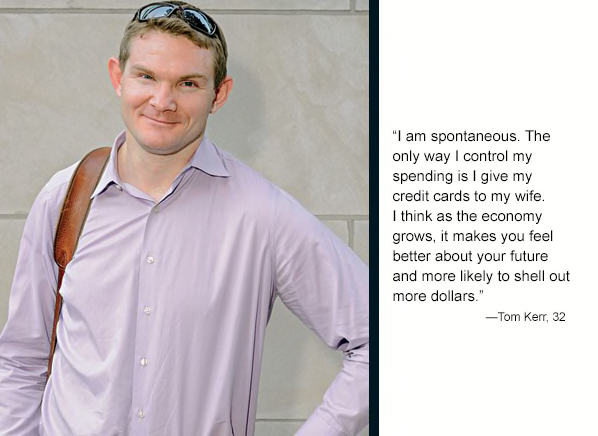

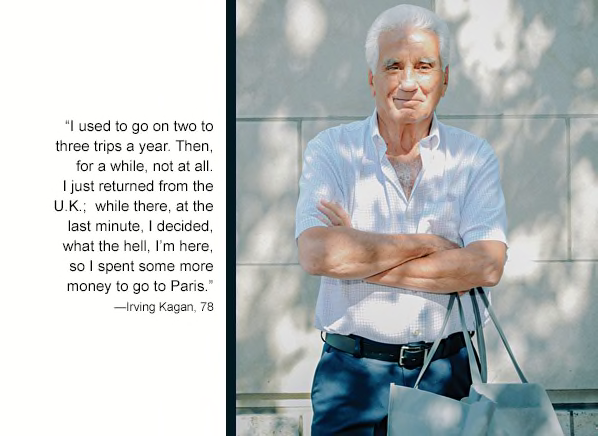

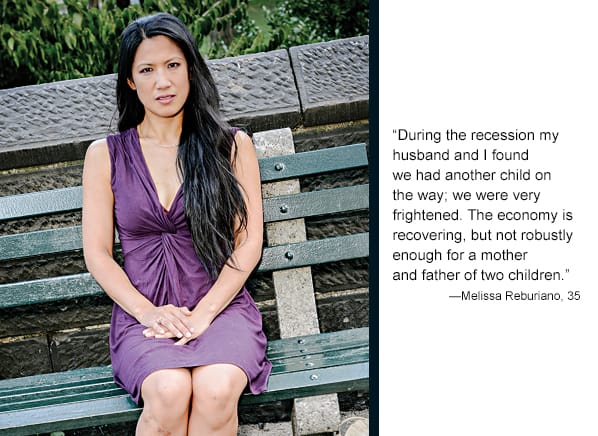

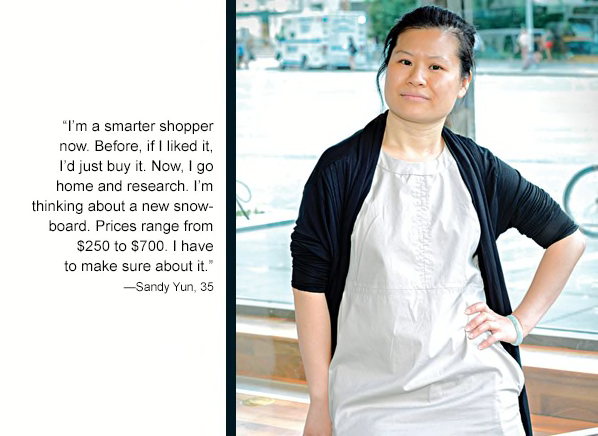

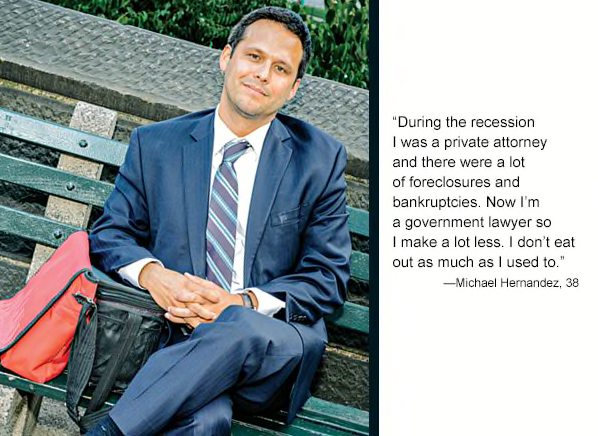

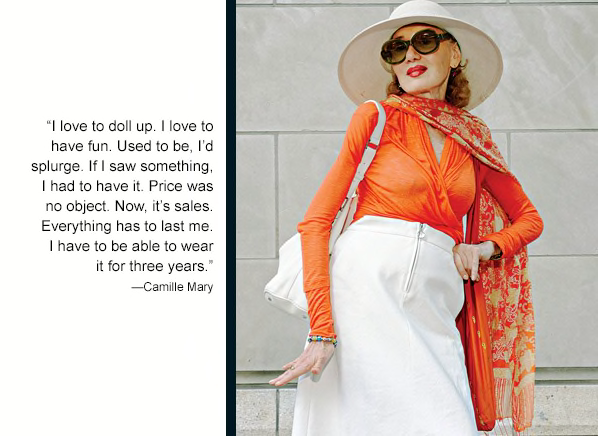

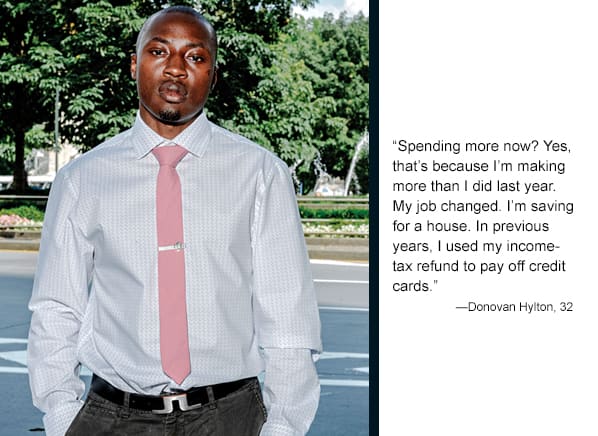

Below you'll find details from other consumers on how they spend.

This article also appeared in the November 2014 issue of Consumer Reports magazine.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop