For years, many investors ignored the fees they paid to invest. And it was easy to do because they look so small—often just 1 percent or less of your portfolio.

But today more investors are catching on to the benefits of low fees, with many shifting to less expensive options, such as index funds. More than $450 billion was stashed in index funds last year, according to Morningstar, the fund data firm.

That trend has sparked a price war among major fund companies to reduce investing fees. Among the latest cost-cutting moves, Schwab recently announced that it will eliminate fees for buying and selling stocks, exchange-traded funds (ETFs), and options online. Schwab's price cut was quickly followed by TD Ameritrade and ETrade, which both announced zero-commission stock, ETF, and option trades.

Over the past couple of years Vanguard and Fidelity have also expanded their menus of ETFs that can be traded without commissions, and Fidelity has launched no-fee index funds.

Though all this is good news for investors, they need to be aware that brokerages often levy other fees that aren't always obvious.

The impact of trimming your investing costs might not seem that important, but it could make or break your retirement success, says John Scott, director of the retirement savings project for The Pew Charitable Trusts.

As Pew's free online calculator shows, a 20-something investor who saves in funds that charge low annual fees over 40 years could retire with $300,000 more than someone with the same portfolio who is charged higher fees.

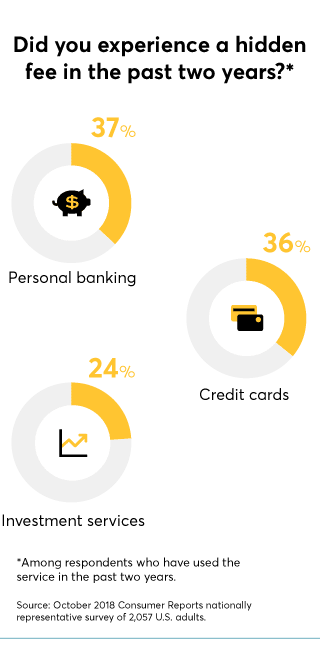

Still, not all investors take advantage of lower costs. A recent Consumer Reports survey found that 4 in 10 investors weren't sure how much they paid in fees. And among those who knew the costs, many said they were unhappy with the amounts being charged.

Here are some fees to watch out for and how to avoid them.

Management Fees

It's wonky-sounding, but your fund's expense ratio is a key number to know. This is the annual fee that's charged by mutual funds and ETFs for investment management and operating expenses, which is calculated as a percentage of assets. This cost is deducted from your investment return.

The average annual expense ratio these days is 0.52 percent, according to Morningstar, which means that someone with $10,000 invested would pay $52. But there's a wide range. Some mutual funds charge 1 percent or more, and very low-cost index funds and ETFs charge just 0.10 percent or less.

You can check to see whether your fund's or ETF's expense ratio is high or low by plugging it into FINRA's free fund analyzer tool.

The fix: Opt for low-cost index funds from such firms as Fidelity, Schwab, or Vanguard that have fees of 0.20 percent or less. Or consider exchange-traded funds, which may charge 0.10 percent or less. If you're saving in a company-sponsored retirement plan, such as a 401(k), look for funds with the lowest expense ratios. (Read more advice on 401(k) fees.) Over the long run, that could boost your nest egg by hundreds of thousands of dollars.

Sales Charges

A generation ago it was common to have to pay a fee, once as high as 8.5 percent, to buy and sell investments. Today it's easy to avoid these commission costs, especially if you work with an online brokerage, because most offer a wide array of no-transaction-fee mutual funds and ETFs.

But if you're working with a broker, be wary—you may still get a recommendation for a so-called A-share mutual fund, which will have the letter A at the end of its name. These funds typically charge an up-front sales load of 2 to 4 percent, and the expense ratio can be 10 times higher than a low-cost index fund, according to Morningstar. If you want help from a financial expert, you have more cost-efficient choices, as we explain next.

The fix: Consider a "robo-advisory firm" such as Betterment or Wealthfront—computer-driven services that design and manage a portfolio for 0.25 percent. Or opt for a low-cost target-date retirement fund, which provides a mix that becomes more conservative as you near retirement.

Financial Advice Fees

Many financial advisers levy an annual fee of 1 percent of your assets to manage your portfolio and provide financial advice. And that's on top of fund expense ratios. Typically you must have a sizable investment portfolio—often $250,000 or more.

The fix: Hire a certified financial planner who charges by the hour or a flat fee. Find lists of such advisers through the National Association of Personal Financial Advisors or the Garrett Planning Network. The XY Planning Network offers advisers that charge an annual retainer. (Read more about choosing a financial adviser.)

Account Maintenance Fees

Full-service, or traditional, brokerages often charge fees to maintain your accounts. For instance, Edward Jones charges an annual account fee of $40 for one IRA and $20 for each additional IRA account. Morgan Stanley charges an annual account maintenance fee of $175 that's cut to $150 if you agree to e-delivery of your statements. An additional IRA account maintenance fee ranges from $50 to $100.

The fix: Stick with major online brokerages—such as Schwab and TD Ameritrade—which typically don't charge account maintenance fees.

What the Fee?!

Are you tired of the endless stream of add-on charges that appear on your bills? On the TV show "Consumer 101," Consumer Reports' expert explains to host Jack Rico how to avoid these pesky fees.

Editor's Note: This article also appeared in the July 2019 issue of Consumer Reports magazine. It has been updated with the news that many online brokerages have eliminated commissions for the online trading of stocks, ETFs and other investments.