Sign In

In late 2008, owners of new homes, mainly in the South, began reporting troubling problems. Drywall made in China, they asserted, was emitting noxious, sulfuric fumes connected with health issues and the corrosion of pipes, wires, and other metal-based interior systems in their homes. By early 2010, the Consumer Product Safety Commission had received nearly 3,000 such complaints.

Homeowners insurance companies responded by denying claims because the drywall fell under an exclusion found in most policies for "faulty, defective, or inadequate" building materials. Insurers even dropped policyholders who filed claims, maintaining that the customers' finances and homes were now subject to additional risks. Attorneys for homeowners have instead sought redress by suing the builders and drywall manufacturers.

The drywall fiasco, now under investigation by the CPSC, highlights an industry trend. Insurers are placing more risk on policyholders by changing policy language, charging more, or interpreting coverage to the detriment of homeowners.

You might not be among the unfortunate drywall victims, but chances are you'll be affected by at least one of the insurance trends we detail below. Those issuers might threaten to leave you with less coverage for your money or boost the cost of the coverage you have. For each trend, we offer steps to help you mitigate the pain.

In 2009, premiums for renters and homeowners insurance rose by 3.2 percent overall, according to the Bureau of Labor Statistic's Consumer Price Index. In many coastal areas, however, increases have been higher in recent years. The National Association of Insurance Commissioners says rates in Louisiana rose an average of 11.4 percent from 2006 to 2007, the most recent period for which data are available. In Massachusetts, they were up 10.6 percent over the same time period.

Shop for better options. In moving to a new company, you might lose the "loyal customer" discount that can be 10 percent or so of the premium. But if that base premium is relatively high, you may still save money by making a switch. Be sure to compare terms as well as price. A lower-priced policy that has more exclusions is not necessarily a savings, especially if you need to make a claim.

When Consumer Reports surveyed subscribers in 2008 about their homeowners insurance, we found that among those who switched to a new carrier in the prior four years, more than half paid less for coverage. An independent agent or insurance-shopping Web site may be able to provide quotes from a variety of companies.

If you've been forced into a more-expensive tier of homeowners insurance, it might pay to periodically ask an agent whether your insurer would now be willing to move you to a less-costly tier. The company may have adjusted its criteria for eligible clients, or your circumstances might have changed. Or your agent may have taken on a new company that has criteria that favor you, notes Tim Dodge, director of research and external communications for the Independent Insurance Agents & Brokers of New York.

Price is just one component of a good policy; how well the company responds when you really need it is crucial. Our Homeowners Insurance Ratings, published in the September 2009 issue of Consumer Reports (and available to subscribers), detail the claims experiences of 10,700 Consumer Reports readers with 16 insurance groups. The highest-rated insurers were Amica, USAA, and Chubb.

When shopping, look into the financial ratings of any company you're considering. As we've mentioned before in these pages, the most stringent life insurer financial-strength ratings can be found at TheStreet.com (formerly Weiss Ratings), which also rates property/casualty insurers. Go to www.thestreet.com and click on "Portfolio and Tools." A drop-down menu will take you to the insurance ratings. Type in the full name of the insurer, not just the name of the group that owns it, to find its financial-strength rating. Look for insurers with a rating of A (excellent) or B (good).

In many states, homeowners now have two deductibles: one for their main policy and another for a high-risk peril such as a windstorm or hurricane. Florida requires a hurricane deductible of 2 percent for homes valued at $100,000 or more. Policyholders can opt to go higher, up to 10 percent of the insured value.

This trend goes beyond the Hurricane Belt. In Kansas and Oklahoma, State Farm may now apply a percentage deductible for wind coverage. Where these types of deductibles are optional, insurers may offer customers lower premiums in return for taking a higher deductible. On the flip side, homeowners can choose a lower deductible but pay more for the privilege.

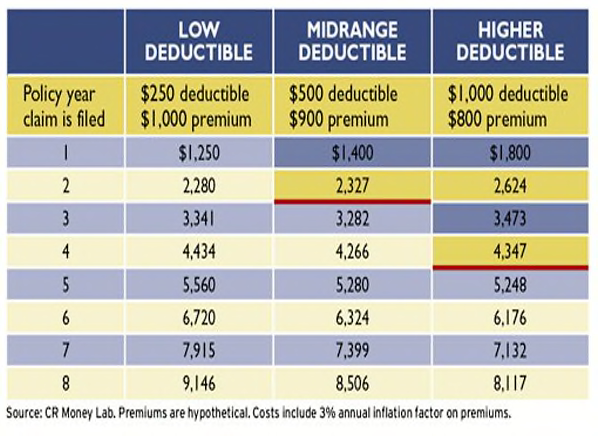

If you must take a percentage deductible, set aside savings toward it in your emergency fund. Switching to a higher flat-dollar deductible can reduce your total costs over time, as the table on the facing page shows. This is especially so if you don't make any claims against your policy in its early years. The average claim is made between years eight and 10 of a homeowners policy, the industry-sponsored Insurance Information Institute says.

Keep in mind that higher deductibles not only save you money but can also protect the rest of your coverage. In another trend, insurers are dropping policyholders if they file frequent claims within a short period. A higher deductible means you'll be self-insuring for smaller claims.

With property values depressed in many regions, homeowners may want to reduce the limits of their homeowners insurance. If their home isn't worth as much, the reasoning goes, why not cut the coverage?

Here's why that's unwise: Homeowners coverage isn't based on your home's market value; it's based in part on the cost to rebuild your home if it were completely destroyed. That figure is related to local building costs. While labor costs in your area may be lower due to less overall demand, costs to rebuild could go the other way if the price of materials rises.

Check your coverage with an agent to make sure you've got the right amount. Your home's replacement cost equals the cost of labor and materials to rebuild, generally excluding the foundation. For a second opinion, an insurance appraiser can give an independent assessment for between $250 and $500.

Your risk of experiencing financial trouble is increasingly central to how an insurer determines your premium. Credit scores are at the core of that judgment, though consumer advocates argue that they don't measure risk of loss. (Consumers Union, the nonprofit publisher of this newsletter, has said that credit-based underwriting in insurance is unfair and should be banned.) Nonetheless, in most states, even customers in good standing—and those with good credit histories—can face much higher premiums based on their "credit-based insurance scores".

Pay your bills on time, and check your credit reports periodically for mistakes and correct any that you find. You can get your free annual reports from the three major credit-reporting bureaus—Equifax, Experian, and TransUnion—by going to www.annualcreditreport.com. Stagger your requests to get one free report every four months. Don't bother with credit-monitoring services, which purport to screen for unauthorized use of your credit cards and other abuses for a cost of more than $150 a year.

A dozen major carriers will sell identity-theft coverage as a stand-alone policy or endorsement (with other extras) to your homeowners policy. Depending on the carrier, the coverage might reimburse you for expenses incurred if your personal information is compromised. Those expenses may include lost wages, notary fees, and legal fees.

Current events are spurring other types of coverage. A new "green" policy endorsement, for instance, pays to rebuild a damaged home with new, environmentally friendly materials.

You'll probably fare just as well monitoring your credit reports and regularly changing passwords, among other ID-theft precautions that cost nothing to implement. ID-theft coverage won't prevent your identity from being stolen, and it won't restore all the money you lose as a victim. Linda Foley, founder of the San Diego-based Identity Theft Resource Center, says a policy that won't cover lost wages related to restoring your good name isn't of great value; neither is a policy with a deductible of $500 or more. Some major credit cards—notably American Express and Visa—offer telephone help from experts in the event your identity is stolen.

Before you opt for a green rider, see if the additional cost of using green materials warrants a pricier insurance policy. Some other extra coverage might be worth buying. For older homes, law-and-ordinance riders pay to rebuild according to new building codes. (Most policies will apply about $10,000 toward that cost.)

National flood insurance is a separate coverage that reimburses you for damage from flooding as well as from clogged drainage systems and mud flows. The average premium is around $558 per year. For information, go to www.floodsmart.gov.

Look into policy discounts. You can save money by bundling auto, home, umbrella, and other property coverage with one carrier, and by notifying the insurer when you install improvements such as a sprinkler system, burglar alarms, or a new roof. In some states, you may be able to reduce your overall premium with special shutters, roof-to-wall "hurricane straps," and other mitigation measures.

One new discount: Farmers Insurance Group recently unveiled a homeowners policy in Texas that gives discounts to such occupations as educators, law-enforcement officers, and physicians.

For nearly 30 years, Consumer Reports readers have consistently rated Amica Mutual Insurance among the top homeowners carriers for claims handling and customer service. But in the last two years, we've received an increasing number of complaints from Amica policyholders that their "credit-based insurance score" made them ineligible for the lowest premiums available. Several told us their credit scores were at or near 800.

Today, more and more insurers are increasingly dependent on credit information to determine a policyholder's risk of filing a claim. "It has greatly enhanced our ability to match pricing to risk," says Peter Drogan, senior assistant vice president of sales and client services at Amica.

Amica executives don't dispute that some clients with good credit scores might experience higher premiums or get less-than-top rates for homeowners and auto insurance. Jim Bussiere, Amica's senior vice president of sales and client services, says the company started using credit in its premium determination about six years ago. Amica is required by the Federal Fair Credit Reporting Act to notify customers of the potential adverse effects of their credit-based insurance scores.

But Bussiere points out that an individual's premium is determined by more than just their credit-based insurance score; it includes other factors such as previous claims, the age of the home, and its proximity to a coastline.

Policyholders who are good risks often save money—or experience less-drastic premium increases—because of their credit-based insurance scores, Amica executives say.

Upping the deductible on your homeowners policy can lower your annual premium and, over time, your total costs, even if you file a claim. This table shows how a low, midrange, and higher deductible affect the total you would pay (in cumulative premiums and deductible) if you filed a claim in any of the first eight years of a typical policy. Red bars show when total costs become less than those for the low-deductible option.

This article appeared in Consumer Reports Money Adviser.

WASHING MACHINE REVIEWS

WASHING MACHINE REVIEWS GENERATOR REVIEWS

GENERATOR REVIEWS

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop