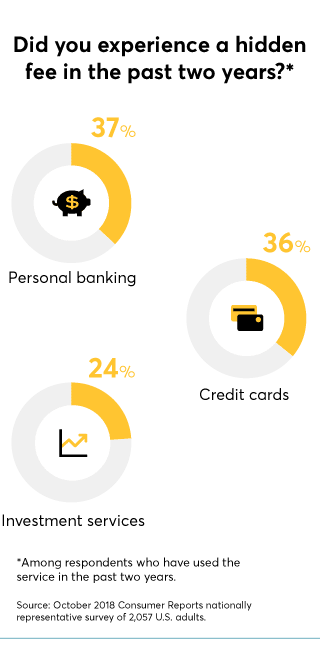

Many banks market their accounts as "free" but fail to mention all the fees—for out-of-network ATMs, overdrafts, monthly service charges, even paper statements—that can add up.

And many of these fees are rising. In 2018, average ATM fees hit a record high for the 14th year in a row, up 36 percent compared with 2008, according to account comparison website Bankrate. And the average overdraft fee is close to the highest it has ever been. The good news is that there are ways to avoid paying some common fees.

"Consumers need to pay close attention when signing up for bank accounts," says Anna Laitin, director of financial policy at Consumer Reports. "A free account can, in fact, be expensive once you take into account the fees you may incur."

As add-on fees become more prevalent across the marketplace, consumers are having a harder time finding the best deal to fit their needs, whether they're shopping for hotel rooms, airplane tickets, cable TV, or a bank account, Laitin says.

"This can be particularly tricky when shopping for bank accounts, where different banks may have very different fee structures," she says.

The good news is that there are ways to avoid having to pay bank fees, says Greg McBride, chief financial analyst at Bankrate.

Here are some common fees that you could be charged and ways to get around them.

Monthly Service Fee

Some banks charge a monthly service fee when your checking account balance falls below a certain threshold. The fee, according to Bankrate, averages $14.35 for interest-bearing accounts and $5.57 for non-interest accounts.

The fix: Open an account with a bank that doesn't have a minimum balance requirement. You're more likely to find truly free checking at a credit union or at primarily online banks such as Ally Bank, Discover Bank, and USAA Bank, according to Bankrate. Another option: Ask your bank whether it will waive the monthly service fee if you have your paycheck directly deposited into your account each pay period. Many banks will do so.

ATM Fees

Failing to use your own bank for cash withdrawals can get expensive. The cost of using an out-of-network ATM has gone up 4.7 percent, on average, every year over the past 20 years. Today, out-of-network ATM fees average $4.68.

The fix: If you're away from home, use your bank's app to find the closest in-network ATM, says Jason Reposa, co-founder and CEO of MyBankTracker, a bank comparison website. Or switch to a bank that covers ATM charges; about a third of the banks surveyed by Bankrate do. Finally, keep in mind that there are other ways to quickly access money from your account. For instance, you can ask for cash back at a store when making a purchase with your debit card.

Overdraft Protection Fee

Banks charge an overdraft fee when you either take a withdrawal or make a payment for more than your account balance. That can be useful if you've set up automated bill payments. But if you go into overdraft, banks charge a hefty fee—on average, about $33, according to Bankrate.

The fix: Set up alerts so that you're notified when your balance falls below, say, $100. And link accounts so that money can automatically transfer from savings to checking. If you're hit with an overdraft fee, you may be able to have the charge removed by calling your bank and asking for a refund. Unless you regularly rack up overdraft fees, there's a good chance your bank will reimburse you.

Or just opt out of the service. But remember: In that case, your bank will decline a purchase or withdrawal larger than your balance.

Wire Transfer Fee

If you need to send or receive money from one bank to another, you may need to use a wire transfer, which can be expensive. The average fee is $13 for incoming wire transfers, $25 for outgoing domestic, and $45 for outgoing international, according to NerdWallet.

The fix: If you don't need the money to clear immediately, consider transferring funds using an ACH (Automated Clearinghouse) transfer instead. Some banks offer it free, and others charge a small fee. Be aware that ACH transfers can take two or three days to process; a wire transfer takes just a few hours. If you need to transfer money to a family member, you could use a payment app such as Apple Pay or Venmo, but there are limits on how much you can transfer at one time.

Foreign Transaction Fee

Even if your bank doesn't charge out-of-network ATM fees in the U.S., you might get hit with charges for using an ATM or debit card when you're abroad. Foreign transaction fees range from 1 to 3 percent of the transaction, according to NerdWallet, a comparison site.

The fix: If you travel frequently, consider switching to a bank, such as Capital One 360, that doesn't charge foreign transaction fees. You might also consider using a credit card that doesn't charge foreign transaction fees, says Arielle O'Shea, a banking and investment specialist with NerdWallet. Among them are cards from Barclaycard, Capital One, and Discover.

What the Fee?!

Are you tired of the endless stream of add-on charges that appear on your bills? On the TV show "Consumer 101," Consumer Reports' expert explains to host Jack Rico how to avoid these pesky fees.