Sign In

A good insurance plan can steer you to the care that helps and away from wasting your time and money on unnecessary tests and treatments. For the third year running, we are presenting health plan rankings from the National Committee for Quality Assurance (NCQA), a nonprofit health care accreditation and quality measurement group, of a record 984 plans on their quality of care, customer satisfaction, and commitment to improvement and disclosure of information.

This year, the NCQA ranked 474 private plans (which consumers obtain through a job or purchase on their own), 395 Medicare Advantage plans, and 115 Medicaid HMOs.

Private and Medicaid plans will be a crucial part of the expansion of health insurance coverage that's coming in 2014 with the full implementation of the Affordable Care Act. (See Making Sense of Health Care Reform or download our free guide to health care reform.) The quality data the NCQA collects will become even more important as 25 million Americans gain private insurance coverage and millions more join Medicaid HMOs. (Read more about Medicare and Medicaid.)

Click on the image at right for rankings of health insurance plans nationwide. Use the tool to:

In recent years, the NCQA has detected some improvement in the quality of health maintenance organizations (HMOs) and preferred provider organizations (PPOs). HMOs require patients to get care from providers in the plan network; PPOs allow treatment out of network, for an extra cost. Of the 32 clinical performance measures that the NCQA tracks, private HMOs show clear improvement in 23. Overall, more people receive certain recommended tests, such as colorectal cancer screening and blood sugar tests for people with diabetes.

Consumers say private plans are getting better, too. Seven indicators of consumer satisfaction have improved almost every year since 2007.

But not everything is coming up roses. Measures designed to track overuse show particularly troubling trends. For instance, research shows that imaging tests aren't helpful for most forms of lower-back pain and can even be harmful. But insurance plans have failed to rein in imaging claims for back pain in the seven years the NCQA has tracked it.

For the third straight year, the No. 1 ranked private plan in the nation was the nonprofit Harvard Pilgrim Health Care's HMO in New England, and one of its PPOs finished fifth in the NCQA's rankings. In fact, every one of the top 10 private plans is a nonprofit that doesn't have to satisfy investors with growing profits.

Moreover, five of those plans are integrated health systems, meaning that in addition to providing insurance, they employ the doctors (and in some cases own the hospitals) that care for their customers. Unlike traditional independent "fee for service" doctors and hospitals that make money by doing as many treatments and procedures as possible, whether needed or not, integrated plans prosper by keeping their customers healthy and avoiding wasteful care. They are Capital Health Plan in Florida, Group Health Cooperative of South Central Wisconsin, and Kaiser Foundation Health Plans in Colorado, Northern California, and Southern California.

Kaiser ranks the best of any of the major private insurers, with 75 percent of its private plans in the top 25 percent of rankings. Plans not affiliated with a major national brand come next, with 53 percent in the top quarter, followed by Blue Cross Blue Shield plans, with 41 percent.

Other big brands don't fare as well: Aetna, Humana, and UnitedHealthcare (the second-largest health insurer in America after Blue Cross Blue Shield) all have more private plans in the bottom 100 than in the top 100. Coventry (which Aetna is in the process of buying) has about two-thirds of its plans in the bottom quarter, all of them unaccredited.

Kaiser also did the best of any brand in the Medicare category, with 91 percent of its plans in the top quarter, followed by Aetna, with 59 percent. Humana, the largest purveyor of Medicare HMOs and PPOs, has 35 percent of its plans in the bottom quarter.

A caveat: Plans that don't have NCQA accreditation or have a lot of missing, undisclosed, or less thorough data tend to fall in the rankings. Accreditation, which accounts for up to 15 points of the score, is an exacting process in which insurers must show how they ensure high-quality care, show plans for improvement, and commit to customer service and disclosure. (See Why Accreditation Matters.)

The NCQA has been ranking HMOs for eight years, but this is only the second year for ranking PPOs, which this year make up more than half of private ranked plans reporting. Given that HMOs have had a substantial head start in using NCQA findings to improve their quality, PPOs are catching up. This year, for example, private PPOs perform about the same as private HMOs overall.

In some measures, such as appropriate use of medications for asthma and imaging for lower-back pain, private PPOs are on a par with HMOs. Medicare PPOs actually outperform HMOs on some individual measures, such as managing antidepressant treatments and rheumatoid arthritis medications.

Medicare PPOs are falling behind in the number of customers who give them top scores on satisfaction with the plan. This year, HMOs beat PPOs by 6 percentage points in that area. That might be due to the increasing costs of PPOs. Not only have their premiums been growing, but so has the patient share of in-network costs and the extra costs for going out of network. On the other hand, PPOs perform slightly better than HMOs on getting care quickly, doctor communication, and getting needed care.

Unaccredited plans lose ground in the NCQA rankings because accreditation counts for up to 15 points out of a possible 100. Here's why.

During the accreditation process, evaluations by physicians and managed-care experts make sure not only that the plan has the right policies and procedures but also that the plan is following them. Do the plans provide accurate marketing material? Do they give clear information to members on coverage and denial decisions? Do the providers in their networks have proper credentials?

"It's not enough to have an appeals process," says Andy Reynolds, an NCQA assistant vice president. "The on-site survey looks to see how the plan executes it."

Accredited plans also commit to being held accountable for their performance by reporting data on it. Experience has shown that when plans report on their performance, it usually gets better. In fact, the health care reform law will require that any plan sold through exchanges in 2014 and beyond must be accredited.

A total of 254 ranked plans are not accredited, of which 22 are scheduled for accreditation and two were going through the accreditation process as we went to press. There are a number of reasons a plan might skip NCQA accreditation, including the expense—plans pay a fee to the NCQA for it. Plans might be accredited by another organization, again for a fee. Many more Medicare and Medicaid plans than private plans are not accredited.

All unaccredited ranked plans do submit some quality and consumer satisfaction data, so you can compare both types of plans in your area.

Read more about accreditation and what's behind the NCQA rankings of health insurance plans.

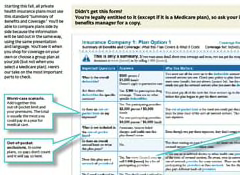

Starting this fall, all private health insurance plans must use a standard Summary of Benefits and Coverage form, similar to the familiar Nutrition Facts label on packaged foods.

You'll be able to compare plans side by side because the information will be laid out in the same way, using the same presentation and language. You'll see it when you shop for coverage on your own or choose a group plan at your job (but not when you select a Medicare plan). If you don't get it, ask your insurer or benefits manager for a copy.

Click on the image above right to download an annotated version of the chart, including our take on the most important parts.

WASHING MACHINE REVIEWS

WASHING MACHINE REVIEWS GENERATOR REVIEWS

GENERATOR REVIEWS

Build & Buy Car Buying Service

Build & Buy Car Buying Service

Save thousands off MSRP with upfront dealer pricing information and a transparent car buying experience.

Get Ratings on the go and compare

Get Ratings on the go and compare

while you shop