Health insurance is one of life's necessities—but it's full of pitfalls for consumers.

It can be difficult to know whether a particular doctor accepts your insurance or is taking new patients. Keeping track of your deductibles, co-payments, and coinsurance can challenge even the most devoted home record-keeper. Determining the cost of a test, procedure, or drug can be daunting. And trying to assess the quality of care from a specific doctor or hospital can be even more overwhelming.

Wouldn't it be great if there was a simple way for consumers to untangle it all?

There is. Many insurance websites now have online tools that allow you to compare healthcare providers in your plan on cost and quality.

Consumer Reports recently looked into these kinds of tools from 11 health insurance companies that do business in New York, plus five stand-alone websites open to all that offer similar services.

Only five of the 40 volunteers we recruited to try the insurer-based tools had ever used one before. And other research suggests that while most people want this kind of information, many don't know where to get it.

But once introduced to those tools, most of our volunteers found that even the lower-scoring ones provided useful information and that the best ones were very helpful.

Here's what you need to know about these tools—and why they're more important than ever right now.

Why We Need Help

Staying on top of your healthcare costs has never been more essential, for three main reasons:

1. Higher deductibles. People insured through their employers have seen their deductibles almost triple in recent years, from $584 a decade ago to $1,478 today.

And New Yorkers who buy a midlevel Affordable Care Act plan through the state's health insurance marketplace now have an average deductible of a whopping $2,000.

These high-deductible plans may make people more aware of cost before seeking healthcare. But for consumers to shop by price, they need to know the real cost of their care, something that's not always easy to find.

2. More restrictive lists of healthcare providers. More plans now have small or limited networks of doctors and hospitals. And most insurers make you pay all or much of your healthcare bill out of your own pocket if you choose a provider off that list.

But knowing who is and isn't in your network can be confusing. And in most of New York, people who buy insurance on their own through the state marketplace don't have access to a single plan that covers nonemergency out-of-network care.

3. Soaring drug costs. Drug sales are expected to rise by double digits in 2016, due in part to costly new drugs coming to market and pharmaceutical companies jacking up the cost of existing meds, such as what happened with EpiPens.

In some cases, Consumer Reports found that you're better off shopping at Costco, Target, or another chain pharmacy than using your health insurance. But you can't make that choice without knowing what a health plan will charge you for a drug.

Why Costs Vary

The prices your health insurer pays to doctors, hospitals, labs, and other providers are the result of some very hard bargaining.

A prestigious academic medical center, for example, might command a higher price for a routine hernia repair or knee replacement than a community hospital. Young doctors just starting to build a practice might agree to lower fees than veteran physicians who already have more than enough patients. If there's only one group of orthopedic surgeons in your area, for example, they can pretty much name their price.

As a consequence, prices for the same service can vary significantly in a given locale. In Rochester, for instance, the estimated cost of a lower-back MRI ranges from $539 to $786, according to analysis by Guroo, a website that provides free information on healthcare costs to consumers.

In Albany, a checkup for a middle-aged patient can cost $276 to $950 depending on the provider and the patient's gender.

And in New York City, the price for a routine childbirth, including prenatal and newborn care, ranges from $13,215 to $19,849.

When it comes to medication, insurers often hire outside companies to do the negotiating for them. Depending on the deals they make, a popular cholesterol drug or antidepressant, for example, might be cheap in one plan but costly in another.

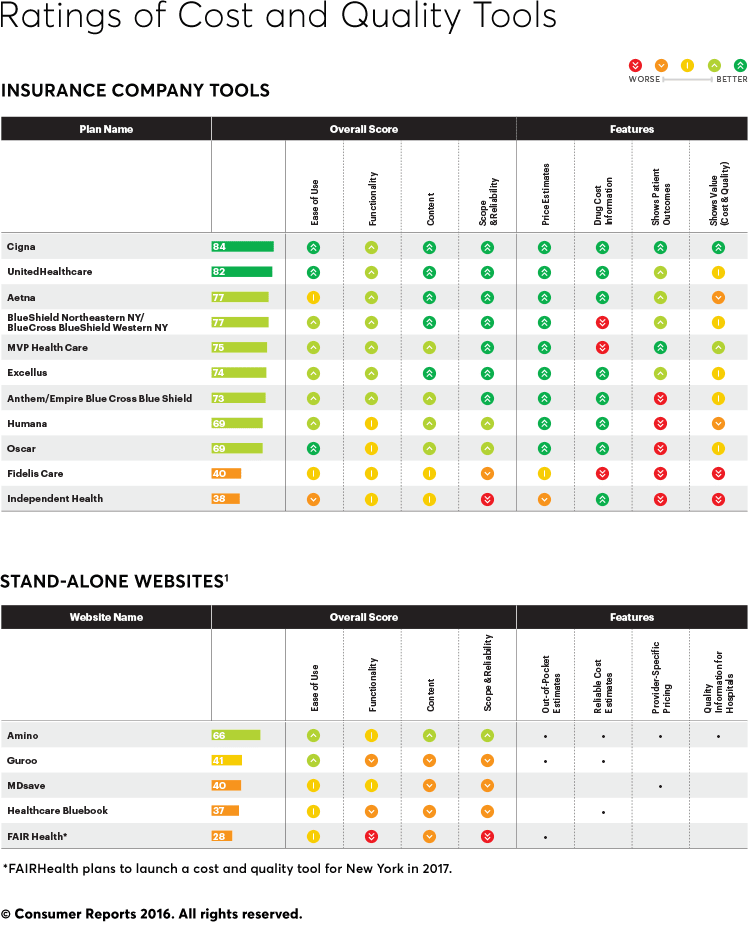

What We Found

To analyze the tools, we interviewed consumers who had the largest health insurance plans sold in New York State that include price calculators.

We asked them what their ideal health plan website would look like, and then had two expert observers look over their shoulders (virtually) as they logged in to websites to search for providers, prices, and other information. We asked another group of volunteers to evaluate stand-alone cost estimators using similar methodology.

Read more about how we conducted our analysis, plus an in-depth look at what we found.

What consumers liked. Like anyone who uses websites, they appreciated the ones that were clearly organized, easy to use, and provided information in nontechnical language.

They most valued being able to look up claims and benefits easily; find hospitals, doctors, and other providers; and find cost information specific to their plan, especially when the site also rated providers on the quality of care.

What consumers disliked. They were frustrated when they had to click through screens or navigate drop-down menus to find or narrow the information they wanted.

They were suspicious of sites with outdated or incomplete information. And they were annoyed when price information was missing or didn't break out what they would have to pay out-of-pocket.

For details, see the ratings below. You can also call your health insurer to ask for specific cost comparisons and information.

6 Steps to Using Cost and Quality Tools

Almost everyone who tested these tools for Consumer Reports said they provided useful information. So it's worth making the most of whichever tool your insurer offers or trying one of the stand-alone websites that provide some of the same services. Here's what you need to know to use them effectively:

1. Set up a username and password. With almost all of the tools, signing in also gives you access to your claims history and price information based on how much of your deductible you've used up. Save your log-in info. Several plans didn't recognize members from one visit to the next.

2. Get familiar with your plan's benefits and rules. Sure, you know your deductible, but do you know whether there's a co-pay (a specific dollar amount) or coinsurance (a percentage of the bill) for a doctor visit, an imaging test, or a hospital stay? Does your plan cover some services, such as primary care visits, before you've met your deductible? Almost all of the plans we reviewed made it easy to find those details.

3. Use the tool to find providers—but verify the information. Every tool included a list of participating doctors, hospitals, labs, and other providers. Some, such as UnitedHealthcare and Blue Cross Blue Shield, had better tools for narrowing your search. We couldn't independently check the accuracy of the provider directories, but other research suggests they're not always up-to-date. So once you've narrowed your choices, call your insurer and the providers to double-check that they will take your specific plan.

#HighDeductible is a hot topic on Twitter. Join in the discussion with other people feeling the pinch of a high-deductible health plan.

4. Comparison shop when you can plan ahead. You can't always shop around for healthcare. After all, you're not going to compare prices in an ambulance after a heart attack. But you can and should shop around for many tests and treatments that are common and can vary widely in price, such as MRIs, lab tests, joint replacements, biopsies, hernia repair, or childbirth. All of the tools we evaluated allow those sort of searches, though they don't always list prices that are specific to a member's personal plan. And note that the tools can sometimes be difficult to find on the websites. So look for the words "cost" and "quality" in the tool's navigation.

5. Check for quality. The best tools present information on the quality of care provided by doctors and hospitals, such as complication rates or patient satisfaction scores, along with cost. That helps you choose providers that offer the best overall value. Cigna, for instance, shows cost and quality side by side. Even if your insurer offers info on quality, check other sources, too, notably Consumer Reports' hospital ratings. And note that higher cost doesn't always mean higher quality.

6. Use stand-alone tools. If your plan doesn't have price information, use a stand-alone website. That can give you a sense of a fair price for the services you're interested in, which you can then compare with prices quoted by your insurer, doctor, or other provider.

New York Heath Insurers That Don't Offer Cost Estimators

If your insurer is listed below, you can still get some of the same information from a stand-alone website that offers similar cost estimates. Check the chart above to see how those stand-alone websites fared.

- Affinity

- Atlantis/Easy Choice

- CDPHP

- EmblemHealth

- The Empire Plan (United)

- Healthfirst

- MetroPlus Health Plan

- North Shore LIJ

- CareConnect (Northwell Health Company)

- Oxford Health (UnitedHealthcare)

How We Test

We evaluated cost and quality tools developed by health insurance companies as well as those offered by stand-alone websites. In each case, the Overall Score is based on four components: Ease of Use, which focuses on user-friendliness; Functionality, including how easy it is to compare providers as well as filter and sort search results; Content, including what type of price, quality, and other information is available; and Scope and Reliability, reflecting the breadth and the reliability of the price and quality data. For details, see our technical report (PDF).

Editor's Note: This article also appeared as an insert in the January 2017 issue of Consumer Reports magazine. For a PDF of that insert, click here.

Support for this work was provided in part by the New York State Health Foundation.