Michelle Dehetre, a 48-year-old mother of five, had to pull over while driving last March and be taken to the emergency room when her blood sugar dropped too low. One reason for that dangerous decline: The Lewiston, Maine, resident had cut back on her diabetes meds, unable to afford the $300 per month that her treatment would cost, even with insurance.

And Tameka Woodard, 42, a medical assistant from Aberdeen, N.C., moved in with her mother last February so that she could afford medications for high blood pressure, depression, anxiety, and diabetes. Even with insurance, just one of her drugs costs more than $900 per month. "I have insurance, but my medications aren't covered," Woodard says.

Their stories are not uncommon. "High drug prices are financially toxic for American workers," says Stacie B. Dusetzina, Ph.D., associate professor of health policy at the Vanderbilt University School of Medicine in Nashville, Tenn., and co-author of a 2017 report on drug costs by the National Academies of Sciences, Engineering, and Medicine.

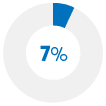

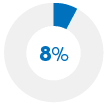

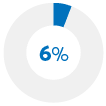

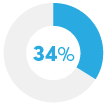

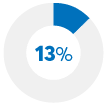

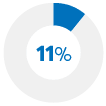

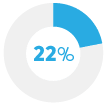

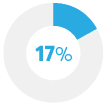

A new Consumer Reports survey backs that up. Thirty percent of Americans who currently take prescription medicine say their out-of-pocket cost for a drug they regularly take has increased in the past year, according to CR's September 2019 nationally representative survey of 1,015 U.S. adults. Of those, 12 percent say their drug costs went up by $100 or more. And those who saw spikes in their out-of-pocket costs were almost twice as likely to not fill a prescription, forgo other medical treatments or tests, cut back on groceries, or get a second job.

One contributing factor: No federal law or regulation effectively keeps drug prices in check. The heads of seven leading drug companies testified before the U.S. Senate last February, often justifying their high drug prices by pointing to the billions of dollars it takes to develop new medications. When pressed by senators, the industry executives said drug costs could be controlled only if the entire payment system was reformed.

Indeed, to pin all the blame on Big Pharma is an oversimplification. How much a consumer pays for meds is also driven in part by drug supply system middlemen whose wheeling and dealing with drugmakers contributes to rising drug costs, according to multiple government reports and industry experts. Shrinking insurance coverage is another part of the problem, with greater numbers of Americans paying a larger share or even the full price of their medication.

For example, Bryan Lumpkin, a 40-year-old from Valley, Ala., recently took a second job as a paramedic, hoping to make enough money to pay for Epidiolex, a drug that Lumpkin says would cost him $2,336 per month and that his son needs to treat seizures—but is not covered by his insurance. "Even if we had been covered, we would have had to meet a $2,000 deductible, then pay $200 every month for refills," Lumpkin says.

And there's no sign of price increases slowing down, even as politicians from both sides of the aisle call for relief. At least 50 separate pieces of legislation that seek to control prescription drug prices were introduced in the Senate and the U.S. House of Representatives in 2019. Some would help to get generic drugs to market faster. Others would legalize buying drugs from Canada or allow the feds to negotiate with drug companies to get lower prices for Medicare. But not one of these has been signed into law.

And while "Medicare for All"—or expanding the government's healthcare program to everyone—has become a common refrain in the current presidential campaign, it's unclear what effect, if any, it would have on drug prices.

Meanwhile, consumers remain caught in the middle. Here, we take a closer look at three complex, hidden forces that contribute to ballooning drug costs, and explain how you can pay less for your meds.

Increased Drug Costs |

No Increased Drug Costs |

||

| Out-of-pocket drug costs increased in the past 12 months. | Out-of-pocket drug costs did not increase in the past 12 months. | ||

|

Did not fill a prescription |

|

|

|

Put off a doctor's visit |

|

|

|

Took an expired medication |

|

|

|

Declined a medical test or procedure |

|

|

|

Did not take a drug as scheduled* |

|

|

|

Swapped an expensive rx drug for a non-rx option* |

|

|

Increased Drug Costs |

No Increased Drug Costs |

|||||

| Out-of-pocket drug costs increased in the past 12 months. | Out-of-pocket drug costs did not increase in the past 12 months. | |||||

|

Spent less on entertainment and dining out |

|

|

|||

|

Used a credit card more often |

|

|

|||

|

Spent less on groceries |

|

|

|||

|

Spent less on family |

|

|

|||

|

Postponed paying other bills |

|

|

|||

|

Took a second job |

|

|

|||

Middlemen Making Money

Although public anger over high drug prices often focuses on drugmakers, there's a middleman who plays a role, too. Pharmacy benefit managers, or PBMs, work under contract with health insurance companies to create a "formulary," a list of drugs the plan agrees to cover, says Neeraj Sood, Ph.D., at the USC Leonard D. Schaeffer Center for Health Policy and Economics in Los Angeles. PBMs also manage prescription drug claims for insurance companies.

Drugmakers who want to get their drugs on a PBM's formulary so that insured people will choose them offer the PBM what's known as rebate payments, Sood says. As consumers fill prescriptions, drug companies issue these rebates. Some of that money stays in the PBM's pocket, while some goes to other players in the prescription drug supply chain, notably insurers, including Medicaid and Medicare plans.

In other industries, that might be considered an illegal kickback. But in the early 1990s, the Department of Health and Human Services (HHS), authorized by Congress, wrote an exception for these rebate payments to federal anti-kickback laws. That allowed drug companies to use the payments as a negotiating tool, according to Stephen Schondelmeyer, Pharm.D., a professor of pharmacoeconomics at the University of Minnesota in Minneapolis.

PBMs have long had a lot of power over what consumers pay for drugs. And a consolidation of the industry over the past several years has made that even more true. Now just three dominate: CVS Caremark, Express Scripts, and OptumRx. In total, they cover more than 150 million people. That allows PBMs to be more aggressive when negotiating with drug manufacturers, demanding higher rebates, Sood says.

Those payments and other discounts doubled over five years, from an estimated $83 billion in 2013 to $166 billion in 2018, according to figures from Adam Fein, an industry consultant and drug pricing expert at the Drug Channels Institute, a research firm.

The Pharmaceutical Care Management Association, which represents PBMs, says its research shows that rebates are not responsible for drug price increases and, in fact, help keep premiums low for consumers.

America's Health Insurance Plans (AHIP), which represents insurers, also says that rebates are a necessary tool that allows insurers to negotiate "with drugmakers for lower consumer costs."

But the problem for consumers is that this system pushes a drug's full, or list, price—like a car's sticker price—higher, as drug companies seek financial wiggle room to provide larger rebates to the PBMs, according to a May 2018 report by HHS (PDF). So while the rebate system might keep some overall costs in check, it could be at the expense of individual patients who need expensive drugs.

One dramatic example: Humira, a rheumatoid arthritis drug from the pharmaceutical company AbbVie. Since 2014, the amount that the company must pay to PBMs increased sharply—about 600 percent. That helped push Humira's list price up 78 percent. (See "Anatomy of a Drug Price: Humira," below.) AbbVie did not respond to requests for comment.

In recent years, the full list price for Humira—an arthritis drug—has jumped, in part as middlemen in the drug supply chain called pharmacy benefit managers have taken a bigger cut. As a result, the cost to consumers—who often have to pay 30 percent of the drug's list price as coinsurance—has also risen sharply, from $874 in 2014 to $1,552 in 2019.

In recent years, the full list price for Humira—an arthritis drug—has jumped, in part because middlemen in the drug supply chain called pharmacy benefit managers have taken a bigger cut. As a result, the cost to consumers—who often have to pay 30 percent of the drug's list price as coinsurance—has also risen sharply, from $874 in 2014 to $1,552 in 2019.

How to address the drug cost problems caused by the rebate system? HHS has proposed eliminating the system entirely for Medicare Part D plans and possibly for commercial plans—an idea PBMs have criticized (PDF) and HHS has reportedly dropped.

Another possible fix: Change the way PBMs are paid, to remove incentives that make drug prices artificially high. That's a proposal from the Pharmaceutical Research and Manufacturers of America (PhRMA), which represents drug companies. It suggests that PBMs get a flat fee for the work they do instead of a negotiated rebate payment, according to Holly Campbell, a PhRMA spokesperson. "This can make the system work better for patients," she says.

Shrinking Insurance

Until recently, consumers with insurance typically paid a flat copay of $10, $25, or $40 for a drug. So the full price of a medication didn't matter much, because most people never paid it, says Dusetzina at Vanderbilt.

But that's changing. As more expensive drugs enter the market, and as drug prices have risen, insurers have come up with a new way to require patients to pay a larger share of the cost and for insurers to pay less: coinsurance. Instead of a flat copay, a consumer's cost for these drugs is now often calculated as a percentage, typically 20 to 30 percent, of the drug's full price, Dusetzina says.

About a third to half of people in commercial plans are charged using a coinsurance percentage for certain drugs, Fein says. That compares with just 3 percent of people enrolled in these plans in 2004. Depending on the drug, a person could be on the hook for hundred dollars or more per month.

To illustrate, consider Humira again. The list price for a month's supply is now $5,174, compared with $2,914 in 2014, according to GoodRx, a company that tracks retail prices for prescription drugs. So people with 30 percent coinsurance would pay $1,552 every month out of pocket—$678 more than just a few years ago.

To make matters worse, the coinsurance payment is typically based on the drug's full list price, not the discounted price that the PBM negotiates for insurers, says Stephen Buck, an industry consultant and a former executive of McKesson, a drug wholesaler. He thinks it would be fairer if a consumer's coinsurance share was based on the discounted price. And at least two pieces of legislation now in Congress would require insurers to do just that. In the case of Humira, that could lower a person's coinsurance payment by more than $600 per month, or $7,000 per year.

Another way to lower the cost of expensive drugs would be to share the rebate with patients as they fill prescriptions. Campbell at PhRMA says that "could save commercially insured patients with high deductibles and coinsurance more than $800 annually and would increase premiums by 1 percent or less."

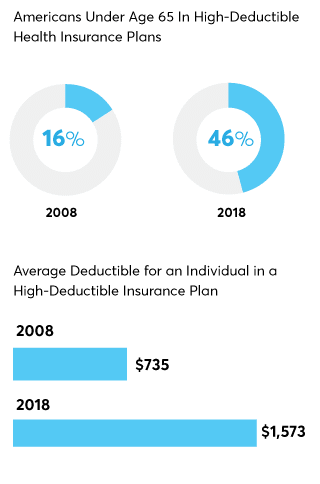

An increasing number of Americans are enrolled in high-deductible health insurance plans, which require an individual to pay an average of nearly $1,600 per year before insurance starts to cover medication and other healthcare costs.

An increasing number of Americans are enrolled in high-deductible health insurance plans, which require an individual to pay an average of nearly $1,600 per year before insurance starts to cover medication and other healthcare costs.

Steeper Deductibles

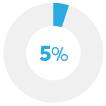

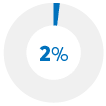

High-deductible plans, which have lower premiums but require consumers to pay more out of pocket before insurance kicks in, became popular in the early 2000s as employers tried to slow the growth of premiums, says Schondelmeyer at the University of Minnesota. Almost half of Americans under age 65 with private insurance are now in these plans, up from 16 percent in 2008, according to the Centers for Disease Control and Prevention.

Insurers often cover a person's drug costs without them having to meet a deductible. But a growing number of plans—now 44 percent—require a person to first meet a deductible, either combined with his or her medical benefit or as a separate drug deductible, according to the Pharmacy Benefit Management Institute, a research group. And until they do meet the deductible, consumers often must pay the full cost for the drugs—not a flat copay or coinsurance.

AHIP says higher deductibles are needed to cover the rising cost of drugs and healthcare overall in this U.S.

But those increased deductibles can strain budgets for many Americans. An employee with a family in a high-deductible plan pays an average of $4,250 before drug coverage starts, according to the PBMI. That's almost four weeks of pay for the average worker. What's more, the deductible is rising, according to another report by the Kaiser Family Foundation. It found that between 2010 and 2015, the average annual deductible for workers with health insurance increased 67 percent.

About a quarter of employers have tried to soften the blow by limiting how much more people in high-deductible plans must pay for healthcare after they reach their deductible, according to the PBMI. The average amount for these so-called out-of-pocket maximums is $5,380 for a family or $2,699 for an individual.

"Even if insured, consumers facing a life-threatening condition or a costly disease who don't have an out-of-pocket maximum could be bankrupted by medical bills," says Dena Mendelsohn, senior policy counsel at CR. "Out-of-pocket maximums protect consumers from debilitating medical bills so they can focus on their care."

How to Lower Your Drug Costs

Although the behind-the-scenes forces that drive up drug prices trace back to the problematic way healthcare is delivered and paid for in this country, that doesn't mean you're powerless. Here are several steps you can take to make your meds more affordable.

With Your Doctor

Request generics. When a doctor recommends a prescription drug, ask whether a generic version is available. Most brand-name drugs have generic equivalents, and these generics can be up to 90 percent cheaper, Schondelmeyer says.

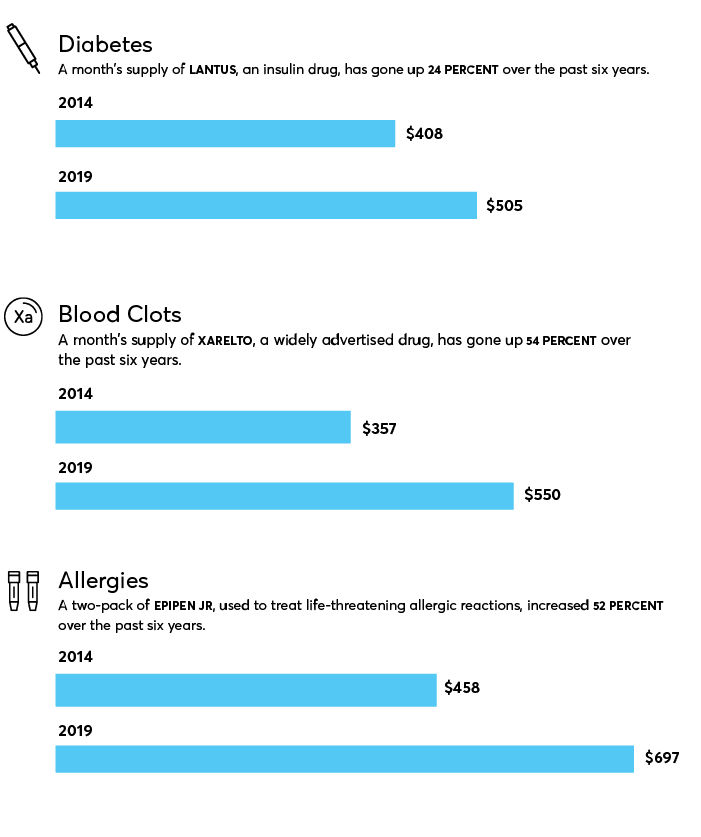

Look for other treatments. If there is no generic version, ask your doctor whether there is another drug, perhaps older but still tried-and-true, to try first. About 70 percent of expensive drugs have alternatives, Schondelmeyer says. For example, people who need a blood thinner may be prescribed Eliquis or Xarelto, both of which cost about $550 per month. But an older drug, warfarin, retails for about $19 per month and might be an option for you. Doctors often don't ask patients about their ability to afford treatment, according to a 2019 physician survey in the Annals of Internal Medicine, so you might have to initiate the conversation.

Ask about over-the-counter options. Certain new, pricey medications are actually combinations of two older, inexpensive drugs, some you can buy without a prescription. Consider Duexis, used to treat arthritis and prevent stomach ulcers. It has a list price as high as $2,601 on GoodRx. But Duexis is simply two over-the-counter drugs, ibuprofen and famotidine, combined into one pill. The two, separately, could be purchased without a prescription for less than $19. Always check with your physician before changing your medication.

When Picking Up Your Drugs

Talk with your pharmacist. If you get to the pharmacy counter only to be shocked by the price of your medication, ask the pharmacist whether there's a way to make it more affordable. CR's secret shoppers have found that pharmacists can often find discounts or in-store deals. They can also contact your physician to change the prescription to a lower-cost alternative when appropriate, Schondelmeyer says.

Use manufacturer discounts. Many drugmakers offer some type of discount, especially for expensive drugs, to help lower out-of-pocket costs, says Rich Sagall, M.D., president of NeedyMeds, a nonprofit that connects consumers with discount programs. These can help if the drug has a steep copay, is subject to coinsurance, or isn't covered by your insurer. For example, Janssen, which makes Xarelto, offers a discount that can bring the price down to as little as $10. You can find an up-to-date list of drugmaker discounts at NeedyMeds.

Note that details vary from program to program. For example, in some cases only the amount you pay out of pocket may go to your deductible, not the coupon's full value, Buck says. So if you have a $100 copay and the coupon covers $90, only $10 is credited to your deductible. That's an unwelcome change compared with two years ago, when the full coupon could have gone toward your deductible, Buck says.

Look for patient assistance programs. Sagall suggests checking with the drugmaker to see whether you qualify for an income-based patient assistance program. Some companies have recently raised the cutoffs on these programs to as high as $100,000. Note that you might not be eligible if you have insurance or are enrolled in Medicare or Medicaid, Sagall says. But check anyway, because programs differ and often change. NeedyMeds lists these programs, too.

Many drugs have increased in prices over the past few years. Below, three examples:

Many drugs have increased in prices over the past few years. Below, three examples:

When Buying Insurance

Choose insurance plans carefully. Some employers are now offering more low-deductible options, Schondelmeyer says. Though these plans have higher premiums, they can be good choices, especially if you or someone in your family regularly takes expensive drugs.

Consider opening a health savings account. If you're stuck with a high-deductible plan, ease the pain by opening a health savings account. It lets you save pretax money for qualified health expenses, including prescriptions. An individual can deposit up to $3,550 per year and a family $7,100 into these accounts. Unused funds from one year roll over into the next. Many employers who offer high-deductible plans also provide an HSA option—some even help fund it. But if your employer doesn't, you can open one on your own with a bank, a credit union, an insurer, or an investment company. To qualify, your deductible must be a minimum of $1,400 for an individual or $2,800 for a family.

Editor's Note: This article also appeared in the January 2020 issue of Consumer Reports magazine.