Sign In

Did you recently get a notice saying that your insurance company is canceling your policy because it doesn't meet the new health law's higher standards? Thousands of people are, and many are angry about it. But before you rush to judgement, it might not be as bad as it seems.

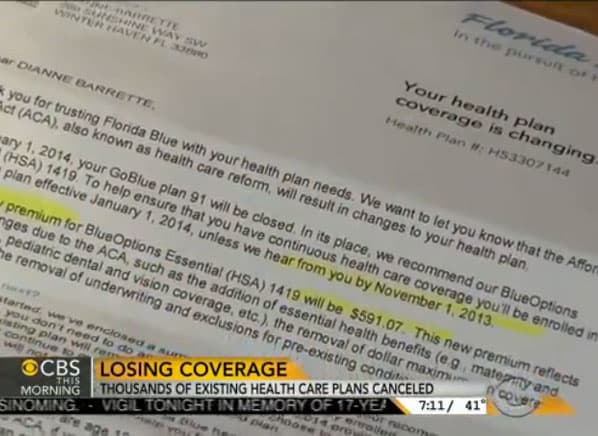

Conisder the case of Diane Barrette, a 56-year-old woman from Winter Haven, Fla. Her story was featured in this CBS News report and endlessly echoed on the Internet. She was upset because Blue Cross Blue Shield of Florida was canceling her $54-a-month "GoBlue plan 91" and offering to replace it with a $591-a-month "Blue Options Essential plan."

Sounds terrible—except that Barrette's expiring policy is a textbook example of a junk plan that isn't real health insurance at all. If she had ever tried to use it for anything more than an occasional doctor visit or inexpensive prescription, she would have ended up with tens or hundreds of thousands of dollars of medical debt.

Here are some of the gory details. (You can see the rest for yourself on this complete plan summary from the insurance company.)

"She's paying $650 a year to be uninsured," Karen Pollitz, an insurance expert at the nonprofit Kaiser Family Foundation, said. "I have to assume that she never really had to make much of a claim under this policy. She would have lost the house she's sitting in if something serious had happened. I don't know if she knows that."

In fact, had Blue Cross Blue Shield allowed her to keep the plan, she would have been fined for going uninsured in 2014. Limited plans such as these are considered "excepted benefits" that don't fulfill the new obligation to have health coverage.

Okay, but can't we be outraged that Ms. Barrette will have to fork over $591 a month for a replacement plan? Actually, no, because she has other and better options than the costly plan Blue Cross Blue Shield wants to put her in. She get real insurance that covers all essential health benefits for well under $200 a month.

She has said her income is about $30,000 a year. It would be nice to look up her choices on HealthCare.gov, which is running the marketplace in Florida. But you can't do that without actually applying for coverage.

So, using tools available through eHealthinsurance.com (I'll walk you through this useful resource tomorrow), I determined that she qualifies for a premium subsidy of $320 a month. She can use that to purchase a Humana Direct Silver 4600/6300 plan for $165 a month.

Like all plans sold in the state Health Insurance Marketplaces, it covers essential health benefits such as doctor visits, inpatient and outpatient treatments, diagnostic and screening tests, maternity care, mental health care, prescription drugs, home health care, and rehabilitation services.

It's not the most generous plan in the world. The deductible is $4,600 and the only things the plan pays for outside the deductible are preventive services, the first $500 of diagnostic lab tests and x-rays in the year, and "diagnostic" office visits, meaning going to the doctor because you're feeling awful and need to know what's wrong. Visits for treatment are subject to the deductible. There's a separate $1,500 deductible for prescription drugs, after which there's a copay of $10 for generics and $50 for brand-name drugs. Once you've run up $6,300 in out-of-pocket expenses, the plan picks up 100 percent of your costs for the rest of the year.

To put these two plans in perspective, let's imagine that Ms. Barrette's luck runs out and she receives a diagnosis of breast cancer that will cost $120,000 to treat.

Under her current junk plan, she would probably receive no more than a few hundred dollars of benefits for doctor visits and drugs. It wouldn't cover her surgery, her chemotherapy, her many expensive medications, or the repeated diagnostic tests she'd likely require. She would end up with probably $119,000 of unpaid medical bills. With the Humana plan, those bills top out at $6,300 a year, no matter what.

Got a question for our health insurance expert? Ask it here. It helps if you include the state you live in.

—Nancy Metcalf

Health reform countdown: We are doing an article a day on the new health care law until Jan. 1, 2014, when it takes full effect. (Read the previous posts in the series.) To get health insurance advice tailored to your situation, use our Health Law Helper.

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop