Cash is king, right? But check your pockets. Almost half of us walk around with less than $20, according to a 2014 survey by Bankrate.com. And with so many other ways to pay—a dozen and counting, including mobile wallets and store-branded payment apps, and, of course, old-fashioned credit and debit cards—legal tender today is becoming more minion than monarch.

Bryce Mendelsohn, 36, a San Francisco physician, is cashing out, meaning he has all but abandoned paper money. He usually carries no more than $20 and favors Apple Pay, mobile wallet software that came preloaded on his iPhone 6. It's faster and more secure than cash and doesn't stuff up his pockets. So he actively seeks out retailers that let him pay by holding up his iPhone to the cashier's payment card reader. With one touch of his finger, a transaction is complete.

Mendelsohn uses a different kind of mobile payment platform to pay baby sitters (Venmo) and tutors (PayPal) without physical money. Those are person-to-person, known as P2P, smartphone payment apps that let anyone send money to anyone else in a snap (see "A Field Guide to Mobile Money").

Elizabeth White, who usually carries less than $5 or no paper money at all, is also cashing out. She lives in New York City and loves to collect miles on travel rewards credit cards, onto which she charges "everything," even small purchases such as a pack of gum. For other expenditures, White, 37, now pays with electronic alternatives—Apple Pay for groceries and coffee, the Square Cash app for her hairdresser, the Uber app for car service around town, and a transponder (hers is E-ZPass) for electronic bridge, tunnel, and turnpike tolls.

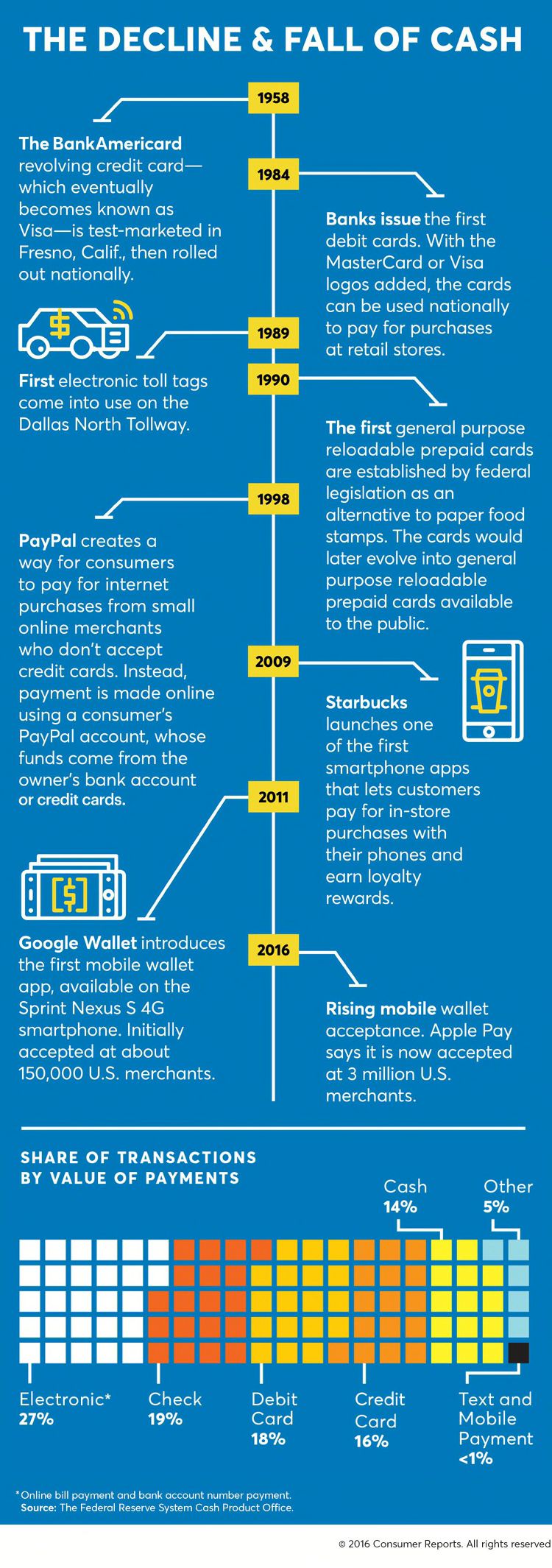

America has been cashing out and on a steady march toward becoming a cashless society since the 1950s, when Diner's Club, American Express, and Bank of America launched the first modern charge and credit cards. Through the '60s, '70s, '80s, and '90s, plastic gradually muscled in on cash as a main way to pay. In many respects, the new mobile payment methods are simply virtual versions of payment cards—because an underlying credit, debit, or prepaid card, or a checking account, is still required to fund the transactions. (See "The Decline & Fall of Cash" infographic below for more details.)

But now that smartphones and other electronic devices are becoming part of the payment process, the way we spend cashlessly is dramatically shifting, presenting new benefits and some potentially negative consequences—from privacy concerns to worries about overspending because it's so quick and easy. And how a lost, broken, or dead-battery phone can disable your ability to pay.

Research shows that all consumers are wading into some mobile payments technology, but younger ones are going all-in sooner; 34 percent of those ages 18 to 29 are now using mobile payments vs. only 16 percent of consumers ages 45 to 59, and 7 percent of those 60 and older, according to a May 2015 Federal Reserve Board survey. "My parents have no interest in Apple Pay," Mendelsohn says. His theory? "My guess is there's something tangible about cash." And they may have concerns about actually using the device.

Now, as retailers scramble to keep up with mobile payment adopters, the rest of us may also decide that it's time to rethink the way we pay for goods and services.

You're probably already helping to make cash obsolete if you're among the 20 million who have access to Walmart Pay or are a driver with one of the 37 million electronic toll transponders. Thirty years ago, 36 percent of consumer purchases (as measured by dollar volume) were paid for with the green stuff, according to the Federal Reserve. By 2012, that number had dropped to just 14 percent.

Other countries have been quicker to change, according to some industry research. In Belgium, France, Canada, the United Kingdom, and Sweden, cashless payments—which still include old-fashioned checks—now comprise 89 to 93 percent of consumer spending. In Sweden the switch had such a negative impact on tithing that houses of worship began installing a sort of digital collection basket, to take offerings via text and credit and debit cards, and through apps. In Denmark last year, lawmakers proposed allowing some retailers to refuse cash entirely.

And in June, Canadians began paying select merchants and friends with MintChip, a digital equivalent of cash developed by the Royal Canadian Mint and acquired by nanoPay, a private tech company. MintChip is an encrypted digital currency, based on the Canadian dollar, which can be loaded onto your smartphone or other device to pay merchants and send money to friends instantaneously. (The government was its original architect to ensure that the system was affordable, private, and secure.)

But Americans are catching up. A MasterCard study of 33 major economies says that the U.S. is at a "tipping point," beyond which near cashlessness is inevitable, because disruptive new digital payment products are expected to change entrenched consumer habits that still favor cash—to settle small-dollar purchases or preserve the anonymity of a transaction.

The infrastructure for accepting cashless payments hasn't always been available at every point of purchase, either. But that's changing. Handheld and mobile technology such as Square has made cashlessness possible for a whole new class of merchants. Food trucks, art shows, street festival vendors, and plumbers can now use their iPhone and Square technology to accept payment cards.

Cash may never go away completely; there's still about $1.5 trillion in U.S. paper and coin circulating the globe. And the physical stuff continues to have a comforting effect on Americans, particularly when natural disaster threatens. "Before a hurricane makes landfall, the Federal Reserve gets on average a 25 percent increase in currency orders from financial institutions in the path of the storm," says Barbara Bennett, vice president of the National Cash Product Office at the Federal Reserve Bank of San Francisco. And paper money is likely to always be required when the tooth fairy calls.

New cashless technologies are in the works that will allow consumers to leave phones and mobile wallets at home. Technology is already allowing consumers to authorize payment with only fingerprint detection. "Eyeprint" readers could be next.

To help you decide whether it's time to abandon cash, here are some pros and cons, in four key areas: convenience, security, privacy, and marketplace fairness.

Convenience

Pros

Consumers value convenience as the most important characteristic of any way to pay, according to research by the Federal Reserve Bank of Boston, and they rate cash, debit cards, and credit cards as highly convenient. But the newer alternatives can involve even fewer hassles than carrying cash.

For example, when you owe money to a friend, P2P payment apps eliminate the chore of writing a check or running to the ATM to make a withdrawal. The P2P app Venmo is so popular that its trademark name is starting to be used as a verb. "If I have dinner with friends, one of us will pay and the others Venmo him their share of the bill," says Owen Clapp, 25, a Los Angeles musician who usually carries less than $10. He says that's simpler than splitting the bill with several payment cards.

Branded apps like the ones from Starbucks and Dunkin' Donuts let you earn discounts and rewards when you use them to make payments, eliminating actual coupons. "The customer response to our mobile apps has been phenomenal. Not only are they using their phone as a wallet, but as a connection point to Starbucks," explained Adam Brotman, general manager of Starbucks Digital Ventures, on the anniversary of the app's rollout.

Soon, digital payments are expected to radically change the way we shop in stores with an app that will allow customers to scan merchandise and pay for it in the aisles, then simply walk out the door with their purchases, says Amitaabh Malhotra, chief marketing officer for OmnyPay, which creates those shopping and payment functions within apps.

Cons

All of those goodies may appear to be free, because consumers pay little to no explicit charges for most cashless transactions. But consumers ultimately pay billions in fees each year when they pay without cash.

The fees are not so transparent because banks charge merchants for each cashless transaction, and merchants ultimately pass on those added costs to consumers in the form of higher prices, says Mallory Duncan, general counsel at the National Retail Federation trade group. "That means everybody is now paying $100 for what would otherwise be a $99 basket of goods. That hurts customers, especially the poor," Duncan says.

Cashless convenience has some other drawbacks. "It definitely encourages you to spend more money too easily," says William Sanchez, 41, a web operations manager at a radio network with $4 in his pocket. He learned that after noticing how T-shirt and raffle-ticket sales skyrocketed once his son's Cub Scout den started using a Square reader during fundraisers. Retailers have seen that, too.

Costco members who have the store's official credit card spend more, on average, than those without it, says Richard Galanti, chief financial officer of the big-box chain. Cashless ways to pay reduce the friction and frustration, which increases the likelihood of spending, concluded researchers Priya Raghubir and Joydeep Srivastava in their 2008 study.

There are additional downsides. Kari Paul, a Brooklyn-based freelance writer, has noticed that "Venmo is turning our friends into petty jerks," because it allows them to pester each other for reimbursement on tabs they used to pick up as a kindness.

Security

Pros

In surveys, consumers say they believe credit and debit cards are in some ways more secure than cash, in part because stolen cash is gone forever but fraudulent card charges can be reversed. Consumers don't seem to have as much faith in mobile payments, rating them as the least secure, says economist Scott Schuh, director of the Consumer Payments Research Center at the Federal Reserve Bank of Boston.

That lack of confidence is a bit misplaced, considering smartphones that make mobile cashless payments possible are drawing from an underlying debit or credit card. That means both mobile and plastic payments are covered by the same small- to zero-loss liability consumers are protected by. Mobile technology secures transactions as well as—or sometimes better than—credit and debit cards alone. Here's an example: Apple Pay stores payment credentials on an encrypted "secure element" chip built into the phone. That substitutes the actual payment account number with an encrypted "token" and creates a one-time-use code for each transaction—that would be useless to a hacker who captured them. To authorize payment, the shopper must enter a PIN or use fingerprint touch ID. So basically, if you lose your credit card, someone can pick it up and use it, but it's more difficult for a crook to use your Apple Pay if you lose your iPhone.

Cons

The digitization of dollars puts them at risk of hackers looking to find and exploit security weaknesses. In 2015, crooks found a way around Apple Pay's state-of-the-art security. They acquired iPhones—probably using stolen identities—and loaded stolen credit card account numbers onto the devices.

Apple wouldn't comment on the record about that security problem, which has since been resolved. But the scam illustrates the relentlessness of hackers. An estimated 112,000 consumer accounts—across all brands of mobile wallets—were taken over last year, according to Javelin Strategy and Research, a California-based consulting firm.

Officials from Javelin warn that as mobile wallets gain popularity, they'll continue to be a target for cybercriminals.

To protect yourself, before setting up your mobile wallet install anti-malware software on your smartphone; anti-malware is not available for iPhone. Use strong, unique passwords with your mobile carrier's online account.

Privacy

Pros

Mobile payment transactions can generate a mountain of digital data, including your Social Security number, internet protocol address, and payment card account numbers. Also collected is your spending information detailing what you bought, where, when, and for how much.

That data is necessary to provide the payment services and process the transactions you want. It's also used to authenticate your identity, and detect and prevent fraud.

The already digitized transaction data can also serve as the necessary raw material for household budgeting and money management software. "What's great about being mostly cashless is the fact that I can automatically import 95 percent of my spending transactions into Mint," says White, the cashless fan, referring to the online budgeting and money management tool.

Customized advertisements and coupons can be another benefit, if you don't mind being targeted in that way.

Cons

Unfortunately, that huge trail of info can tell lots about us that we may not want others to know. Mix that with other information that can be gleaned from a smartphone and mobile payment companies can see you in even greater detail.

Google's Android Pay mobile wallet also captures your search queries and information from third parties, including your credit report. Their privacy policy says they don't share sensitive personal information with companies outside of Google without your opt-in consent. But Google, which did not respond to a request for comment, is itself a publisher of advertising, including targeted ads.

One of the biggest privacy concerns is unanticipated uses of your data, because privacy policies tend to give their authors broad permission for uses that may not even exist yet, says Claire Gartland, consumer protection counsel at the Electronic Privacy Information Center: "It's a take-it-or-leave-it disclaimer that codifies your consent for the company to do anything conceivable with your information."

Marketplace Fairness

Pros

About 34 million low-income consumers have little or no access to traditional banking services and wind up paying the most to use their own money. The U.S. Postal Service inspector general estimates that those consumers spend more than $2,400 per year in interest and fees on high-priced alternative financial services. Because 84 percent of adults earning less than $30,000 per year own a cell phone or a smartphone, the Consumer Financial Protection Bureau and Federal Deposit Insurance Corporation see mobile financial services as a potential money saver for lower-income consumers.

Virtual banks such as Ally Bank and GoBank—which are essentially a smartphone app—can open the door to a variety of more economical banking services. With those accounts, consumers can use P2P services, e-toll tags, and mobile wallets. Android Pay, Apple Pay, and Samsung Pay also support participating prepaid cards—payment cards that are preloaded with funds and can be used like a normal credit card, with no credit check or bank account needed.

Cons

Mobile financial services have some critical drawbacks. The cost of cellular and data services can often be prohibitive, especially for low-income consumers, and wireless service can be spotty.

Security is a major concern. Low-income consumers worry about transacting financial business via smartphone, in part because they don't have the financial cushion necessary to handle even temporary loss of access to their funds due to fraud. Fear over loss or theft of their phone is another concern.

Last, consumer protections vary. "The world of mobile financial services remains complex," says Suzanne Martindale, staff attorney at Consumers Union, the policy and mobilization arm of Consumer Reports. "The potential benefits these services offer may in some cases be undercut by gaps and uneven consumer protections that may leave economically vulnerable consumers at greater risk of fraud or loss."

Editor's Note: This article also appeared in the November 2016 issue of Consumer Reports magazine.