Sign In

People say they're furious at behemoth banks, for myriad reasons: lending practices that helped sink the economy, government bailouts, foreclosures, huge bonuses for CEOs, and now higher fees and tougher account requirements.

Get ready to vent some more. Here's what's industry experts and our own analysis suggest you'll find now and in the coming months:

Banks are trying to make up billions in lost revenue due to the bad economy, new regulations, and in some cases perhaps even their own inefficiencies. But you don't have to be the one to pay the price.

Does it make sense for you to switch banks? We'll show you what to expect and what your options are.

For David Bookbinder, a computer technician from Peabody, Mass., the decision about whether to ditch his megabank was an easy one. When Citizen's Bank imposed tougher requirements in 2010 for customers who wanted to maintain no-fee checking, he transferred his personal and business accounts to East Boston Savings Bank, an institution with a fraction of Citizen's assets.

"I didn't have the time/patience or attention span to waste on watching my accounts so as to avoid the fees," he wrote to The Consumerist, one of Consumer Reports' websites.

It's a common refrain. Bank experts say that institutions are increasingly depending on fees from traditional bank accounts and other lines of business.

Bank of America, which recently dropped plans for a $5 monthly debit-card fee after an uproar, is charging some customers $5 to replace lost debit cards and $20 for rush replacement, which had not been extra. It also charges e-banking customers $8.95 each month they use a teller to make a transaction. In December TD Bank began charging $15 for incoming domestic wire transfers. And in February Chase imposed a $12 fee on its standard checking account, which had been free for most customers.

Some banks even charge fees if you close an account too soon after opening it. U.S. Bank and PNC charge $25 if it's closed within 180 days. Chase had imposed a $25 fee if an account was closed within 90 days but dropped it in December 2011.

You're probably paying more and getting less. Fewer than half of the noninterest checking accounts are now free, down from 76 percent just two years ago, according to a 2011 survey by Bankrate.com.

And the average fee banks charge noncustomers to use their ATMs rose to a new high for the seventh consecutive year, from $2.33 in 2010 to $2.40. Add your own bank's fee for using an out-of-network ATM and the charge climbs to $3.81 on average. The average fee to cover insufficient funds hit a record $30.83, up from $30.47.

Experts predict that banks will continue to experiment with fee increases, tougher account requirements, cost-cutting, and new sources of revenue, such as sharing customers' marketing data.

"Banks are closely examining what costs they can eliminate and where they might be able to charge, and what the market will bear and not drive customers away," says Beth Robertson, director of payments research for Javelin Strategy & Research in California.

It's likely the megabanks will lead the pack, as small institutions wait to see whether they should follow along or court angry customers by offering better deals.

Here's what to expect:

More relationship accounts. Banks will probably dangle more carrots and brandish more sticks to get you to consolidate your accounts at a single institution, which will mean more fees. But you can avoid them by, for example, having direct deposit of your paycheck or linking your savings and investments. Mike Moebs, an economist and CEO of Moebs Services, an economic research firm in Lake Bluff, Ill., says customers with multiple accounts are the most profitable for banks.

Move toward electronic banking. Banks save when you serve yourself, just like gas stations do when you pump your own. So expect them to push computer and mobile-phone banking. That means you might pay more if you use a teller or speak with someone on the telephone. Some banks might present the changes as a perk, not a fee. TD Bank offers customers a $1 discount off their monthly checking maintenance fee if they agree to online statements instead of printed ones.

Higher penalty fees. Do something wrong, such as overdraw your account, and you'll probably pay more. It costs banks just a few cents to handle a debit-card transaction, but when an account is overdrawn and the bank has to figure out what happened, the cost can escalate to $13, Moebs says. Because 87 percent of Americans don't balance their checkbooks, he says, there could be lots of fees.

Big credit-card push. Banks are likely to encourage the use of credit cards, says Bill Hardekopf, CEO of LowCards.com, a consumer resource for credit-card information in Birmingham, Ala. They get a swipe fee when someone uses a credit card, and so far those fees have escaped regulation that has made debit cards less profitable for banks. Moebs predicts that banks will shrink the grace period on credit-card purchases, now around 20 days, and eventually eliminate it. So even customers who pay their bill off every month could be hit with interest charges.

Less-favorable rates. Banks could try to reduce their losses by increasing the interest-rate margin—the spread between what they pay to borrow money and what they charge to lend it. That could mean higher lending rates, especially on credit cards and other unsecured loans, as well as on auto loans.

Higher loan fees. Don't be surprised if you're suddenly charged a fee when you apply for a car loan, Moebs says. And fewer banks might offer to drop origination fees on mortgages.

Charges for premium services. Customers could see new or higher charges for premium services, such as safe-deposit boxes, online budgeting tools, or person-to-person payments, such as Chase's QuickPay service, which allows you to send money to someone else using just an e-mail address or mobile-device number.

Quirky new features. Check your account statement these days and you might notice retailer ads or coupons. With so-called transaction-driven marketing, banks have begun allowing marketing and data-mining companies to sift through customer transactions and tailor offers based on what they find. Fifth Third Bank's Prewards program provides digital coupons that automatically apply a discount when you swipe the bank's debit card at a specified retailer.

Banks are fighting pressure on several fronts. Lending is down, interest rates are at historic lows, and there's been a decline in investment income.

"Fee income really has served to stabilize revenue in light of the volatile interest-rate environment of the past dozens years," says Greg McBride, Bankrate.com's senior financial analyst.

Big banks are also struggling with out-of-control costs, Moebs notes.

He says banks with assets of around $50 billion or more have exceeded their optimal efficiency level, which he places between $500 million and $5 billion.

"The big banks have gotten themselves in the mess that they're in, and it's a cost mess," he says. "And that is something the average consumer and government officials don't see. They're always saying bigger is better. Bigger is not better."

Taking all expenses into account, including salaries, buildings, and equipment, Moebs estimates that it costs a megabank $350 to $450 to maintain a checking account annually, compared with $175 to $240 for community banks and credit unions.

That "translates to higher fees, higher balance requirements, higher loan rates and lower deposits rates," he says. That's why, he says, overdraft fees for big banks average $35, compared with $28 for small banks and $25 for credit unions.

Scott Talbott, senior vice president of governmental affairs for the Financial Services Roundtable, an industry group, says it's hard to compare institutions of such different sizes. "Banks compete with each other on a daily basis, and those competitive forces result in a wide-variety of products and services being offered to the consumer," he says.

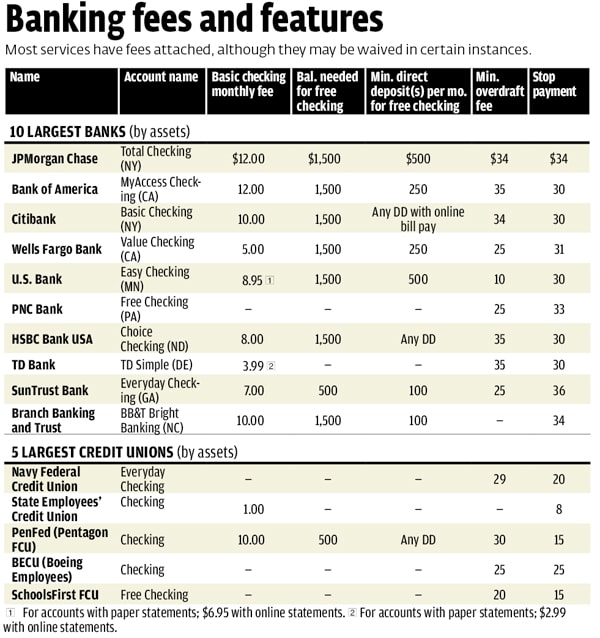

Analysis performed for Consumer Reports by Informa Research Services, a market-research firm in Calabasas, Calif., found other differences among the more than 1,000 financial institutions it tracks. For example, among those that charge a monthly fee for noninterest checking, the average was $10.27 at the largest 10 banks, compared with $7.45 at banks with less than $4 billion in assets and $6 at the 10 biggest credit unions. The fee was higher ($6.91) at credit unions that had assets below $4 billion than at the largest ones.

An Informa study published in The American Banker in July found that interest rates at community banks were lower than national averages for credit cards, home-equity loans, and lines of credit. But they were higher for five-year auto loans.

Bank of America's debit-card-fee attempt caused particular outrage because customers didn't like the idea of having to pay to get their own money, Hardekopf of LowCards.com says. "There's no charge for writing a check, so why should there be a fee for me to access my own money to buy that tank of gas?" he asked.

David Darnell, co-chief operating officer of Bank of America, says it recognized customers's concerns regarding the debit-card fee. "As a result, we are not currently charging the fee and will not be moving forward with any additional plans to do so," he says.

But a study by the Research Intelligence Group, a market-research company in Fort Washington, Pa., found that customers don't easily forgive. Almost a third of the respondents said they would leave their bank if it charged for debit-card payments, and two in five would harbor ill feelings even if the bank reversed the fees.

Matt McFarland, an attorney from Nashville, Tenn., abandoned Regions Bank last fall for a smaller bank when Regions imposed a monthly $4 charge on debit-card transactions. The bank reversed its decision and refunded charges to customers, but he isn't eager to go back. "They said everyone is going to do this, which turned out to be wrong," he says. "They were trying to put it off on Congress."

At a time when banks are relying more on fee income, federal regulations have indeed clamped down on fees in several areas. The regulations are intended to stop what consumer groups and government officials saw as banking-industry abuses.

The latest rule, which took effect in October, limits the so-called "interchange" fees that large banks—those with more than $10 billion in assets—can charge retailers when people swipe their debit cards to pay for a purchase.

They're now capped at 21 cents to 24 cents per transaction, about half the average amount banks had been charging. (The actual cost of processing a debit transaction requiring a PIN is 8 cents on average, and one requiring a signature is 13 cents.) That change alone is expected to cost banks $6.6 billion a year, Javelin says.

It follows other rules that took effect in 2010. One limits the ability of credit-card issuers to raise interest rates on cardholder balances. The Boston Consulting Group estimates that new regulations will cost banks about $18 billion a year. Another provision bars them from charging overdraft fees in connection with ATM and debit-card transactions unless customers opt for overdraft protection. Javelin estimates that will cost banks $5.6 billion a year.

It's not surprising that banks are reacting by raising fees in areas not regulated, says McBride of Bankrate.com. "If the government came along and said you can only charge so much for a hamburger, you'd charge more for soda and fries," he notes.

John Hall, a spokesman for the American Bankers Association, says that as with any business model, when you reduce income, banks are going to rethink their strategies.

Others question bank tactics. Jean Ann Fox, director of financial services for the Consumer Federation of America, says, "All kinds of adverse financial changes have struck banks, and it appears that they are turning to their captive customers to make up that revenue, knowing how difficult it is to switch accounts."

Suze Orman, personal finance expert and TV host, says everyone should size up their bank and check out the fees they're paying, but many won't. "People barely open up their statements because they don't want to see the money they don't have," she says. "You're now asking people to open a statement and try to find the fees they're being charged."

There's a lot of business at stake. Moebs estimates there are 132 million people who have checking accounts with banks and credit unions. The Credit Union National Association says its members have 45 million checking accounts. But the association noted in a 2009 report that its members are much smaller in asset size than the biggest banks. (About 650,000 accounts were added in the four weeks following Bank of America's announcement of its since-rescinded debit-card fee, CUNA says.)

Credit unions were originally organized to serve small groups of customers from a workplace or community. Gradually, regulations have been loosened. In 1998, for example, Congress allowed credit unions to offer membership to people in well-defined geographic areas.

Specialized credit unions have been able to offer services on a wider scale. For example, the Pentagon Federal Credit Union, at www.penfed.org, was set up to offer services to members of the military and their families. Now, you can join for $20 even if you don't have military connections.

Many credit unions have expanded services to match what you'll find at a bank. Since they're nonprofit institutions that exist solely for the benefit of their customers, fees tend to be lower. Larger credit unions have consistently lower fees than smaller ones, according to Informa data.

While some credit unions might not have as many branches and ATMs, a number belong to cooperative networks. You can search for credit unions that might be a good fit for you at the CUNA website locator, at www.creditunion.coop.

Sorting through the terms and conditions in banking agreements can make it hard for consumers to comparison shop. There's an effort under way to make it easier. Sens. Dick Durbin (D-Ill.) and Jack Reed (D-R.I.) have asked banks to adopt a one-page, easy-to-read disclosure form developed by the Pew Charitable Trust, a nonprofit policy group.

They've also asked the Consumer Financial Protection Bureau to require financial institutions to post a concise, consumer-friendly disclosure form on their websites. Consumers Union, the advocacy arm of Consumer Reports, supports this move as a way for customers to shop for the best deals in banking.

If your bank plans to stick you with new fees or tougher account requirements, your first thought might be to find a new one. That might be your best option, but switching banks can be a hassle. So it's important to weigh your options before making a decision to move.

Check the terms. If you're facing a single new fee, see what it would take to avoid it. Increasing your account balance by a few hundred dollars or signing up for direct deposit might work.

Change your habits. For example, plan a weekly visit to an ATM in your bank's network to withdraw cash instead of going out of network. And check your statements more carefully so you don't rack up overdraft fees.

Try to negotiate. You might be able to get a fee waived if you tell your bank you're thinking about moving your accounts.

Consider convenience. Banking is about much more than rates and fees. It's also about the day-to-day banking experience. Does the bank have adequate ATM locations and local branches with convenient hours, or give you privileges to use out-of-network ATMs?

Do your homework. Check with competing banks and credit unions, starting with their websites. That's where you'll find complete information about rates, fees, terms, and conditions.

Plan your getaway. If you've decided that moving your money is the best solution, make the process as smooth as possible. Check to see whether your new bank offers a "switch kit" to help you streamline the process. Or you can download a PDF of our step-by-step guide.

Make your move. Open up the account in your new bank or credit union with a small deposit. Then you can transfer funds from your old bank to the new institution electronically. Arrange to switch over your automatic payments and deposits to the new account.

The grand finale. Leave at least a small amount of cash in your old account and close it once you're sure all checks and transfers have cleared.

WASHING MACHINE REVIEWS

WASHING MACHINE REVIEWS GENERATOR REVIEWS

GENERATOR REVIEWS

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop